A Highly Cyclical, High Growth Stock That Could Worth Adding To A Diversified Portfolio

"General Electric's Runway For Growth Appears Long"

As you know by my name, I love dividends. And in addition to sharing on here, I write regularly on the investment platform- Seeking Alpha.

My goal there is to teach everyday investors about building wealth, so they won’t to need to work to traditional retirement age.

I want to help you take control of your life, have F.I.R.E.

Here at Dividend Collection Agency the goal is to give investors and/or readers a different perspective. We take a simple approach to building wealth. And although investing may seem easy, people often miss opportunities by over complicating it.

But we are here to help.

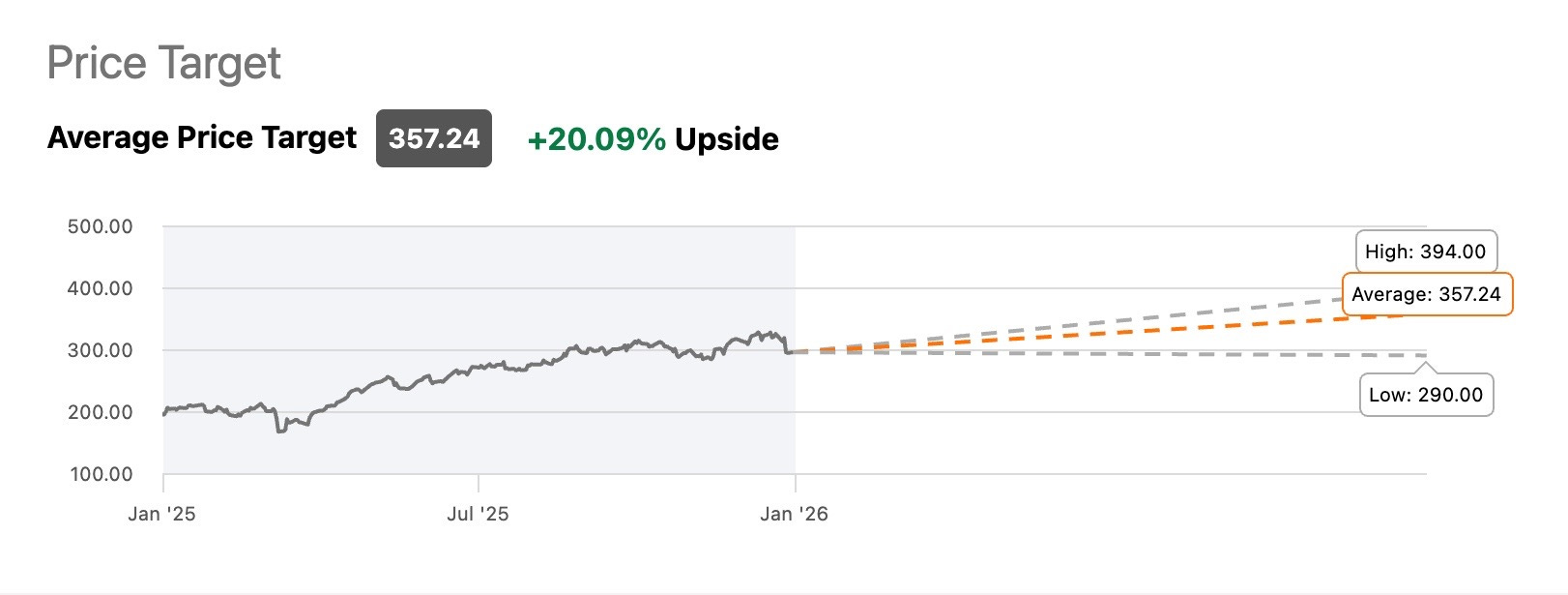

Current Price: $297.47

Portfolio Purpose: Growth 📉

When investors think about high-growth stocks, General Electric Company (GE) doesn’t always come to mind. Especially, among dividend growth investors.

Its highly cyclical nature, combined with a sub-0.5% yield, likely explains why it’s rarely mentioned in dividend-focused discussions.

However, GE stock has been on fire lately. Shares are up more than 47% over the past year, and in my view, the growth runway remains long.

Despite its cyclicality, I believe GE deserves consideration within a diversified, growth-focused portfolio, particularly for investors willing to tolerate volatility in exchange for long-term upside.

In this article, I review GE’s latest earnings, outlook, dividend safety, and valuation—and explain why, despite its elevated P/E ratio, I rate the stock a Buy.

Brief Overview ✈️

General Electric is now a pure-play aerospace company, designing and servicing aircraft engines for commercial airlines and defense customers. I’m personally familiar with GE, as the company also builds engines for U.S. Navy ships and U.S. military aircraft.

