1 Dividend King And 1 Aristocrat To Add To Your Income Watchlist

"Both Stocks Trade Below Their 5-Year Averages"

As you know by my name, I love dividends. And in addition to sharing on here, I write regularly on the investment platform- Seeking Alpha.

My goal there is to teach everyday investors about building wealth, so they won’t to need to work to traditional retirement age.

I want to help you take control of your life, have F.I.R.E.

Here at Dividend Collection Agency the goal is to give investors and/or readers a different perspective. We take a simple approach to building wealth. And although investing may seem easy, people often miss opportunities by over complicating it.

But we are here to help.

The market has remained surprisingly resilient despite persistent inflation, with the S&P 500 (SP500) up roughly 17% in 2025. Yet beneath the surface, several high-quality companies have struggled, leaving investors frustrated as share prices continue to lag.

As a value investor, that’s exactly where I look for opportunities.

When quality businesses fall out of favor, investors have a chance to buy strong companies at attractive prices. And if those companies eventually return to their historical valuation ranges, the upside can be significant.

Today, I’ll discuss two dividend growth stocks that appear positioned for a strong rebound over the next 2 to 5 years.

1. PepsiCo (PEP) 🥤

PepsiCo isn’t a stock many investors are excited about today.

Despite gaining roughly 12% over the past year, the Dividend King has significantly underperformed the broader market over longer periods. Over the last three years, Pepsi shares have declined approximately 21%, while the S&P 500 has gained more than 67%.

The primary culprit has been inflation.

Higher input costs and weaker consumer demand have pressured margins across the consumer staples sector. While Pepsi’s iconic brands remain resilient, the company has struggled to generate the level of growth investors became accustomed to in previous years.

However, recent results suggest conditions may be improving.

During the most recent quarter:

Revenue increased 8.5%

EPS rose to $1.61, beating estimates

Food volumes grew 4%

EMEA organic sales increased 7%

The U.S. business remains sluggish, but international growth continues to provide support.

