Can Nike Get Back To Their Glory Days?

"The 3% Dividend Yield Is An Incentive While You Wait For The Turnaround"

As you know by my name, I love dividends. And in addition to sharing on here, I write regularly on the investment platform- Seeking Alpha.

My goal there is to teach everyday investors about building wealth, so they won’t to need to work to traditional retirement age.

I want to help you take control of your life, have F.I.R.E.

Here at Dividend Collection Agency the goal is to give investors and/or readers a different perspective. We take a simple approach to building wealth. And although investing may seem easy, people often miss opportunities by over complicating it.

But we are here to help.

Current Price: $51.24

Dividend/Yield: $1.64/3.20%

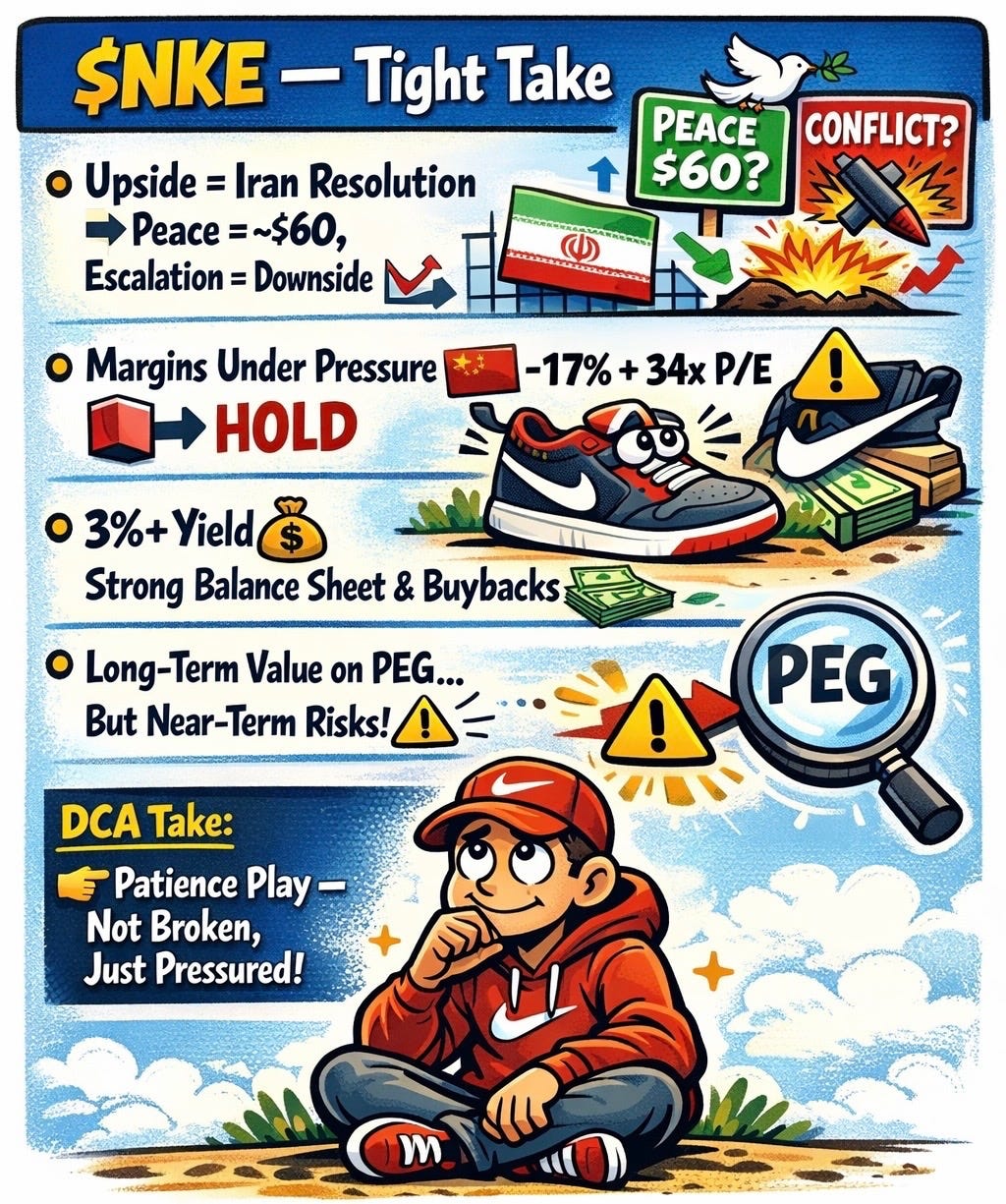

Nike, Inc. (NKE) has been a frustrating hold for investors. Despite its dominance as a global brand, the stock has significantly underperformed over the past decade, weighed down by slowing growth, rising competition, and persistent macro headwinds.

