A Dividend King That Has Delivered Real Returns For More Than 50 Years!

"Amidst The AI Hype & Gold Rush, Altria Continues To Deliver Income"

As you know by my name, I love dividends. And in addition to sharing on here, I write regularly on the investment platform- Seeking Alpha.

My goal there is to teach everyday investors about building wealth, so they won’t to need to work to traditional retirement age.

I want to help you take control of your life, have F.I.R.E.

Here at Dividend Collection Agency the goal is to give investors and/or readers a different perspective. We take a simple approach to building wealth. And although investing may seem easy, people often miss opportunities by over complicating it.

But we are here to help.

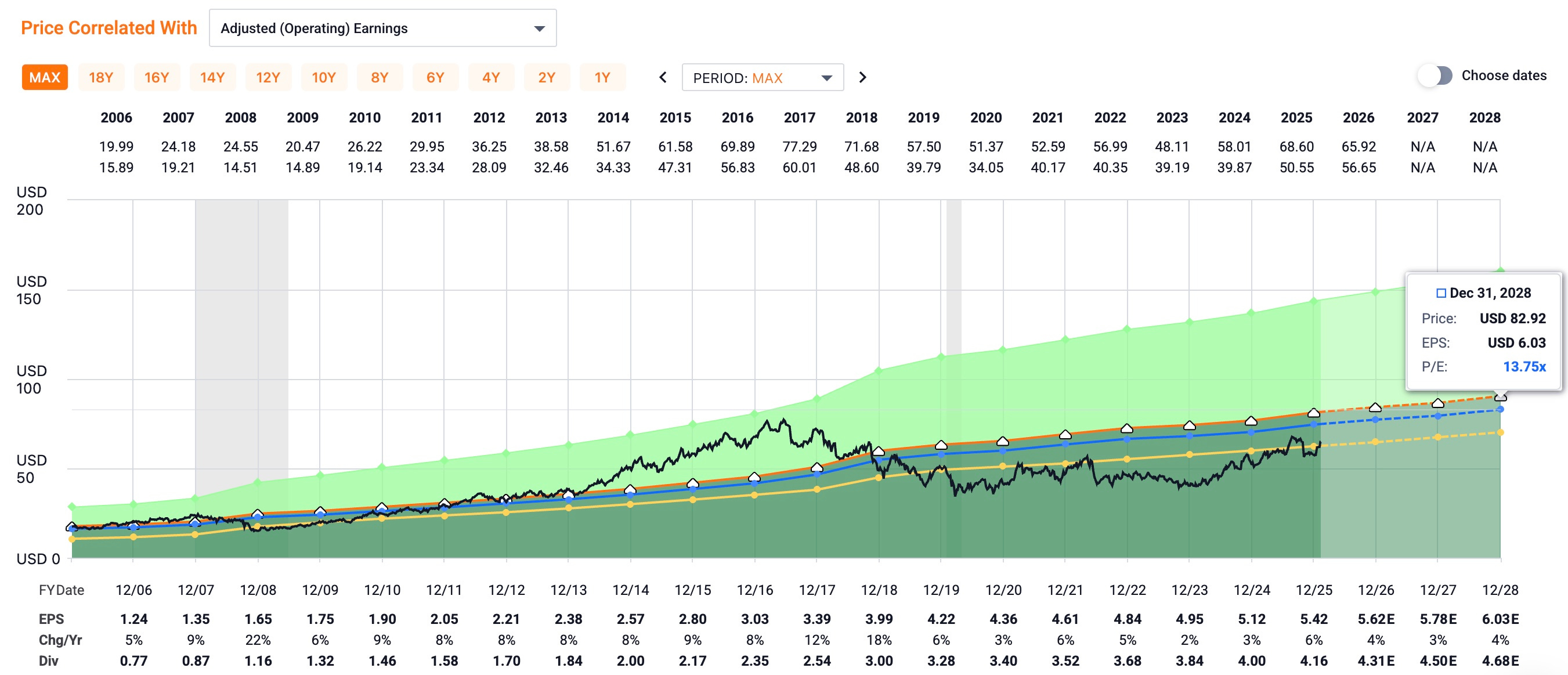

Current Price: $65.41

Portfolio Purpose: Income 💰

With AI enthusiasm still dominating headlines, it’s easy to overlook companies with real staying power.