Founded in 1892, GE went public that same year. In 2021, the company announced plans to break itself into three independent businesses:

GE Aerospace

GE Vernova Inc. (GEV)

GE HealthCare Technologies Inc. (GEHC)

That transformation culminated in 2024, when GE Aerospace officially became a standalone entity. Today, the company operates through two segments:

Commercial Engines & Services (CES)

Defense & Propulsion Technologies (DPT)

Strong Q4 Performance ↗️

GE reported Q4 earnings this week and delivered what I consider a strong finish to the year, even though the stock briefly sold off following the report. In my opinion, the pullback had little to do with fundamentals and more to do with profit-taking after a powerful rally.

Orders surged 74%, while both revenue and earnings grew at double-digit rates. Revenue came in at $11.9 billion, beating analyst estimates by roughly $700 million. EPS totaled $1.57, exceeding expectations by $0.14.

While EPS declined modestly from the prior two quarters ($1.66), it still showed clear improvement from Q1’s $1.49, and revenue continued its steady sequential climb.

For the full fiscal year:

Revenue rose 21% to $42.3 billion

EPS increased from $4.60 to $6.37

Growth was driven primarily by strong equipment and service demand, reflected in rising order volumes.

Segment Highlights 📊

CES: Revenue grew 35%, supported by a 35% increase in orders and double-digit service growth

DPT: Revenue rose 11%, while orders increased 19%

As a result, segment profits climbed:

CES profits: +26% to $8.9 billion

DPT profits: +22% to $1.3 billion

Performance across both segments was supported by GE’s FLIGHT DECK initiative, launched in 2024. This lean-manufacturing framework is designed to improve efficiency, reduce costs, and enhance operational execution.

GE also benefited from continued investment in its MRO network and LEAP engines:

LEAP deliveries increased 28% in FY25

Commercial engine deliveries rose 25%

Defense engine deliveries climbed 30%

Overall, this was a very strong quarter and a strong year.

2026 Outlook

GE initiated guidance that points to continued double-digit growth, even as comparisons become more challenging.

EPS guidance: $7.10–$7.40 (midpoint growth of ~14%)

Revenue growth: Low double-digits

LEAP deliveries: Expected to increase 15%, down from ~25% previously

While growth is expected to moderate from 2025’s exceptional pace, momentum remains strong heading into 2026.

If interest rates continue to decline—as I expect—GE could see additional tailwinds through lower financing and operating costs. This may allow management to raise guidance in future quarters.

Dividend Safety 💵

GE’s dividend yield, currently below 0.5%, is likely why the stock is rarely discussed among dividend investors. However, this overlooks the fact that GE is very much a dividend growth stock.

The company recently raised its dividend 28.6%, increasing the payout to $0.36 per share. That hike reflects strengthening fundamentals and improving cash-flow visibility.

FY25 free cash flow grew from $6.2 billion to ~$7.7 billion

For 2026, management expects ~6.5% FCF growth, with 100% conversion

For comparison, peer The Boeing Company (BA) has not generated consistent free cash flow since 2023, with Q3 FCF of just $0.2 billion.

GE also plans to continue share repurchases, further enhancing per-share cash flow and dividend capacity.

Payout Math 🧮

Shares outstanding: ~1.068 billion, expected to decline to 1.050 billion in 2026

2025 dividend payments: ~$1.54 billion

FCF coverage: ~20% payout ratio

This leaves GE with ample room for future double-digit dividend increases.

Liquidity is also solid:

Cash & equivalents: $12.4 billion

Total debt: $20.5 billion

Market cap: >$300 billion

Valuation & Upside Potential 📉

With shares up nearly 47% over the past year, valuation is a valid concern.

Using midpoint guidance, GE trades at a forward P/E of ~40.7x, slightly below its five-year average of ~42x. On a PEG basis, the stock still appears attractive given its growth profile.

Based on consensus estimates, GE offers approximately 21% upside from current levels.

Looking ahead, I believe:

Lower interest rates

Rising aircraft utilization

Increased defense spending

All of these could support continued delivery growth and earnings expansion over the next 1–2 years.

Risks ⚠️

GE’s primary risks include:

A near-term price correction after a strong run

Geopolitical uncertainty

Operational or safety issues related to engine platforms

Because the stock is cyclical, any market-wide correction or slowdown in orders could introduce volatility. Investors should be prepared for pullbacks and consider adding opportunistically on weakness.

Bottom Line ✅

That said, despite short-term risks, I continue to view General Electric as a Buy for long-term investors. With strong fundamentals, expanding cash flows, a conservative payout ratio, and a long growth runway, GE has earned its place in a diversified, growth-focused portfolio.

Do you believe in GE’s growth runway? Let me know in the comments.

Happy Investing!

☎️ If you’re looking to create passive income and build your wealth from one of the top-rated analysts, book a call (Let’s Talk Investing or Detailed Portfolio Review) with me to get started.

If you’re looking to start investing check out our investment group over on Seeking Alpha.

Here’s How: Click the Seeking Alpha link here. Click investing group, subscribe now, or the blue hyperlink in my bio.

Not financial advice. For educational purposes only. I am not a licensed professional. Do your own due diligence.

Like & subscribe if you’re active duty, a veteran, or just love investing.