Altria's Strong Performance Has Caused Its Margin Of Safety To Shrink

"But The 5.7% Dividend Yield Is Still Attractive In An Inflationary Environment"

As you know by my name, I love dividends. And in addition to sharing on here, I write regularly on the investment platform- Seeking Alpha.

My goal there is to teach everyday investors about building wealth, so they won’t to need to work to traditional retirement age.

I want to help you take control of your life, have F.I.R.E.

Here at Dividend Collection Agency the goal is to give investors and/or readers a different perspective. We take a simple approach to building wealth. And although investing may seem easy, people often miss opportunities by over complicating it.

But we are here to help.

Current Price: $72.79

Dividend/Yield: $1.06/5.78%

Altria (MO) just reported Q1 earnings, and if you’ve followed the company long enough, you already know the story.

It was another resilient, steady, and predictable quarter.

Despite ongoing macro uncertainty, inflation pressures, and the continued secular decline in traditional smoking, Altria once again demonstrated why it remains a staple in many income portfolios.

They beat on both the top and bottom line, expanded margins, and continued executing on their smokeless transition strategy.

But here’s the key question:

👉🏾 After a 23% run over the past year… how much upside is really left?

Q1 Results: Beating Expectations Again 📊

Altria delivered a double-beat quarter:

EPS: $1.32 (beat by $0.07)

Revenue: $4.76B (beat by ~$180M)

Year-over-year growth:

EPS: +7.3%

Revenue: +3.2%

While both metrics declined sequentially, the year-over-year growth tells the real story — the business remains stable and continues to grind higher.

For comparison, peer Philip Morris International (PM) posted stronger growth, but at a significantly higher valuation — reinforcing Altria’s positioning as the more income-focused, value-oriented play.

The Transition Story: Smokeless Is Working 🔄

One of the most important aspects of Altria’s long-term thesis is its ability to successfully transition away from combustible products.

And this quarter provided more evidence that progress is being made.

Key Highlights:

on! nicotine pouch volumes: +18% YoY

Shipments: 46 million cans

on! PLUS: Expanded to nationwide distribution

Retail share: Slight YoY dip, but sequential improvement

This matters because:

👉🏾 Smokeless products are no longer just a “future story”

👉🏾 They are actively offsetting declines in cigarettes today

At the same time, traditional cigarette volume declines are moderating:

Reported decline: -2.4%

Adjusted decline: ~-5%

Prior year comparison: -12%

That’s a meaningful improvement and suggests the worst of the volume contraction may be behind us.

Pricing Power & Margin Expansion 💪🏾

Altria continues to lean on one of its greatest strengths:

Pricing power

Price increases of ~3% helped offset volume declines

Operating income (OCI): +6.3% YoY

Margins expanded from 64.4% → 65.1%

This is what makes Altria unique.

Even in a declining volume environment, the company can:

✔ Raise prices

✔ Maintain margins

✔ Generate consistent cash flow

Dividends & Buybacks: The Core Investment Case 💰

Let’s be clear — this is still an income-first story.

Q1 Capital Returns:

Dividends paid: $1.8B

Buybacks: $280M (4.5M shares)

Remaining authorization: ~$720M

Key Metrics:

Dividend yield: ~6%

Payout ratio: ~85%

The slightly reduced buyback activity is likely due to the higher share price, but the strategy remains intact:

👉🏾 Buybacks + dividends = shareholder return machine.

And as long as cash flow remains stable, the dividend appears secure in the near term.

Balance Sheet: Quietly Strengthening ⚖️

Altria continues to improve its financial position:

Leverage ratio: 1.9x (down from 2.1x)

Debt: ~$24B

Cash: ~$3.5B

Management retired over $1B in debt recently, which adds flexibility going forward.

This gives them room to:

Continue buybacks

Support dividend growth

Navigate macro uncertainty

The Macro Risk: Inflation Is a Double-Edged Sword ⚠️

Here’s where the story gets more nuanced.

The Bull Case:

Higher yields attract income investors

Defensive names tend to hold up better

“Bond proxy” behavior supports demand

The Bear Case:

Higher gas & living costs reduce disposable income

Consumers trade down to discount products

Premium brands (like Marlboro) lose share

We’re already seeing signs of this:

Marlboro retail share: -1.4 points YoY

Discount segment gaining share

Management citing pressure on lower-income consumers

Inflation helps the stock narrative…but hurts the consumer behavior.

That tension could drive near-term volatility.