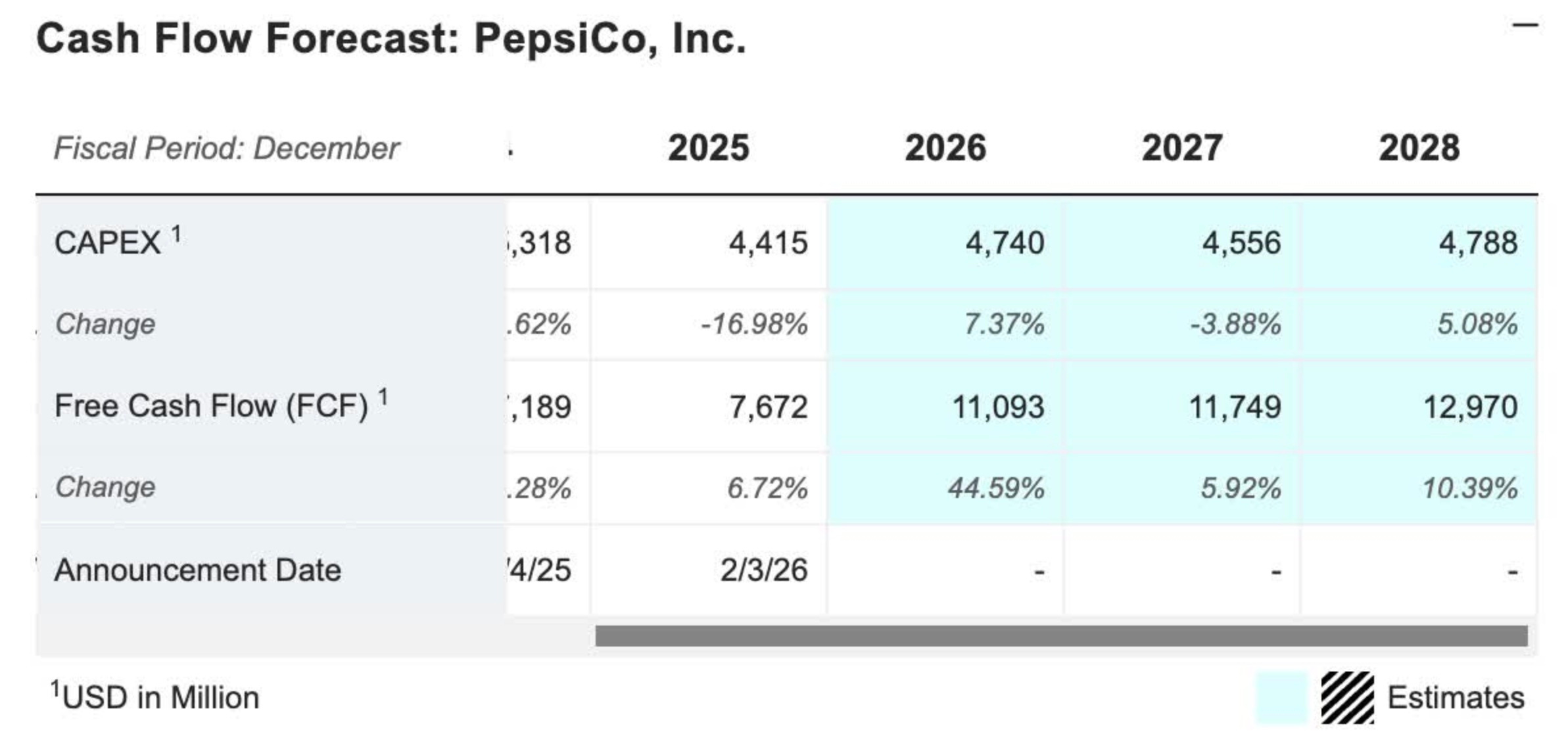

Cash Flow Could Be Turning the Corner 💵

Pepsi’s biggest concern remains its elevated payout ratio.

While free cash flow improved in 2025, the dividend consumed nearly all of it, resulting in a payout ratio near 100%.

Normally, that’s not a situation I like to see.

However, Pepsi has spent aggressively on acquisitions designed to reignite growth. The most notable was its $2 billion acquisition of Poppi, the rapidly growing prebiotic beverage company.

Management has already indicated Poppi is performing well and expects it to become a meaningful contributor to future growth as distribution expands.

Wall Street also expects Pepsi’s free cash flow to improve significantly over the next several years, with estimates projecting growth from roughly $7.7 billion today to nearly $13 billion by 2028.

If that occurs, dividend coverage improves, buybacks accelerate, and investor sentiment could shift dramatically.

Valuation Looks Attractive 🤔

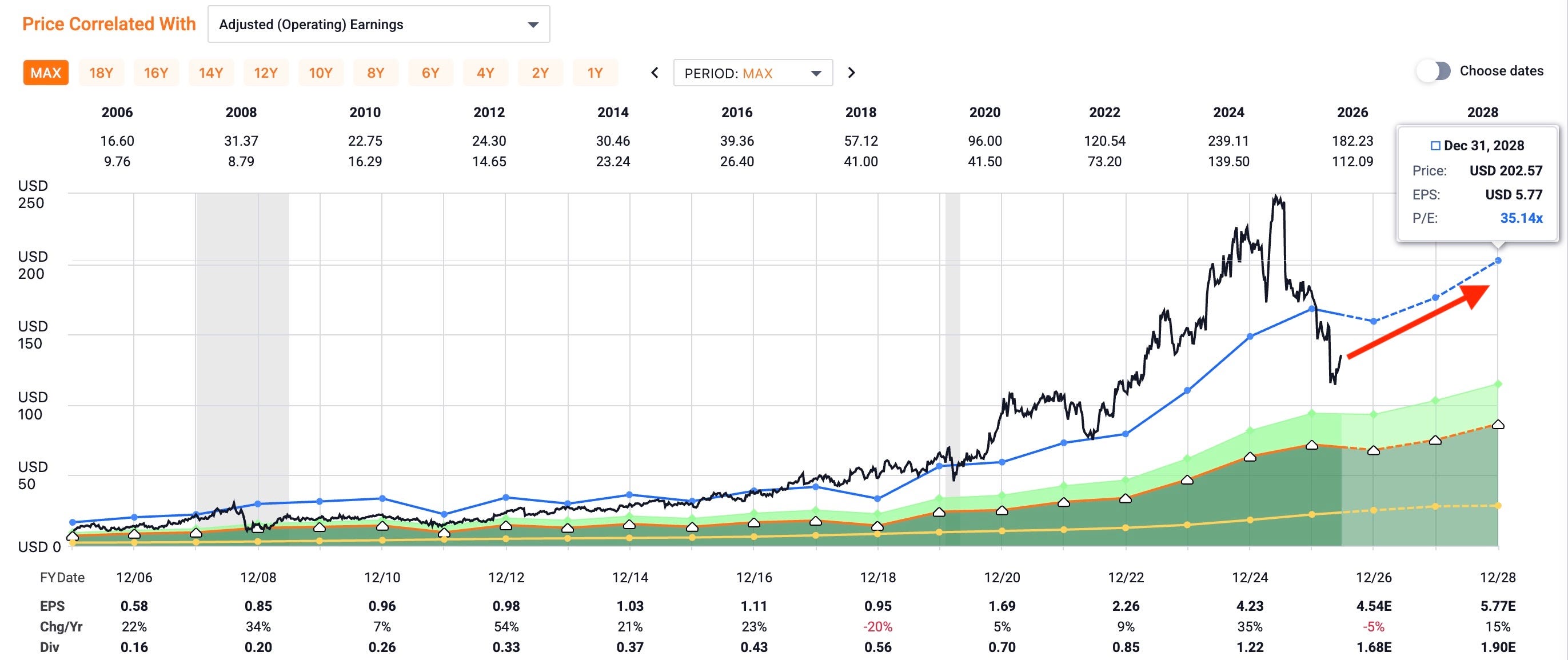

At approximately 16.6x forward earnings, Pepsi trades below its historical average valuation.

