A Buy The Dip 10% Yielding BDC For Passive Income Investors

"The BDC Sell-Off Makes This 10% Yielder A Buy For Income"

As you know by my name, I love dividends. And in addition to sharing on here, I write regularly on the investment platform- Seeking Alpha.

My goal there is to teach everyday investors about building wealth, so they won’t to need to work to traditional retirement age.

I want to help you take control of your life, have F.I.R.E.

Here at Dividend Collection Agency the goal is to give investors and/or readers a different perspective. We take a simple approach to building wealth. And although investing may seem easy, people often miss opportunities by over complicating it.

But we are here to help.

Current Price: $18.43

Dividend/Yield: $0.46/ 10%

Right now is one of the more interesting environments I’ve seen in a while as an income-focused investor.

On one hand, volatility has picked up, uncertainty is rising, and macro risks continue to build. On the other hand, that same volatility is finally creating better entry points across income-producing assets—something we didn’t have much of in 2024 and early 2025.

But as always, it’s important to remember: with higher reward often comes higher risk.

And that’s exactly how I’m approaching today’s market.

While I do think there are opportunities starting to emerge, I’m still being selective. I’m not rushing back into every high-yield name just because prices have come down. Instead, I’m focusing on quality first—and valuation second.

That brings me to the BDC sector (BIZD).

Why I’ve Been Cautious on BDCs ⚠️

If you’ve followed me for a while, then you already know I’ve been cautious on Business Development Companies for some time now.

In fact, I exited all of my BDC positions back in early 2025. At the time, my thinking was simple:

• Interest rates had likely peaked

• BDC earnings were near a cyclical high

• And forward returns looked less attractive

Since then, that thesis has largely played out.

But now we have a new variable in the equation: geopolitical risk.

The ongoing war with Iran has added another layer of uncertainty to the market. While this doesn’t directly impact BDCs in the way it might impact energy or defense stocks, the indirect effects are what matter most.

Wars tend to be inflationary. Inflation complicates the Federal Reserve’s policy decisions. And when the Fed is stuck between fighting inflation and supporting growth, the result is often economic instability.

That instability is where the risk comes in for BDCs.

Because at the end of the day, BDCs lend to businesses—many of which are smaller, leveraged, and more vulnerable during economic downturns.

So while higher rates can support income, they can also increase default risk.

That’s the balancing act.

Revisiting Sixth Street Specialty Lending (TSLX) 📝

I last looked into TSLX about six months ago. At the time, I acknowledged the company’s strong fundamentals, but I remained cautious due to sector-wide headwinds.

Specifically, I was concerned about their heavy exposure to floating-rate loans. With over 96% of their portfolio tied to floating rates, a decline in base rates was almost guaranteed to pressure earnings.

And that’s exactly what we’ve seen.

Since then, TSLX has underperformed, declining more than 25%, while the broader market—as represented by the S&P 500 (SP500)—has remained relatively flat.

But here’s where things start to shift.

Despite that underperformance, the core of the business has remained intact.

Breaking Down the Latest Earnings 💵

Looking at TSLX’s most recent results, we see a company that is clearly feeling the impact of lower rates—but not breaking under the pressure.

Net investment income came in at $0.52 per share, down slightly from the prior quarter and down more meaningfully year-over-year. That decline was expected given the rate environment.

For the full year, NII declined from $2.33 to $2.18. On the surface, that might look concerning, but context matters.

Even with that decline, TSLX still generated enough income to comfortably cover its dividend.

The company paid out $1.99 in dividends, resulting in coverage of roughly 113%. That’s a very healthy margin, especially in a declining rate environment.

From an income investor’s perspective, this is exactly what you want to see:

• Earnings may fluctuate

• But the dividend remains supported

That said, not everything was perfect.

One area that stood out to me was the sequential decline in total investment income. Revenue dropped slightly quarter-over-quarter, and investment activity slowed compared to the prior year.

Commitments and funding were both down meaningfully on a year-over-year basis. While some of that can be attributed to a more cautious lending environment, it still signals slower growth.

And over time, growth matters.

Portfolio Trends & Credit Quality 📊

Another area I always focus on when analyzing BDCs is portfolio quality.

This is where TSLX continues to separate itself from many peers.

Non-accruals remain below 1%, which tells us that the vast majority of borrowers are still performing. Additionally, the company continues to focus heavily on first-lien loans, which sit at the top of the capital structure and offer greater protection.

However, there are some subtle shifts worth watching.

The company’s NAV declined slightly both quarter-over-quarter and year-over-year. While not alarming on its own, consistent NAV erosion can sometimes signal underlying pressure in the portfolio.

For comparison, peers like Ares Capital (ARCC) and Capital Southwest (CSWC) have shown more stability—or even growth—in their NAV over the same period.

That doesn’t mean TSLX is in trouble. But it does reinforce the idea that this is not a risk-free environment.

If economic conditions worsen, we could see:

• Higher non-accruals

• Increased risk ratings

• Pressure on earnings

For now, though, those risks remain manageable.

A Strong Balance Sheet Provides Flexibility ⚖️

One of the biggest reasons I’m comfortable revisiting TSLX is its balance sheet.

The company is operating with a debt-to-equity ratio of 1.10x, which is below the sector average. That gives management room to maneuver if conditions tighten.

