A 18% Yielder I Would Avoid At All Costs

“All High Yields Aren't Created Equal”

As you know by my name, I love dividends. And in addition to sharing on here, I write regularly on the investment platform- Seeking Alpha.

My goal there is to teach everyday investors about building wealth, so they won’t to need to work to traditional retirement age.

I want to help you take control of your life, have F.I.R.E.

Here at Dividend Collection Agency the goal is to give investors and/or readers a different perspective. We take a simple approach to building wealth. And although investing may seem easy, people often miss opportunities by over complicating it.

But we are here to help.

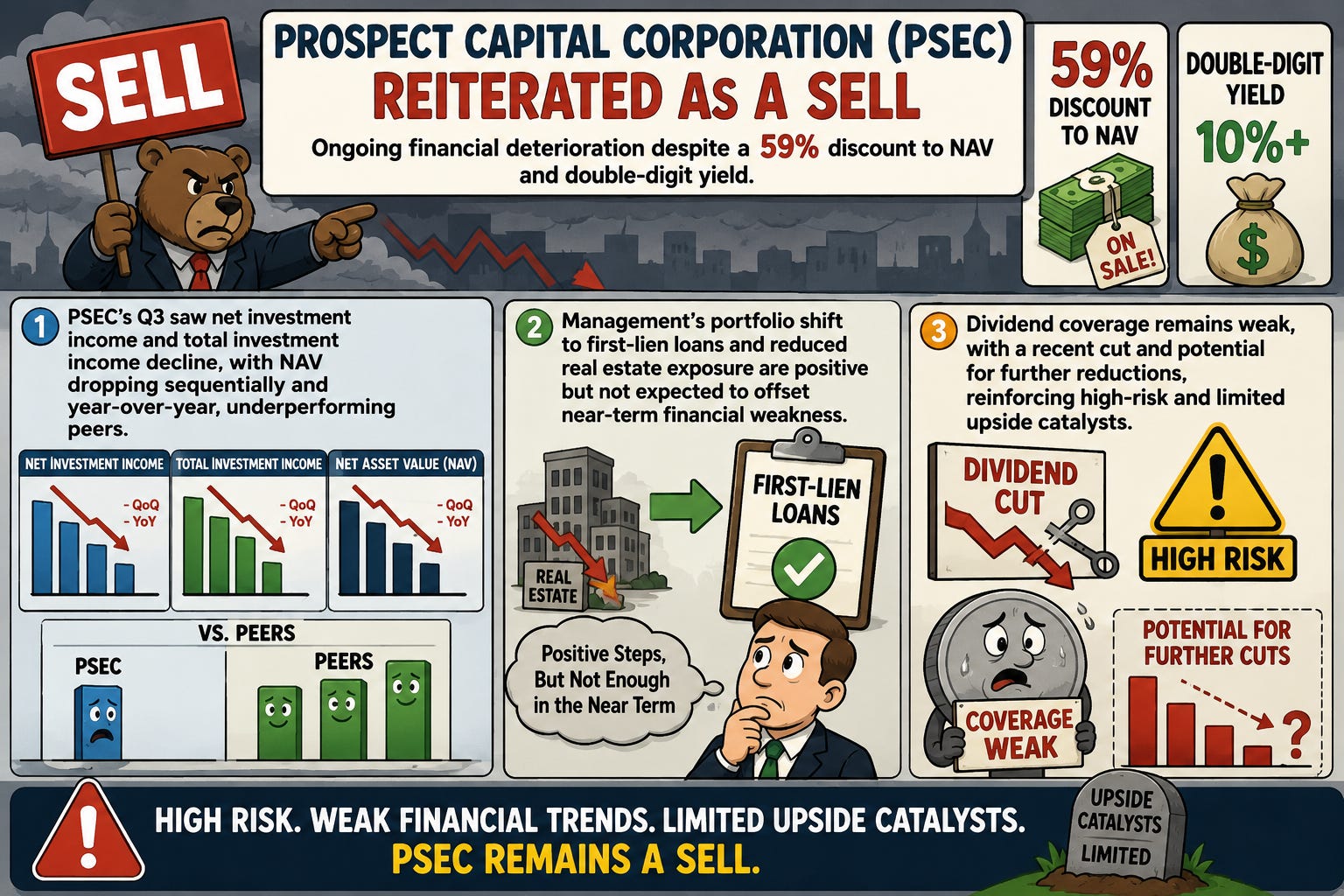

Current Price: $2.35

Dividend/Yield: 17.9%

I’m naturally someone who tries to find the good in any situation, even when it comes to investing during periods of elevated volatility.

But when a stock consistently experiences heavy downside pressure, there’s usually a reason beneath the surface.