Analysts currently project around 6% annual earnings growth through 2028. If Pepsi simply delivers on those expectations and returns closer to its historical multiple, shares could approach close to $200 by the end of 2028.

If you’re looking for a stock analyzer tool that gives you future price targets based on historical data, use my code to get 25% off of FAST Graphs, my go-to the stock analyzer tool for research.

For a company with an A-rated balance sheet, a 50+ year dividend growth streak, and some of the strongest consumer brands in the world, I believe the risk/reward looks attractive at current levels.

2. Badger Meter (BMI) 💡

The second stock is much less well known.

Badger Meter is a Dividend Aristocrat focused on water technology, serving utilities and municipalities through products that measure water flow, quality, pressure monitoring, and sewer infrastructure.

Although the long-term story remains compelling, shares have been punished over the past year.

The stock has fallen more than 46% from its 52-week high as inflation, tariffs, and slower project activity pressured results.

In my opinion, part of that decline was simply a valuation reset.

At its peak, BMI traded at more than 45x earnings. Today, the stock trades closer to 28x forward earnings — still not cheap, but considerably more reasonable.

Short-Term Headwinds, Strong Long-Term Fundamentals 💪🏾

The latest quarter wasn’t impressive:

Revenue declined 9%

EPS fell 28.5%

Operating margins contracted to 17.4%

Gross margins declined to 41.7%

Management cited project delays and inflation-related pressures as key challenges.

While those numbers aren’t ideal, I view them as temporary.

Management expects growth to improve during the second half of the year as delayed projects begin moving forward.

More importantly, the company’s balance sheet remains exceptional.

Badger Meter currently has:

Zero debt

$205 million in cash

$150 million of available revolving credit capacity

That financial flexibility gives management ample room to pursue acquisitions during periods of weakness.

Growth Through Acquisitions 🛍️

One reason I’m optimistic on BMI is its ability to expand through bolt-on acquisitions.

A recent example is the acquisition of UDlive, a sewer-monitoring company with approximately 60% market share in the United Kingdom.

Management expects the deal to be immediately accretive, and I believe it likely won’t be the last acquisition we see.

The combination of a debt-free balance sheet, recurring infrastructure demand, and strategic acquisitions creates a compelling long-term growth story.

Dividend Growth Remains Outstanding 💸

While many investors focus on earnings volatility, BMI’s dividend track record remains exceptional.

The company has increased its dividend for 33 consecutive years and has delivered a three-year dividend growth rate of more than 21%.