While the company is actively working through a turnaround, I believe meaningful upside remains at least 12–24 months away.

That said, if execution improves and macro conditions stabilize, there is a path toward $60 by year-end.

What Went Wrong ✏️

Nike’s struggles aren’t due to one issue—they’re layered:

Growth slowdown following a strong 2015–2021 run

Margin compression, with gross margins falling ~300 basis points to 40.6%

International weakness, particularly in Greater China (-17%)

Soft demand in legacy brands like Converse

Rising competition from both premium and niche athletic brands

The result: a once high-growth story now facing a reset period.

Recent Performance: Mixed Signals 🚦

Nike’s latest quarter showed signs of stabilization—but not enough to change the narrative.

EPS: $0.53 (beat by $0.16)

Revenue: $12.4B (+1% YoY, beat expectations)

North America: Strength driven by resilient consumer spending

International: Continued weakness, led by China

Despite the beat, the market remained unconvinced—and the stock continued to slide.

Macro Is Driving the Bus 🚌

Recent volatility has less to do with Nike—and more to do with the broader environment.

The ongoing geopolitical tensions involving Iran have:

Increased inflation concerns

Reduced expectations for rate cuts

Raised recession probabilities

For a consumer discretionary name like Nike, this is a direct headwind.

If rates stay higher for longer—or rise further—it delays the entire turnaround story.

What Could Change the Narrative 📖

Nike isn’t standing still. Several developments could improve sentiment:

Tariff relief following a favorable Supreme Court ruling → potential margin expansion

Partnerships with Apple Inc. (AAPL) (Beats) and SKIMS → brand momentum

Product innovation (Aero-Fit launch) tied to global events like the World Cup

International rollout of new product lines

These won’t fix fundamentals overnight—but they can rebuild investor confidence.

Q3 Preview: Expectations Are Low 📊

Nike reports Q3 earnings next week, and expectations are modest:

EPS: ~$0.30–$0.35 (decline from $0.53)

Revenue: ~$11.3B–$11.6B (down sequentially)

Margins: Additional pressure expected (175–225 bps impact)

The key variable isn’t the headline numbers—it’s international performance, especially China.

👉 If China stabilizes → stock likely rallies

👉 If weakness persists → downside risk remains

Dividend & Balance Sheet: The Safety Net ⚖️

One bright spot: income investors are getting paid to wait.

Dividend yield: ~3%

FCF payout ratio: ~70%

Credit rating: A-rated

Liquidity: ~$7B, matching long-term debt

Nike’s financial position remains strong, giving it flexibility to navigate the downturn.

Valuation: Still Not Cheap… But Interesting 💸

Forward P/E: ~33x (still elevated)

Peer comparison: Higher than lululemon athletica (~12x forward P/E)

PEG ratio: More attractive relative to history

This creates a split narrative:

Short-term: Expensive, limited upside

Long-term: Potentially attractive for risk-tolerant investors

Upside Scenario: Path to $60 📉

Nike doesn’t need perfection—it needs progress.

