A Wonderful Business At The Wrong Price

"Even The Highest Quality Businesses Can Underperform"

As you know by my name, I love dividends. And in addition to sharing on here, I write regularly on the investment platform- Seeking Alpha.

My goal there is to teach everyday investors about building wealth, so they won’t to need to work to traditional retirement age.

I want to help you take control of your life, have F.I.R.E.

Here at Dividend Collection Agency the goal is to give investors and/or readers a different perspective. We take a simple approach to building wealth. And although investing may seem easy, people often miss opportunities by over complicating it.

But we are here to help.

Current Price: $215.59

Dividend/Yield: $0.945/1.59%

Waste Management (WM), in my opinion, is one of the highest-quality businesses on the planet — and for good reason.

Despite another mixed earnings report that included a revenue miss, the company once again demonstrated the resilience investors have come to expect from this industry leader.

Even with softer volumes in one of its key segments, WM still delivered double-digit EBITDA growth and strong free cash flow expansion.

Looking ahead, management continues to expect approximately 29% free cash flow growth in 2026 based on previous guidance, which could support long-term share appreciation and continued dividend growth.

However, at a forward P/E approaching 27x, I believe valuation remains the primary near-term risk.

While Waste Management absolutely deserves to trade at a premium due to its dominant moat and recession-resistant business model, I currently see little margin of safety at today’s price.