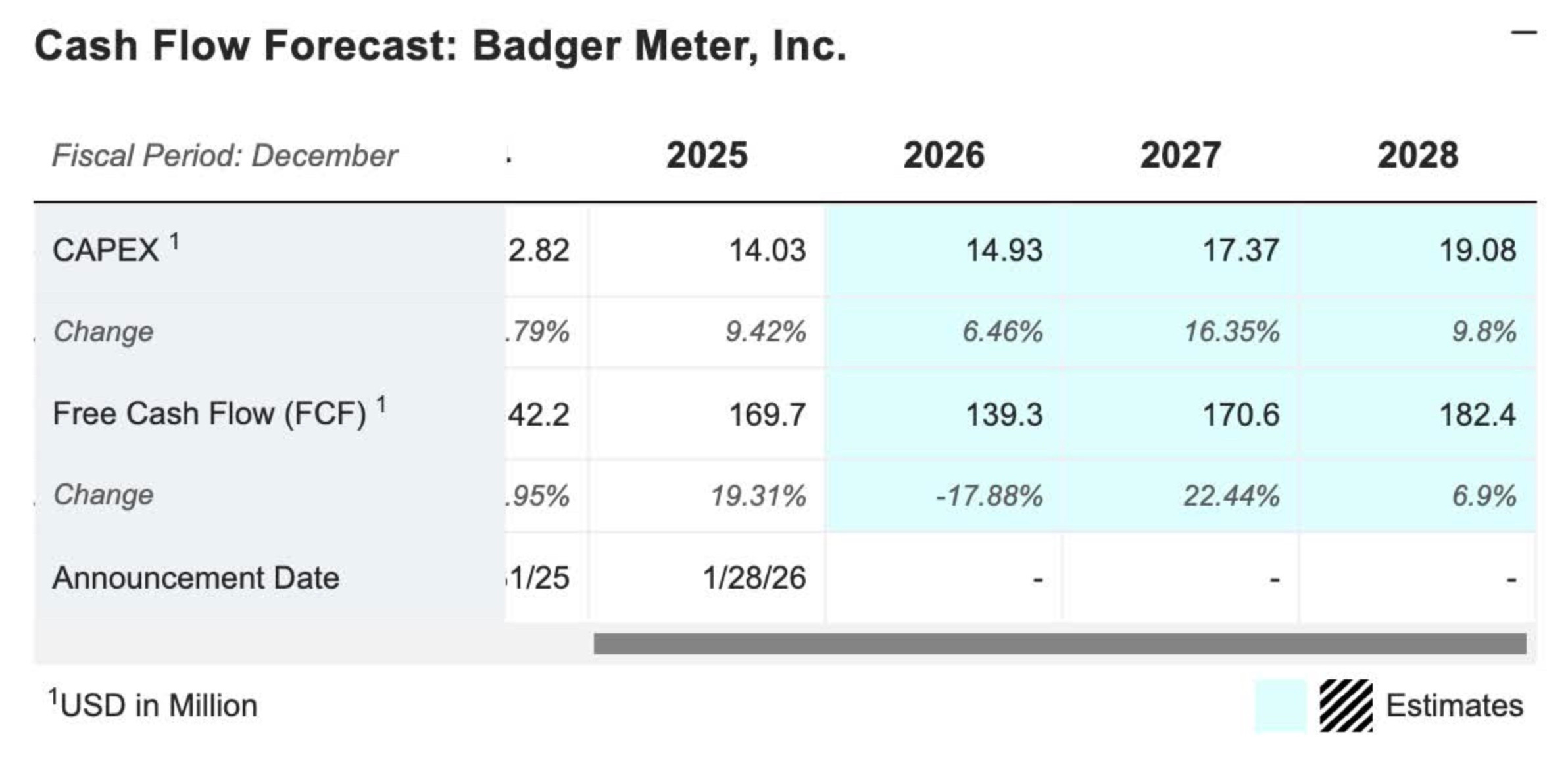

Even after the recent slowdown, the dividend remains extremely well covered, with a payout ratio near 26%. Free cash flow is expected to decline this year and pick back up in 2027.

Given management’s historical approach, I wouldn’t be surprised to see another double-digit dividend increase later this year.

Long-Term Upside 📉

Although analysts expect some softness in free cash flow during 2026, growth is projected to accelerate again beginning in 2027.

If you’re looking for a stock analyzer tool that gives you future price targets based on historical data, use my code to get 25% off of FAST Graphs, my go-to the stock analyzer tool for research.

As earnings recover and acquisitions contribute, analysts currently see meaningful upside from current levels, with an average price target of roughly $203 over the next two to three years.

Risks ⚠️

The biggest risk for both Pepsi and Badger Meter remains inflation.

If inflation continues accelerating, margins could remain under pressure and delay earnings growth.

Additionally, ongoing geopolitical uncertainty could keep commodity and transportation costs elevated, creating further headwinds.

For that reason, investors should continue monitoring profit margins and management commentary for signs of stabilization.

Final Thoughts ✅

Neither Pepsi nor Badger Meter is likely to be a market darling over the next six to twelve months.

However, investing isn’t about buying what’s popular today—it’s about identifying quality businesses before sentiment improves.

Both companies possess strong competitive advantages, solid balance sheets, growing dividends, and valuations below their historical norms.

While short-term volatility may persist, I believe Pepsi and Badger Meter offer attractive risk-adjusted upside for dividend growth investors willing to remain patient over the next 2 to 5 years.

PEP RATING: SPECULATIVE BUY

BMI RATING: SPECULATIVE BUY

Do Pepsi and Badger Meter fit into your portfolio strategy?? Let me know in the comments.

Happy Investing 💰

☎️ If you’re looking to create passive income and build your wealth from one of the top-rated analysts, book a call (Let’s Talk Investing or Detailed Portfolio Review) with me to get started.

If you’re looking to start investing check out our investment group over on Seeking Alpha.

Here’s How: Click the Seeking Alpha link here. Click investing group, subscribe now (GET AN INVESTING GROUP FREE TRIAL), or the blue hyperlink in my bio.

‼️ Seeking Alpha is also currently offering a 20% membership sale ‼️

Not financial advice. For educational purposes only. I am not a licensed professional. Do your own due diligence.

Like & subscribe if you’re active duty, a veteran, or just love investing.