Altria Group (MO) is one of them — quietly delivering income, stability, and market-beating returns while investors chase the next big thing.

Altria closed out the year with another “MO-like” quarter: mixed results, steady execution, and resilient cash flows.

Despite continued declines in traditional smoking, pricing power, buybacks, and progress toward a smoke-free portfolio keep the long-term thesis intact.

I believe MO is positioned to deliver another year of double-digit total returns in 2026.

Another MO-Like Quarter ⚖️

Q4 results were mixed but consistent with expectations. EPS of $1.30 missed estimates by $0.02, while revenue beat by $50 million, coming in at $5.08 billion. Both revenue and EPS declined sequentially, though year-over-year results were relatively stable.

The pressure continues to come from lower cigarette volumes, down 6.5% sequentially. That said, the rate of decline has improved from last year’s ~8%, suggesting some stabilization.

Pricing power remains the offset — Marlboro prices rose $0.67 year-over-year to $9.87 per pack, underscoring the inelastic nature of the business.

Oral tobacco revenue increased 2% despite lower volumes, again driven by pricing.

Smoke-Free Transition Gaining Traction 🚬

In December, Altria received FDA approval for six on! PLUS nicotine pouch products — an important milestone in its shift toward a smoke-free portfolio.

While Philip Morris’ (PM) ZYN continues to dominate the category, Altria’s oral pouch market share increased by 10.4 points year-over-year.

The acquisition of Another Snus Factor - the LOOP acquisition, and the expected launch of on! PLUS in the first half of 2026 should support incremental growth over time, even as competitive pressures remain.

A Well-Covered 6.6% Yield 💵

Altria’s 6.6% dividend yield is backed by one of the strongest shareholder-return frameworks in the market. The company has increased its dividend for 60 consecutive years, supported by aggressive share repurchases and disciplined leverage.

In 2024, Altria returned $10.2 billion to shareholders via dividends and buybacks. In 2025, that figure dropped to $8 billion, preserving roughly $2 billion in cash flow.

Leverage improved to 2.0x EBITDA, squarely within management’s target range, with $1 billion remaining under the current buyback authorization.

2026 Outlook 👀

Management guided to 2026 EPS of $5.56–$5.72, representing ~4% growth year-over-year. While modest, combining mid-single-digit earnings growth with a near-7% yield creates a clear path to double-digit total returns — especially if buybacks continue at the current pace.

Valuation & Risks ⚠️

MO trades at roughly 11x forward earnings, a discount to its historical multiple. The key upside catalyst remains NJOY.

If Altria can successfully resolve the legal issues and relaunch NJOY at scale, upside over the next several years becomes more compelling with a price target of $83 by the end of 2028.

If you’re looking for a stock analyzer tool that gives you future price targets based on historical data, use my code to get 25% off of Fast Graphs, my go to the stock analyzer tool for research.

Absent NJOY progress, I expect shares to trade in a $58–$65 range — but investors are well-paid to wait.

Bottom Line ✅

Altria continues to prove why it remains a core income holding. A near-7% yield, 60 years of dividend growth, strong pricing power, and disciplined capital allocation provide income reliability in a market dominated by AI and precious metals.

As fixed-rate yields eventually compress toward 3%, value-oriented income stocks like MO should regain attention. Until then, investors can collect a reliable dividend and position for another year of solid, market-beating returns.

With traditional smoking on the decline, do you think Altria is a sustainable income investment? Let me know in the comments.

Happy Investing!

☎️ If you’re looking to create passive income and build your wealth from one of the top-rated analysts, book a call (Let’s Talk Investing or Detailed Portfolio Review) with me to get started.

If you’re looking to start investing check out our investment group over on Seeking Alpha.

Here’s How: Click the Seeking Alpha link here. Click investing group, subscribe now, or the blue hyperlink in my bio.

Not financial advice. For educational purposes only. I am not a licensed professional. Do your own due diligence.

Like & subscribe if you’re active duty, a veteran, or just love investing.