Liquidity is also strong, with over $1.1 billion in available capacity. Near-term debt maturities are limited, and the next major maturity after August isn’t until 2028.

That level of flexibility matters more than ever in today’s environment.

It allows the company to:

• Maintain dividend stability

• Take advantage of new opportunities

• Navigate potential downturns

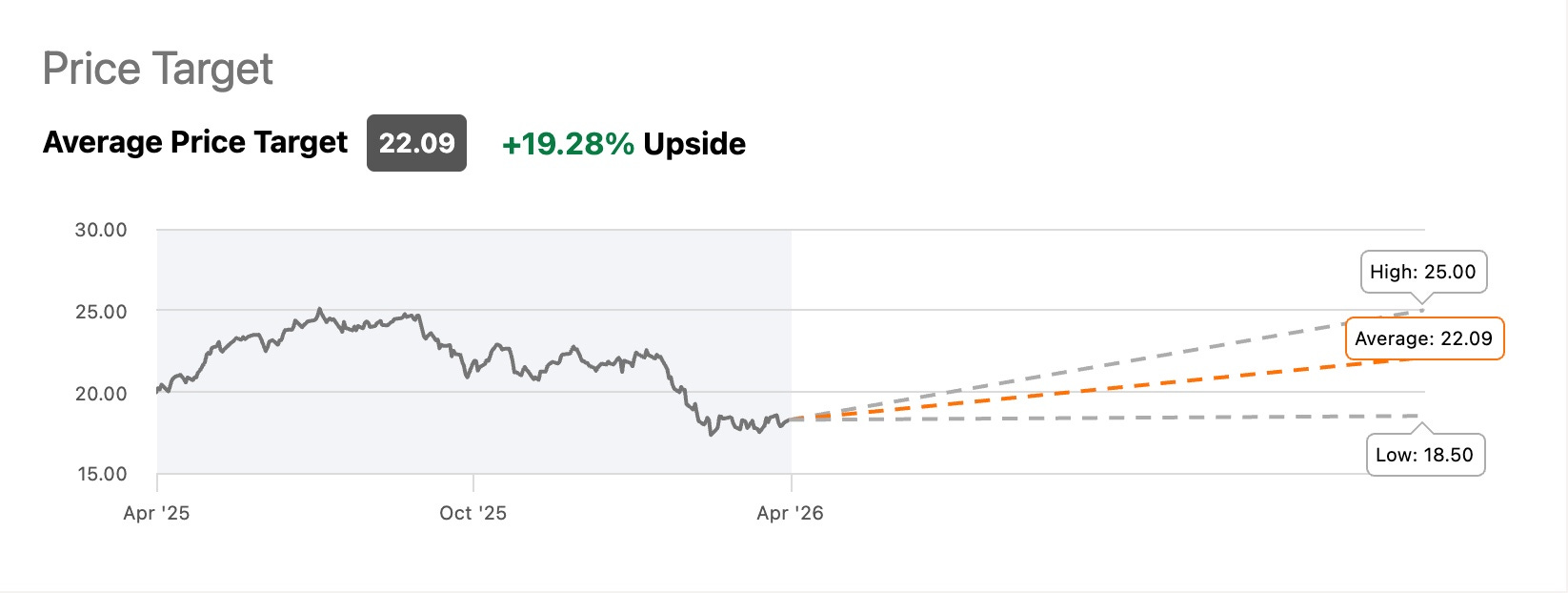

Valuation Has Finally Reset

Perhaps the most important shift—and the reason for my upgrade—is valuation.

Historically, TSLX has traded at a significant premium to NAV, often exceeding 20%. At one point, the stock traded at nearly 1.45x NAV.

Today, that premium has compressed to roughly 5–8%.

That’s a major change.

And it’s what transforms TSLX from a “wait and see” name into a potential buying opportunity.

You’re now getting:

• The same high-quality platform

• The same disciplined underwriting

• But at a much more reasonable price

Bottom Line

I want to be clear—I’m still cautious on the BDC sector overall.

There are real risks in this market:

• Ongoing geopolitical tensions

• Inflation uncertainty

• Rising recession probabilities

And BDCs, by nature, are more sensitive to economic stress.

But investing isn’t about avoiding risk altogether. It’s about being compensated for the risk you take.

With TSLX, I believe you are.

A ~10% yield, supported by strong coverage and a solid balance sheet, combined with a significantly reduced premium, creates a much more balanced risk/reward profile.

This is a classic case of:

👉 Quality name + better price = opportunity

Not a “load the boat” moment.

Not a “no-brainer” buy.

But a disciplined, income-focused entry point.

If you’re building an income portfolio, this is the type of position that makes sense to start—or slowly add to.

Because at the end of the day:

You’re getting paid to wait.

Let me know in the comments.

Happy Investing!

☎️ If you’re looking to create passive income and build your wealth from one of the top-rated analysts, book a call (Let’s Talk Investing or Detailed Portfolio Review) with me to get started.

If you’re looking to start investing check out our investment group over on Seeking Alpha.

Here’s How: Click the Seeking Alpha link here. Click investing group, subscribe now, or the blue hyperlink in my bio.

Not financial advice. For educational purposes only. I am not a licensed professional. Do your own due diligence.

Like & subscribe if you’re active duty, a veteran, or just love investing.