In the case of Prospect Capital Corporation (PSEC), a Business Development Company (“BDC”) I’ve remained bearish on for close to a year, the steep discount to NAV and double-digit yield may initially appear attractive.

However, beneath the surface, deteriorating fundamentals, shrinking income generation, declining NAV, and a recent dividend reduction suggest the pain likely isn’t over.

In this article, I discuss Prospect Capital’s latest earnings, what caused the post-earnings sell-off, and why I continue to expect underperformance moving forward.

Another “PSEC-Like” Quarter 📊

Often times when I say a company delivered “another similar quarter,” it usually means consistency and stability.

But in the case of Prospect Capital, this meant another quarter of financial deterioration.

While Net Investment Income (“NII”) technically beat analyst estimates by $0.05 per share, it still declined sequentially from the prior quarter’s $0.19.

More importantly, total NII dollars continued falling sharply.

Key Weaknesses From Q3:

Net investment income declined 14.3% sequentially

Total investment income missed estimates by roughly $13 million

Revenue declined from $170.7 million to $150.1 million year-over-year

Portfolio value continued shrinking

NAV declined sequentially and year-over-year

One thing many investors overlook with BDCs is that deterioration can often be hidden beneath the dividend yield.

Investors may focus heavily on:

Dividend yield

Discount to NAV

NII per share

But sometimes ignore:

Shrinking portfolio value

Declining earnings power

Deteriorating asset quality

Falling total income generation

That’s exactly why I describe this as another “PSEC-like” quarter.

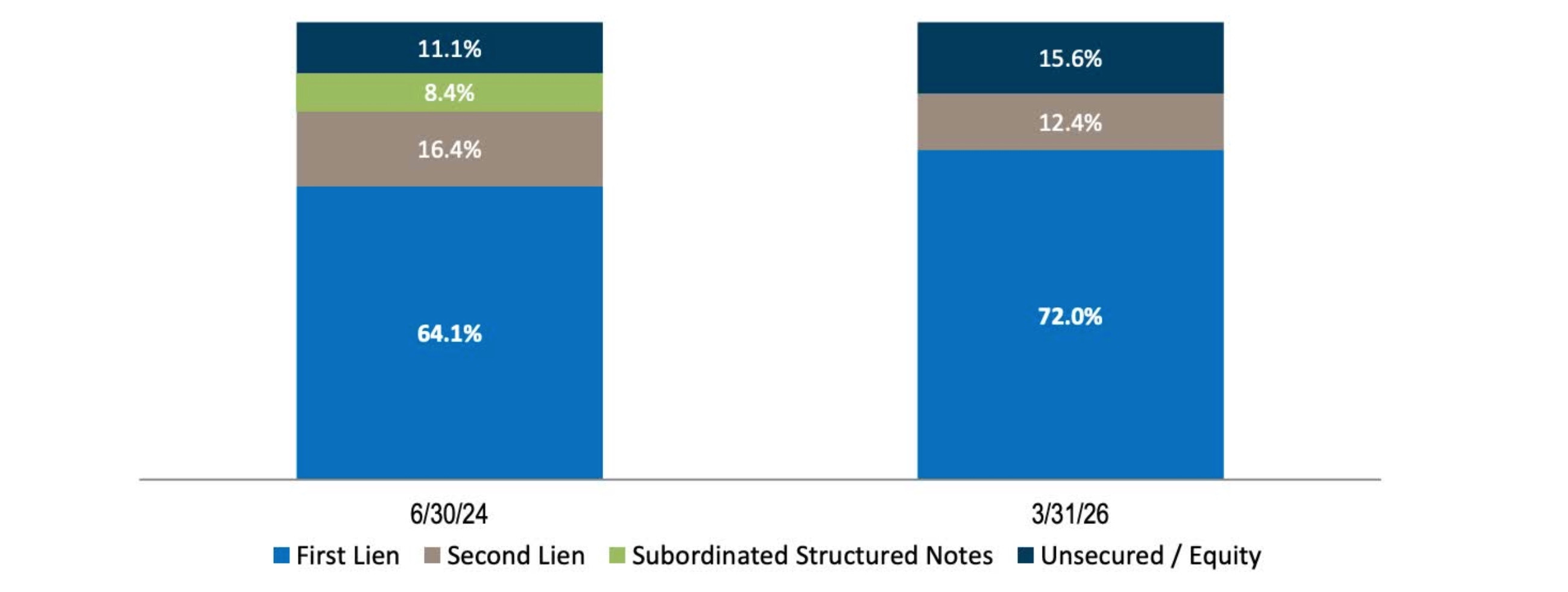

Continued Portfolio Shift 📝

Another major contributor to Prospect Capital’s earnings pressure is the company’s ongoing portfolio repositioning strategy.

Management continues reducing real estate exposure while increasing allocation toward first-lien loans in an effort to improve credit quality and stabilize the portfolio long-term.

