A Relatively New BDC Yielding 12% And Trading At A Discount To NAV

"MSIF's Discount And Double-Digit Yield May Be Attractive For Income-Focused Investors"

As you know by my name, I love dividends. And in addition to sharing on here, I write regularly on the investment platform- Seeking Alpha.

My goal there is to teach everyday investors about building wealth, so they won’t to need to work to traditional retirement age.

I want to help you take control of your life, have F.I.R.E.

Here at Dividend Collection Agency the goal is to give investors and/or readers a different perspective. We take a simple approach to building wealth. And although investing may seem easy, people often miss opportunities by over complicating it.

But we are here to help.

Current Price: $12.10

Dividend/Yield: $0.35/11.45%

Although the BDC sector has significantly underperformed recently, improving long-term setups across much of the space, I remain cautious overall despite being an income-focused investor.

Many business development companies now trade at steep discounts to net asset value, creating potentially attractive opportunities for patient investors. However, in my opinion, economic conditions continue to weaken, and that remains my biggest concern.

Ongoing geopolitical tensions, persistent inflation, tightening lending spreads, and growing uncertainty surrounding AI and automation risks — particularly for BDCs with higher software exposure — could continue pressuring the sector moving forward.

And this is especially concerning for smaller or less fundamentally sound BDCs, where borrower stress could lead to additional downside.

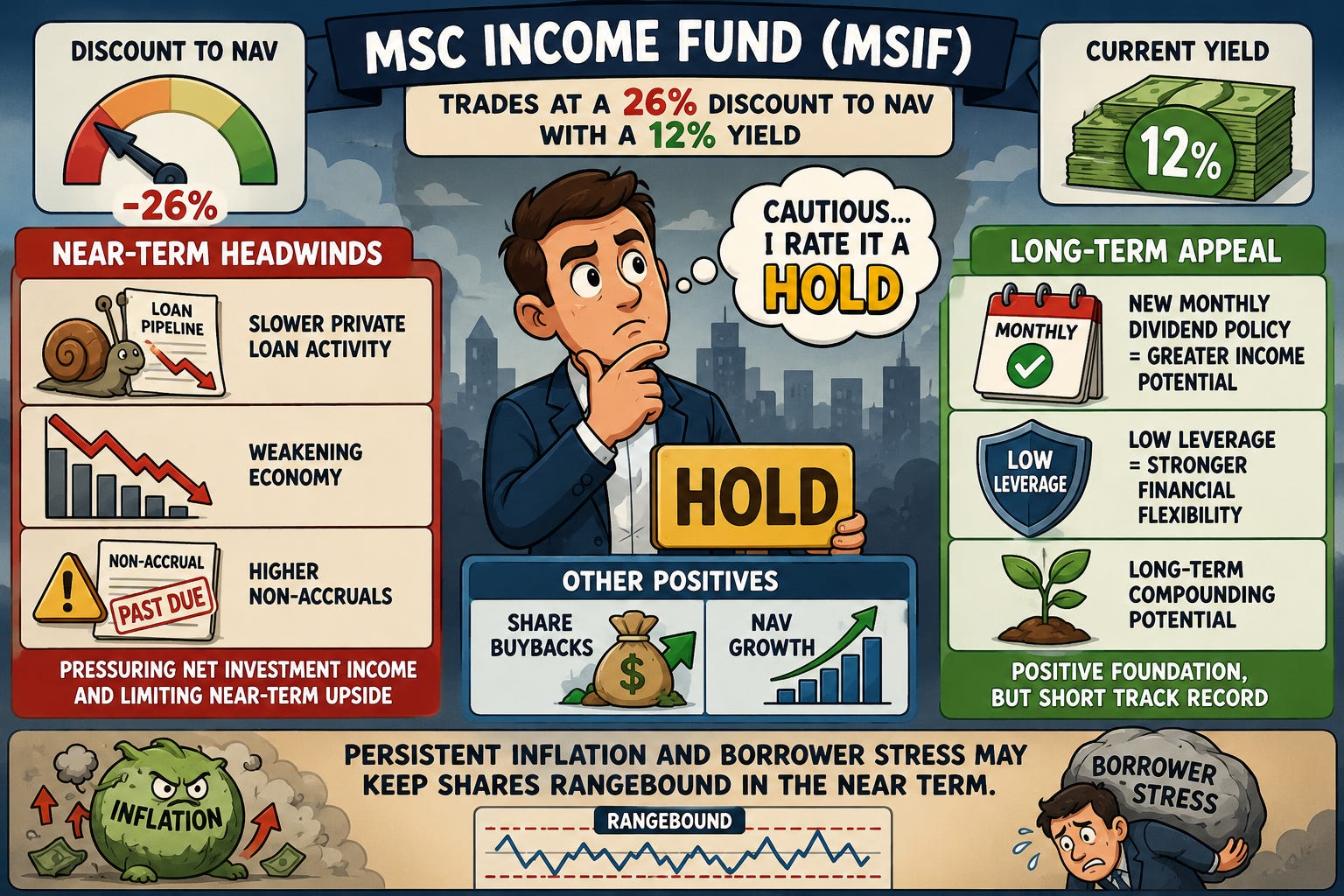

One name that continues to stand out for both its opportunity and risk is MSC Income Fund (MSIF).

Despite the company trading at a massive 26% discount to NAV while yielding roughly 12%, I continue to rate shares a hold.

