2 Attractively-Priced Dividend Growth Stocks To Buy Now

"Near-Term Risks Improve The Long-Term Setup"

As you know by my name, I love dividends. And in addition to sharing on here, I write regularly on the investment platform- Seeking Alpha.

My goal there is to teach everyday investors about building wealth, so they won’t to need to work to traditional retirement age.

I want to help you take control of your life, have F.I.R.E.

Here at Dividend Collection Agency the goal is to give investors and/or readers a different perspective. We take a simple approach to building wealth. And although investing may seem easy, people often miss opportunities by over complicating it.

But we are here to help.

For me, June is one of my favorite months of the year.

Not only does it mark the official start of summer, but it’s also a time when people are traveling, relaxing, and enjoying the warmer weather. Personally, I enjoy taking small road trips and spending time poolside.

This year, however, there’s another reason I’m excited.

With June getting off to a rocky start and stocks pulling back, I’m seeing attractive buying opportunities emerge in several high-quality businesses.

At the time of writing, the Dow Jones Industrial Average (DJI) has fallen more than 400 points as investors weigh rising oil prices, persistent inflation, and growing uncertainty surrounding future Federal Reserve policy.

Going forward, I expect volatility to remain elevated. Inflation risks continue to build, and if economic conditions worsen, the Federal Reserve could be forced to keep rates higher for longer—or potentially tighten further.

For long-term income investors, however, market pullbacks should be viewed as opportunities rather than reasons to panic.

As a result, I continue to dollar-cost average into quality businesses with strong balance sheets, growing cash flows, and attractive long-term dividend growth potential.

Today, I’ll discuss two dividend growth stocks I’m currently buying and why I believe both offer compelling upside over the next 24 to 36 months.

Things Could Get Worse 😱

Markets are currently reacting to higher oil prices as geopolitical tensions between the United States and Iran continue to escalate.

While the outcome remains uncertain, one thing appears increasingly likely: inflation may remain elevated for longer than many investors expected.

Recent increases in energy prices have already pushed inflation higher, and if oil prices continue climbing, it could further complicate the Federal Reserve’s efforts to bring inflation back toward its long-term target.

As a result, expectations for rate cuts have shifted dramatically compared to the start of the year.

If inflation remains stubbornly high, the possibility of additional rate hikes cannot be ruled out.

The question investors should be asking is simple:

What happens if rates move higher?

Personally, I believe the market would experience another meaningful sell-off. Whether temporary or prolonged, it could mark the beginning of the correction many investors have been anticipating.

For me, the strategy remains unchanged.

I’ll continue building positions in quality businesses, collecting dividends, and allowing market volatility to work in my favor.

And right now, two stocks stand out.

T-Mobile US (TMUS) 📱

The first stock I’m buying is T-Mobile.

Over the past year, shares have fallen more than 25%, largely due to valuation compression, macroeconomic concerns, and a recent legal ruling that pressured the entire telecom sector.

While many investors remain concerned about telecom debt levels in a higher-rate environment, I believe T-Mobile remains the strongest operator in the industry.

The company currently maintains the lowest leverage ratio among the major wireless carriers at approximately 2.4x, compared to roughly 2.6x for Verizon (VZ) and 2.7x for AT&T (T).

Meanwhile, T-Mobile continues to execute exceptionally well operationally.

During its most recent quarter, the company delivered strong subscriber growth, double-digit revenue growth, and raised full-year guidance.

Management also increased expectations for EBITDA and free cash flow generation, highlighting continued confidence in the business despite macroeconomic uncertainty.

What excites me most is the company’s capital allocation strategy.