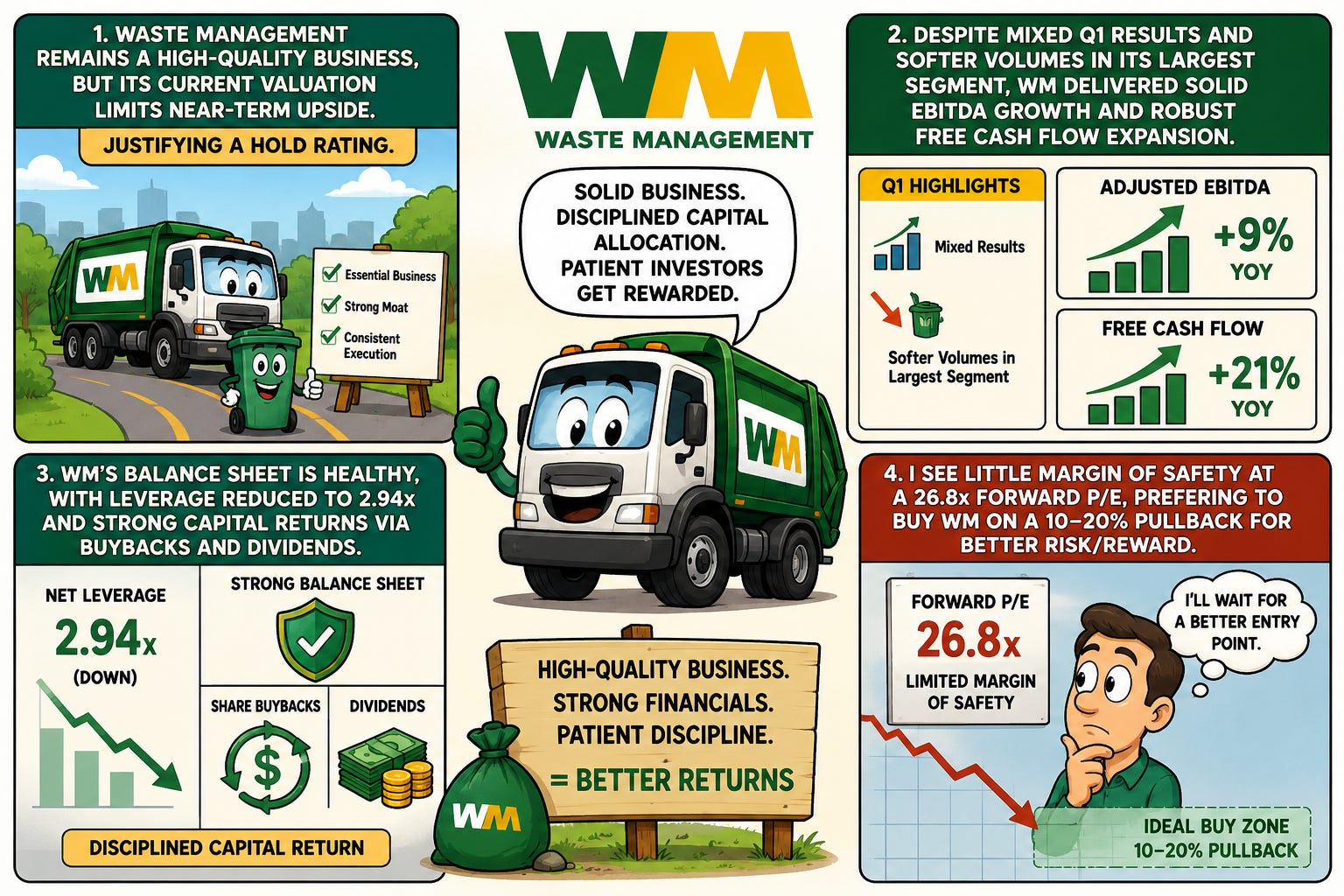

In this article, I discuss Waste Management’s latest earnings, fundamentals, valuation, and why I continue to rate shares a hold despite the company’s exceptional quality.

Softer Volumes Led To Mixed Q1 Results 📊

Waste Management reported first-quarter earnings on April 29th, once again producing mixed results.

This time, however, the company managed to beat EPS expectations by $0.07.

Adjusted earnings per share came in at $1.87, up from $1.67 during the prior year quarter. Net income increased 8.6% year-over-year to $731 million.

Revenue, however, missed estimates by approximately $60 million, totaling $6.23 billion.

Even so, top-line growth remained respectable, increasing 3.5% year-over-year despite a slowing economy and weaker volumes within their largest segment: Collection & Disposal.

Volumes within the segment declined 1.5% during the quarter.

Management attributed the weakness primarily to winter weather impacts and difficult comparisons from elevated wildfire-related activity during the prior year.

Despite lower volumes, Collection & Disposal operating EBITDA still increased 6.4%, although it was the slowest-growing segment during the quarter. Margins also expanded by 110 basis points.

Management noted during the earnings call that they expect volume trends to improve throughout the year due to seasonality and the lapping of lower-margin contract losses.

Outside of Collection & Disposal, results were stronger.

The Renewable Energy segment delivered the highest EBITDA growth, increasing 18% year-over-year.

Meanwhile, Healthcare Solutions posted 12% EBITDA growth.

Both segments also experienced margin expansion, improving 50 and 20 basis points respectively.

Overall, I would describe the quarter as solid.

The softer volumes likely explain part of the stock’s recent underperformance, but management believes the weakness is temporary rather than structural.

Strong Free Cash Flow Growth Continues 💵

One of the more encouraging developments for long-term dividend investors was the continued strength in free cash flow generation.

This follows approximately 27% free cash flow growth during 2025.

During Q1, free cash flow nearly doubled from $475 million to $920 million.

The primary driver was a 22% year-over-year decline in CAPEX spending.

Capital returns also remained aggressive.

Waste Management repurchased $344 million worth of shares during the quarter while returning approximately $730 million to shareholders in total.

Dividends accounted for just $385 million of that amount, leaving the payout ratio at a very conservative 42%.

This gives WM substantial flexibility to continue increasing shareholder returns while still investing in growth opportunities and strengthening the balance sheet.

For 2026, management still expects approximately $2 billion in share repurchases.

Balance Sheet Remains Healthy ⚖️

At the end of 2025, Waste Management’s leverage ratio increased to 3.1x — slightly above management’s long-term target range of 2.5x to 3.0x.