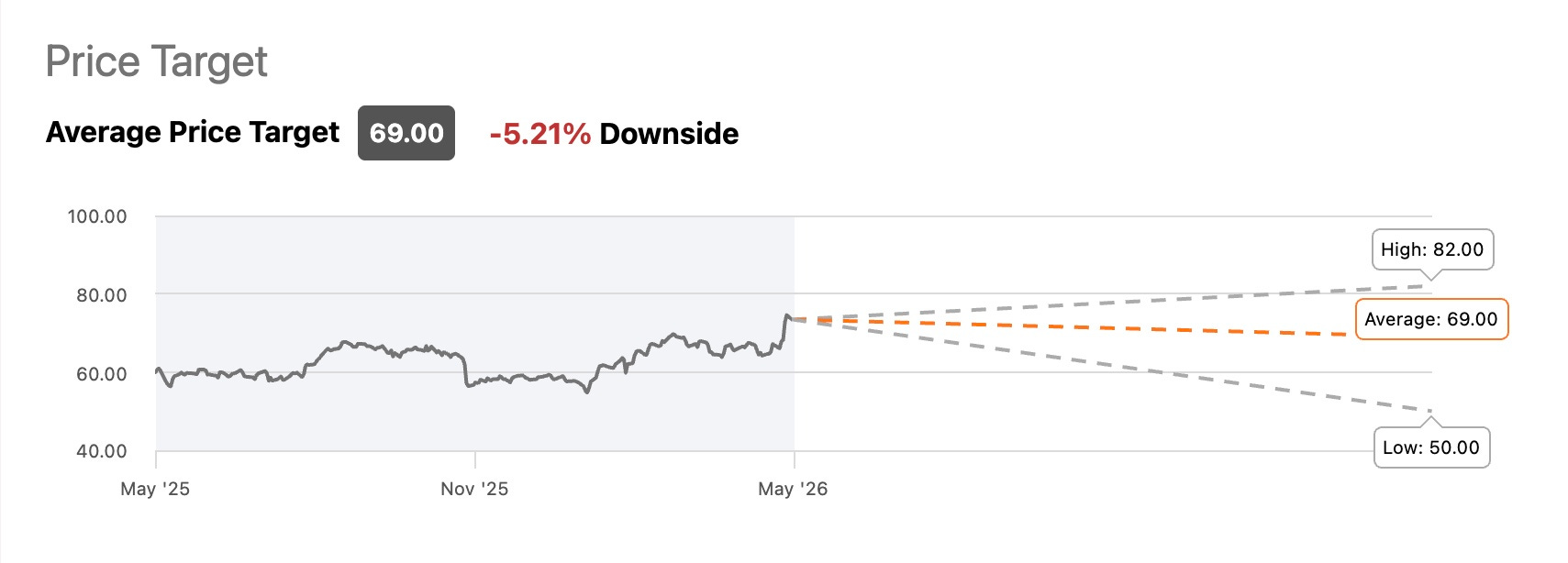

Valuation: Still Cheap… But Less Compelling 💵

From a valuation standpoint, Altria still looks attractive:

Forward P/E: ~12.9x

Peer comparison: Philip Morris International (PM): ~19.5x

But valuation alone doesn’t drive returns.

After a strong rally:

The margin of safety has shrunk

Expectations have increased

Downside risk is more visible

Outlook: Steady, Not Explosive 🔮

Management reaffirmed full-year guidance:

EPS: $5.56 – $5.72

Growth: ~4%

Altria continues to check all the boxes:

✔ Strong cash flow

✔ Reliable dividend

✔ Pricing power

✔ Improving balance sheet

✔ Progress in smokeless products

But investing is about timing and risk/reward, not just quality.

Bottom Line ✅

Despite the strong quarter and solid fundamentals:

The stock is up ~23% over the past year

Trading near highs

Facing increasing macro headwinds

I now see more downside risk than upside in the near term.

That doesn’t mean sell.

It means:

👉🏾 Be patient

👉🏾 Collect the dividend

👉🏾 Wait for a better entry point

Altria remains one of the most reliable income plays in the market.

But after the recent run…

…The easy money has likely already been made (for now).

Do you hold Altria? What is your cost basis? Let me know in the comments.

Just a note to let readers know I will be going paid soon. Be on the lookout for the article laying out the details. Feel free to provide any feedback!

Happy Investing!

☎️ If you’re looking to create passive income and build your wealth from one of the top-rated analysts, book a call (Let’s Talk Investing or Detailed Portfolio Review) with me to get started.

If you’re looking to start investing check out our investment group over on Seeking Alpha.

Here’s How: Click the Seeking Alpha link here. Click investing group, subscribe now (GET AN INVESTING GROUP FREE TRIAL), or the blue hyperlink in my bio.

Not financial advice. For educational purposes only. I am not a licensed professional. Do your own due diligence.

Like & subscribe if you’re active duty, a veteran, or just love investing.