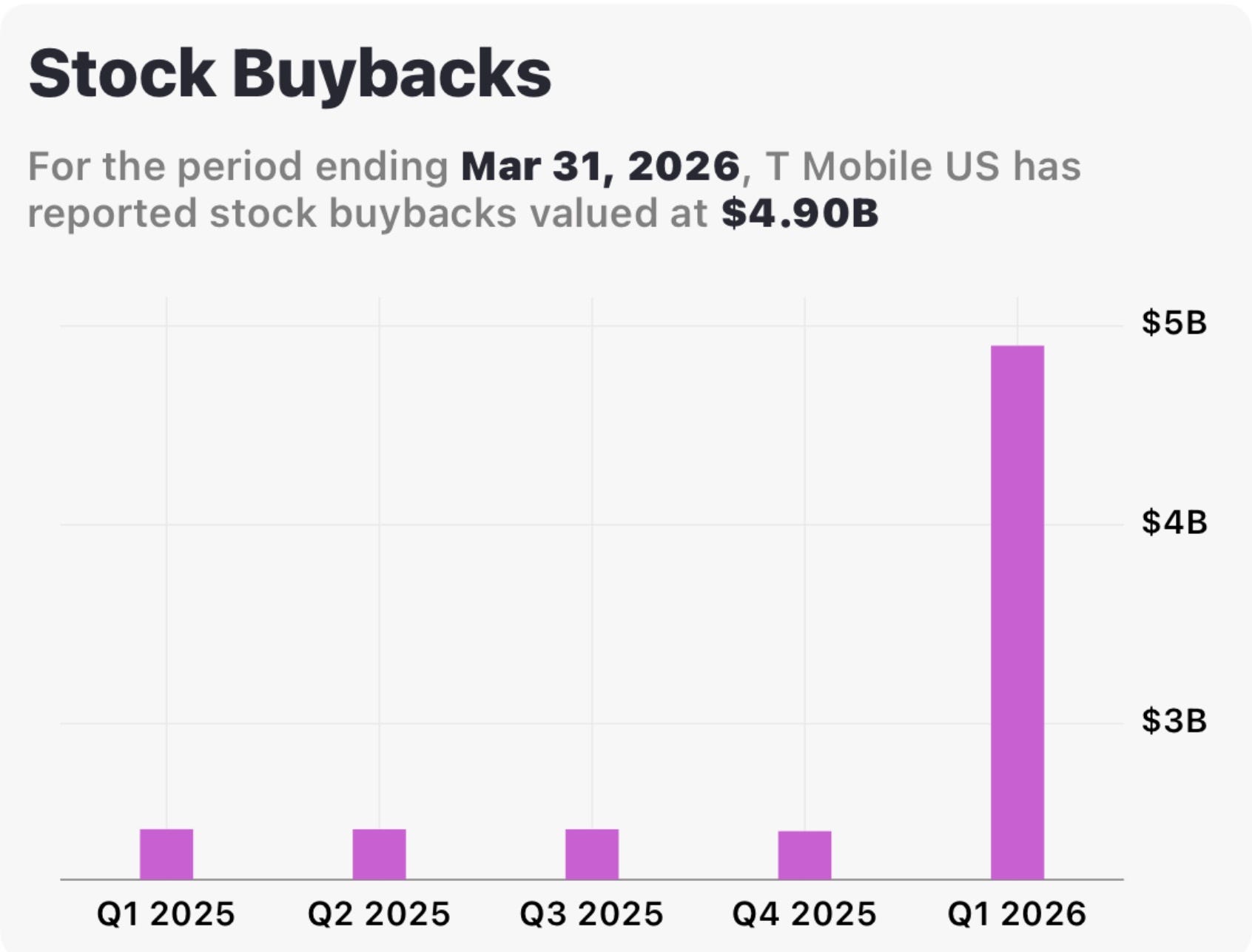

T-Mobile finished 2025 with a free cash flow payout ratio below 25%, giving management significant flexibility to continue growing the dividend while simultaneously repurchasing shares.

Share repurchases nearly doubled year-over-year during the most recent quarter, signaling both financial strength and management’s belief that shares are undervalued.

Given the current valuation, I expect T-Mobile to continue delivering double-digit dividend growth for the foreseeable future.

Trading at roughly 16x forward earnings, shares now sit well below historical valuation levels despite the business remaining fundamentally stronger than ever.