Over the past two years:

First-lien exposure increased from 59% to 72%

Real estate exposure continued declining

Portfolio company count fell from 122 to 89

From a risk management perspective, this shift makes sense.

First-lien loans generally:

Offer stronger downside protection

Sit higher in the capital structure

Reduce overall credit risk

However, repositioning the portfolio comes at a cost.

Asset sales and restructuring activity continue pressuring earnings, and I believe this trend likely persists for at least the next several quarters.

Additional Concerns:

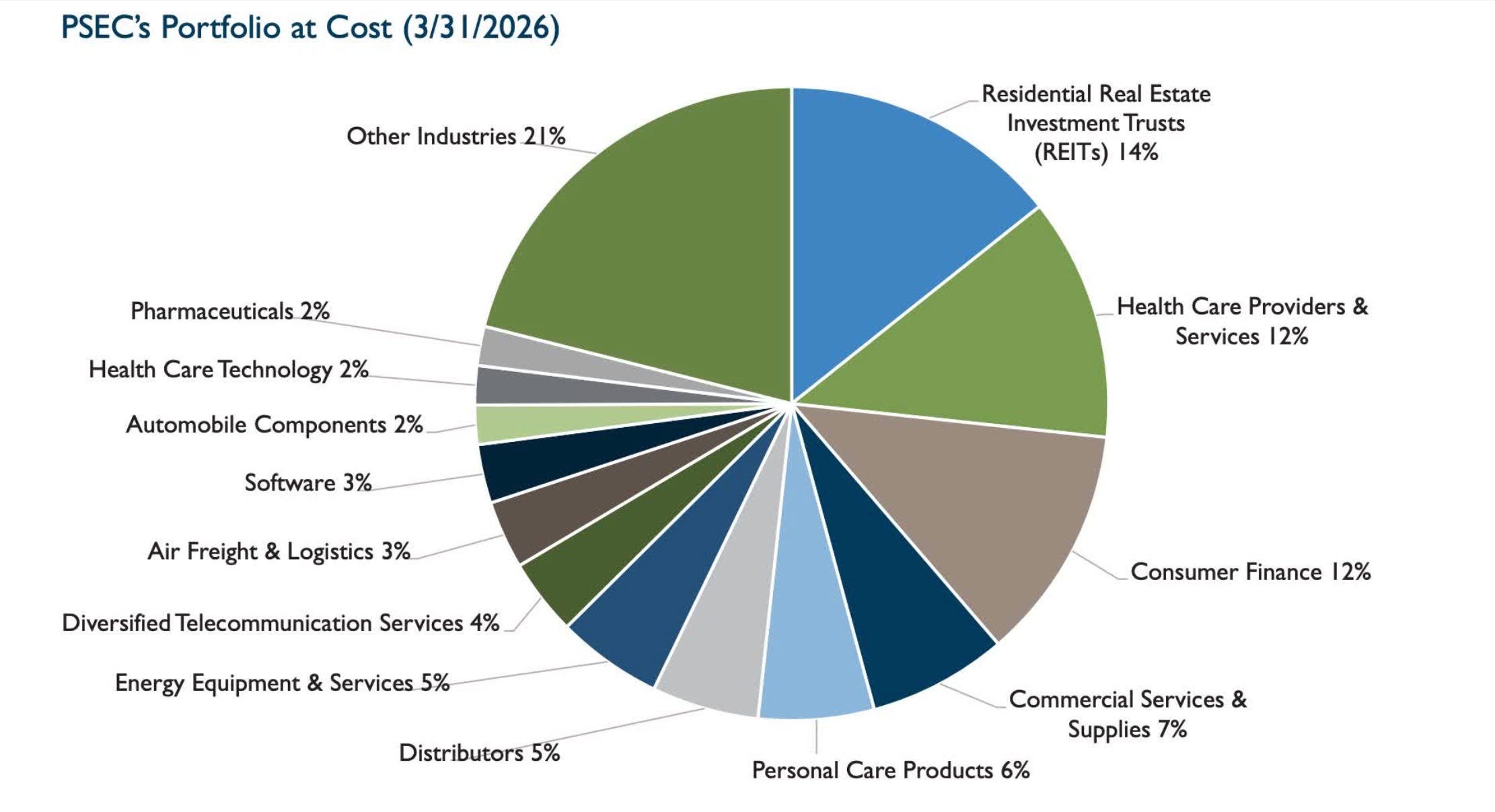

Total portfolio value declined from $7.8B to $6.3B

Real estate still accounts for 14% of investments

Earnings accretion from repositioning could take years

So, while management is making defensive adjustments, investors are still dealing with weakening financial performance today.

NAV Erosion Remains A Massive Red Flag 🚩

One of the most concerning aspects of Prospect Capital’s quarter was continued NAV deterioration.