A realistic bullish path:

Sequential improvement in international markets

Stabilizing margins

Easing macro uncertainty (rate cuts or geopolitical resolution)

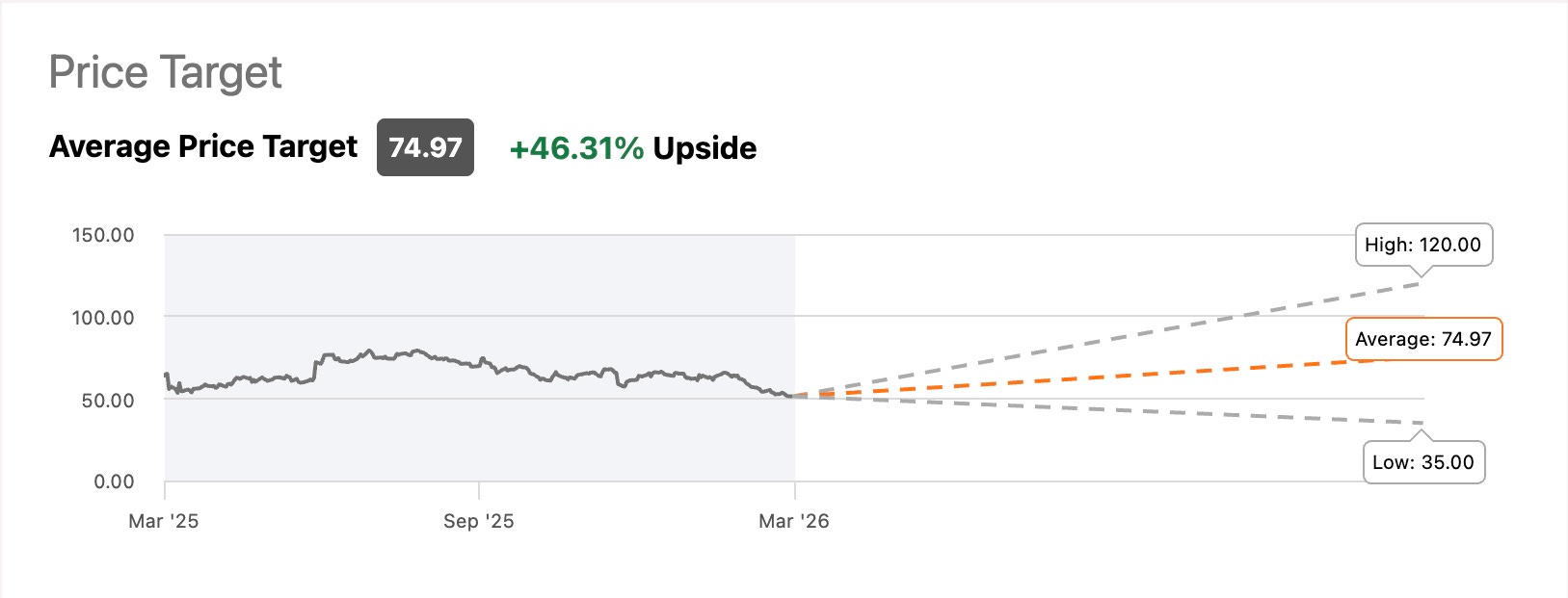

If those align, a move toward $60 is achievable. Long-term, NKE offers strong upside to their average price target of $75 set by Wall Street.

Risks to Watch ⚠️

Prolonged geopolitical conflict

Higher-for-longer interest rates

Continued China weakness

Consumer spending slowdown

Potential recession

These risks disproportionately impact discretionary companies like Nike.

DCA Take 🤔

Nike isn’t broken.

It’s in a transition phase, caught between:

A fading growth cycle

A rebuilding global strategy

And a difficult macro backdrop

For now, I remain neutral (Hold).

👉 Downside appears limited near-term

👉 Upside requires patience and macro improvement

For long-term investors with higher risk tolerance, Nike may be worth accumulating gradually—but expectations should remain grounded.

Bottom Line ✅

Nike is doing the right things operationally—but timing matters.

Until macro conditions improve and international growth stabilizes, the stock is likely to remain range-bound.

Patience is required.

How do you think Nike will recover? Let me know in the comments.

Happy Investing!

☎️ If you’re looking to create passive income and build your wealth from one of the top-rated analysts, book a call (Let’s Talk Investing or Detailed Portfolio Review) with me to get started.

If you’re looking to start investing check out our investment group over on Seeking Alpha.

Here’s How: Click the Seeking Alpha link here. Click investing group, subscribe now, or the blue hyperlink in my bio.

Not financial advice. For educational purposes only. I am not a licensed professional. Do your own due diligence.

Like & subscribe if you’re active duty, a veteran, or just love investing.