For long-term investors, I believe the risk/reward profile remains highly attractive.

Otis Worldwide (OTIS) 🛗

The second stock I’m buying is Otis Worldwide.

Like T-Mobile, shares have fallen more than 25% over the past year as investors focus on inflation pressures and ongoing weakness within China’s construction market.

While these headwinds are real, I view them as cyclical rather than structural.

Otis remains one of the highest-quality industrial businesses in the world, supported by a highly recurring service business and a dominant global market position.

Despite macroeconomic challenges, the company still delivered revenue growth during its most recent quarter while showing encouraging signs of stabilization across several regions.

Most notably, orders in the Americas increased 20%, while trends in Asia improved modestly compared to prior periods.

Management continues to offset inflationary pressures through cost-saving initiatives, generating approximately $170 million in savings last year alone.

At the same time, Otis continues investing in future growth opportunities.

Recent investments in digital elevator technology, service modernization, and products targeting the rapidly growing data-center market should help support long-term growth once economic conditions improve.

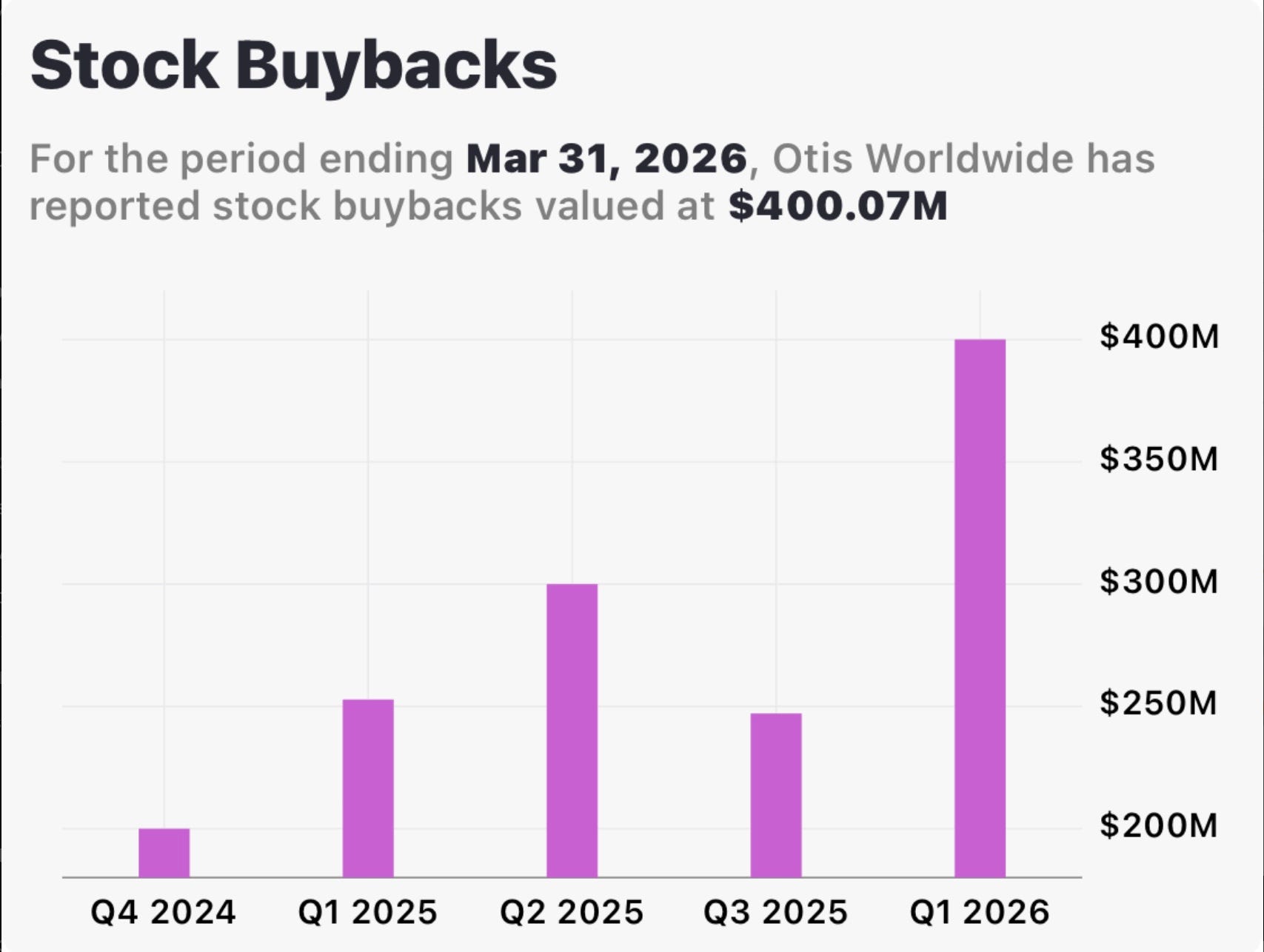

Like T-Mobile, management has been highly shareholder friendly.

The company recently increased its dividend and continues to aggressively repurchase shares, with plans to buy back approximately $800 million of stock this year.

Given the company’s modest debt profile, recurring cash flows, and disciplined capital allocation strategy, I believe Otis is well-positioned to emerge stronger once inflation and China-related headwinds begin to ease.

Trading at less than 17x forward earnings, shares currently trade well below both historical valuation averages and industry peers.

For patient investors, I believe the current valuation creates an attractive entry point.

My June Purchases 🗓️

I’ve already added to both positions during the recent weakness.

T-Mobile remains a stock I’m actively accumulating below $180 per share and would likely become even more attractive should shares decline further.

Likewise, I recently purchased Otis below $70 per share and would continue adding aggressively if shares fall into the high-$60s.