NAV declined:

From $6.21 to $6.05 sequentially

From $8.99 to $6.05 year-over-year

That’s an enormous decline for a BDC. And when compared to peers, Prospect Capital’s underperformance becomes even more apparent.

Peer NAV Comparisons:

TriplePoint Venture Growth BDC Corp. (TPVG): NAV increased slightly

PennantPark Investment Corporation (PNNT): Moderate NAV decline

Barings BDC, Inc. (BBDC): Relatively stable NAV

Meanwhile, PSEC experienced severe erosion.

For BDCs, NAV stability and growth are critical indicators of long-term health.

Persistent NAV destruction often signals:

Weak underwriting

Poor credit performance

Deteriorating portfolio quality

Increased risk of long-term capital loss

And unfortunately, that’s exactly what investors continue seeing with PSEC.

The “Sneaky” Dividend Cut ✂️

Another major negative from the quarter was the dividend reduction.

Management quietly reduced the monthly dividend from $0.04 to $0.035 per share.

While a penny may not seem significant, dividend cuts for BDCs often carry psychological importance.

They signal:

Weak dividend coverage

Reduced earnings power

Pressure on future distributions

Lower investor confidence

This was something I warned about previously. And frankly, I wouldn’t be surprised to see another dividend reduction sometime later this year if earnings continue trending lower.

The combination of:

Falling NII

Declining portfolio value

Weak coverage ratios

NAV erosion

All of this creates a difficult setup for sustaining current payouts long-term.

The Huge Discount To NAV Isn’t Enough 🏷️

At first glance, a 59% discount to NAV and double-digit yield looks incredibly attractive.

But sometimes steep discounts exist for a reason.

In my opinion, PSEC’s discount reflects:

Weak investor confidence

Persistent financial deterioration

Concerns over future dividend cuts

Lack of growth catalysts

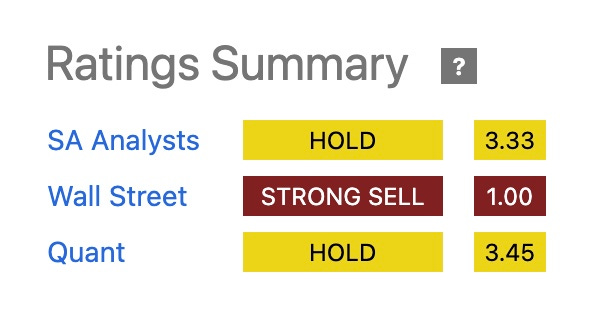

At current levels, I don’t see any meaningful catalyst capable of driving sustained upside. Moreover, Wall Street rates them a strong sell.

Instead, I believe shares are likely to:

Trade rangebound

Continue underperforming peers

Potentially make new 52-week lows

I think this continues until financial performance stabilizes.

There Are Some Positives 👍🏾

To be fair, Prospect Capital does still have some strengths.

Positives:

Very low leverage compared to peers

Strong liquidity profile

Low non-accrual rates

Reduced exposure to riskier sectors like Software

Portfolio becoming more defensive

Leverage stood at just 0.38x, well below many peers.

The company also maintains:

$1.8B in undrawn revolver capacity

$4.6B in total liquidity

Those metrics help reduce immediate balance sheet risk.

However, balance sheet strength alone isn’t enough to offset declining earnings and NAV deterioration.

Risks & Bottom Line ✅

Prospect Capital’s latest quarter further strengthens my bearish thesis.

While the:

Double-digit yield

Deep discount to NAV

Defensive portfolio repositioning

all may look attractive on the surface; the ongoing financial deterioration remains difficult to ignore.

Could the strategic shift eventually improve performance? Possibly.

But I don’t expect meaningful earnings accretion or financial stabilization for at least another year or two.

And until investors see:

Stable NAV

Improved dividend coverage

Stronger income generation

Consistent financial execution

I believe the stock remains a high-risk value trap.

For now, I continue reiterating PSEC as a sell.

Would you consider PSEC for the short term to capture the dividend? Let me know in the comments.

Just a note to let readers know I will be going paid soon. Be on the lookout for the article laying out the details. Feel free to provide any feedback!

Happy Investing!

☎️ If you’re looking to create passive income and build your wealth from one of the top-rated analysts, book a call (Let’s Talk Investing or Detailed Portfolio Review) with me to get started.

If you’re looking to start investing check out our investment group over on Seeking Alpha.

Here’s How: Click the Seeking Alpha link here. Click investing group, subscribe now (GET AN INVESTING GROUP FREE TRIAL), or the blue hyperlink in my bio.

Not financial advice. For educational purposes only. I am not a licensed professional. Do your own due diligence.

Like & subscribe if you’re active duty, a veteran, or just love investing.