However, during Q1, leverage improved to 2.94x, bringing the company back within its targeted range.

For comparison:

Waste Connections (WCN): 2.75x leverage

Republic Services (RSG): 2.6x leverage

Although WM’s leverage remains somewhat elevated relative to peers, the company’s ability to deleverage while continuing aggressive shareholder returns is encouraging.

Long-term debt declined modestly to $22.2 billion compared to $22.8 billion during the prior-year quarter.

Short-term debt stood at just $641 million after management repaid over $1 billion in commercial paper debt that matured in March.

Importantly, upcoming debt maturities remain manageable, with September maturities carrying a weighted-average interest rate of just 2.6%.

Combined with strong retained cash flow and liquidity, Waste Management remains in an excellent position to pursue tuck-in acquisitions while continuing shareholder returns.

Premium Valuation Leaves Little Margin Of Safety 🤔

While Waste Management absolutely deserves to trade at a premium valuation, I believe the current multiple remains difficult to justify from a risk/reward perspective.

Over the last year, shares have declined approximately 6% after previously approaching a 52-week high near $250 per share.

At roughly 26.8x forward earnings, I believe investors are receiving very little margin of safety.

And while I still expect shares to trend higher over the long term due to strong free cash flow generation and consistent execution, I personally would prefer adding closer to the $190–$200 range.

Even the highest quality businesses bought at the wrong price can lead to potential underperformance.

If you’re looking for a stock analyzer tool that gives you future price targets based on historical data, use my code to get 25% off of FAST Graphs, my go-to the stock analyzer tool for research.

According to FAST Graphs, shares still appear overvalued even after the recent pullback, trading above their fair-value multiple of approximately 22.2x earnings.

Personally, I believe a fair valuation range for a company of WM’s quality is between 22x and 24x forward earnings.

Using a discounted cash flow model, I arrive at a similar conclusion.

Based on analyst estimates, WM is expected to grow earnings approximately 10.5% annually over the next five years.

To remain conservative, I assume:

8% long-term earnings growth thereafter

A 12% required rate of return

Long-term returns above the historical S&P 500 average

Using those assumptions, I arrive at an intrinsic value estimate of approximately $225 per share.

At the current price near $219, that leaves investors with less than 3% upside potential based on my estimates.

Risks ⚠️

Waste Management remains one of the premier businesses in the market today.

Its dominant moat, recurring revenue stream, and essential business model make it one of the more reliable long-term compounders available for dividend investors.

However, I believe that same quality has pushed valuation to levels that currently leave investors with little room for error.

As a result, valuation remains the biggest near-term risk in my opinion.

If the broader market experiences another sell-off, I believe Waste Management could easily see additional downside despite its strong fundamentals.

Bottom Line ✅

Long term, I fully expect shares to continue trending higher.

But over the near-to-medium term, I currently do not see a major catalyst capable of driving significant multiple expansion from current levels.

For investors seeking a more attractive risk/reward setup, I believe waiting for a 10%–20% pullback offers a much better opportunity.

Outside of valuation, I have very few complaints regarding the business itself.

Waste Management remains a premier company with excellent execution.

But for now, I continue to rate shares a hold.

Do you think Waste Management is currently overpriced? Where would you buy at? Let me know in the comments.

Just a note to let readers know I will be going paid soon. Be on the lookout for the article laying out the details. Feel free to provide any feedback!

Happy Investing!

☎️ If you’re looking to create passive income and build your wealth from one of the top-rated analysts, book a call (Let’s Talk Investing or Detailed Portfolio Review) with me to get started.

If you’re looking to start investing check out our investment group over on Seeking Alpha.

Here’s How: Click the Seeking Alpha link here. Click investing group, subscribe now (GET AN INVESTING GROUP FREE TRIAL), or the blue hyperlink in my bio.

Not financial advice. For educational purposes only. I am not a licensed professional. Do your own due diligence.

Like & subscribe if you’re active duty, a veteran, or just love investing.