While neither stock offers a particularly high current yield, both possess what I believe is far more important: strong dividend growth potential.

Over time, dividend growth combined with share repurchases and earnings expansion can create substantial shareholder returns.

Risks & Final Thoughts⚠️

There is no guarantee either stock has reached its bottom.

If inflation continues rising, geopolitical tensions worsen, or the Federal Reserve adopts a more hawkish stance, both T-Mobile and Otis could experience additional near-term downside.

T-Mobile could see slower subscriber growth, while Otis could face continued margin pressure and weakness within China.

Those risks are real.

However, I believe both companies possess the balance sheets, competitive advantages, and cash-flow generation necessary to navigate a challenging economic environment.

Over the next 24 to 36 months, I expect macroeconomic conditions to gradually improve.

When they do, I believe both T-Mobile and Otis are positioned to reward patient shareholders through a combination of earnings growth, dividend increases, and valuation expansion.

Until then, I’m happy collecting growing dividends from two high-quality businesses trading at far more attractive prices than they were just a year ago.

RATINGS: BUY

What do you think of these two stocks? Let me know in the comments.

Just a note to let readers know I will be going paid soon. Be on the lookout for the article laying out the details. Feel free to provide any feedback!

Happy Investing!

☎️ If you’re looking to create passive income and build your wealth from one of the top-rated analysts, book a call (Let’s Talk Investing or Detailed Portfolio Review) with me to get started.

If you’re looking to start investing check out our investment group over on Seeking Alpha.

Here’s How: Click the Seeking Alpha link here. Click investing group, subscribe now (GET AN INVESTING GROUP FREE TRIAL), or the blue hyperlink in my bio.

Not financial advice. For educational purposes only. I am not a licensed professional. Do your own due diligence.

Like & subscribe if you’re active duty, a veteran, or just love investing.

I appreciate that you bring some insightful finds in the dividend stock niche. There are a lot of weird ideas floating around on Substack about why “dividends are bad.”

I did a deep analysis on To Mobile a while back. Good business, but I decided not to buy. That doesn’t mean it’s not a good stock though.

Keep up the good work!