Slower Private Loan Activity 🐢

MSC Income Fund reported Q1 2026 earnings in early May and generated adjusted net investment income of $0.34 per share after taxes, down from $0.38 on an annualized basis.

In my opinion, the decline largely reflects slowing activity within the company’s private loan portfolio.

One thing I pay particularly close attention to when analyzing BDCs is growth in total net investment income dollars rather than strictly per-share figures. Temporary factors such as repayments or special dividends can distort short-term per-share results.

Year-over-year, total net investment income declined approximately $0.2 million to $16.6 million, while total investment income rose 3% to $34.1 million.

To me, this suggests portfolio conditions may be weakening beneath the surface.

Management also highlighted slower deal activity in the private loan portfolio, which represents approximately 60% of the overall investment portfolio.

During the quarter, the company reported:

$7.5 million in unrealized losses

A partially offsetting $3.1 million gain from an equity investment exit

$55 million invested into the private loan portfolio

A net portfolio increase of just $17 million

For comparison, during the same quarter last year, management deployed approximately $138 million, resulting in an $89 million net increase.

That’s a meaningful slowdown.

The lower middle-market portfolio performed somewhat better, increasing by approximately $5.1 million to a fair value of $508 million.

In my opinion, the weakening economy is likely a major reason for the slower activity, particularly within private lending markets where borrower caution remains elevated.

While management expects deal flow to improve later this year, I personally don’t expect a significant acceleration unless macro conditions materially improve.

Monthly Dividends Could Become A Long-Term Catalyst 💵

The decline in adjusted NII also resulted in tighter dividend coverage, as earnings failed to fully cover the quarterly dividend.

Dividend income declined approximately $1.6 million year-over-year due primarily to weaker lower middle-market equity distributions and fewer non-recurring items.

However, management announced a potentially important long-term catalyst during the quarter: a transition to monthly dividends.

The company will now follow a structure similar to notable BDCs such as Capital Southwest (CSWC) and Trinity Capital (TRIN).

Beginning in July, investors will receive monthly dividends of $0.11 plus a $0.03 supplemental payment, maintaining a total quarterly payout of $0.36.

Long term, I believe this could improve investor sentiment and increase the stock’s appeal among income-focused investors who prioritize monthly cash flow.

Management also stated future supplemental payouts will likely remain tied to earnings performance, which introduces some flexibility into the payout structure moving forward.

Conservative Balance Sheet Remains A Strength ⚖️

One of the more attractive aspects of MSC Income Fund remains the balance sheet.

Net debt-to-equity increased modestly to 0.88x from 0.74x during my previous coverage but leverage still remains well below the peer average of approximately 1.29x.

That conservative capital structure provides the company with meaningful flexibility should economic conditions deteriorate further.

Debt maturities also remain manageable:

Only $150 million matures in 2026

No additional maturities occur until 2029

This should help support dividend stability near term even if portfolio earnings weaken modestly.

NAV Growth & Buybacks ↗️

Net asset value continued improving as NAV per share rose from $15.35 to $15.87 year-over-year and increased modestly from the prior quarter.

Importantly, management repurchased approximately $16 million worth of shares during the quarter, contributing roughly $0.08 to NAV growth.

Given the deep discount to NAV, continued buybacks could become an important long-term driver of shareholder value.

In my opinion, management will likely continue taking advantage of the discount if shares remain depressed.

Attractive Long-Term Setup, But Risks Remain Elevated ⚠️

There’s certainly a bullish case for MSC Income Fund.

A 12% yield combined with a 26% discount to NAV is difficult to ignore for income-oriented investors.

The balance sheet remains conservative, monthly dividends may improve investor demand, and ongoing buybacks could gradually support NAV growth and eventual price appreciation.

However, I still believe the near-term risks outweigh the rewards.

Economic conditions continue weakening, borrower stress remains elevated, and tighter credit conditions could pressure portfolio performance further over the coming quarters.

Non-accruals currently stand at:

4.2% on a cost basis

1.1% on a fair value basis

While these levels are still manageable, further economic deterioration could push them meaningfully higher.

And if that happens, earnings, NAV stability, and dividend coverage could all come under pressure simultaneously.

Bottom Line ✅

Although the recent BDC selloff has improved long-term setups across much of the sector, I remain cautious overall.

MSC Income Fund possesses several attractive qualities including:

A steep discount to NAV

A double-digit yield

Conservative leverage

Monthly dividend payments

Share buybacks supporting NAV growth

However, the company’s short track record combined with growing macroeconomic uncertainty keeps me hesitant for now.

From an income perspective, I absolutely understand why investors may find shares attractive at current levels.

But in my opinion, ongoing economic weakness and rising borrower stress could continue limiting upside in the near term.

For now, I continue to rate MSC Income Fund a hold.

Do you think MSIF can navigate current headwind and recover over the long term? Let me know in the comments.

Just a note to let readers know I will be going paid soon. Be on the lookout for the article laying out the details. Feel free to provide any feedback!

Happy Investing!

☎️ If you’re looking to create passive income and build your wealth from one of the top-rated analysts, book a call (Let’s Talk Investing or Detailed Portfolio Review) with me to get started.

If you’re looking to start investing check out our investment group over on Seeking Alpha.

Here’s How: Click the Seeking Alpha link here. Click investing group, subscribe now (GET AN INVESTING GROUP FREE TRIAL), or the blue hyperlink in my bio.

Not financial advice. For educational purposes only. I am not a licensed professional. Do your own due diligence.

Like & subscribe if you’re active duty, a veteran, or just love investing.