Collect A 4.4% Yield From This Dividend King

"Fixed-Rate Investments Like HYSA's, Money Markets, and CDs Offer Safety, But No Capital Appreciation"

As you know by my name, I love dividends. And in addition to sharing on here, I write regularly on the investment platform- Seeking Alpha.

My goal there is to teach everyday investors about building wealth, so they won’t to need to work to traditional retirement age.

I want to help you take control of your life, have F.I.R.E.

Here at Dividend Collection Agency the goal is to give investors and/or readers a different perspective. We take a simple approach to building wealth. And although investing may seem easy, people often miss opportunities by over complicating it.

But we are here to help.

Current Price: $104.85

Portfolio Purpose: Income 💰

In a market where risk-free yields remain attractive, income investors face a familiar question: Why take equity risk when I can earn 4%–5% with little volatility?

It’s a fair point. But while fixed-income offers stability, it lacks upside. That’s where high-quality REITs like Federal Realty Investment Trust (FRT) come into focus.

Federal Realty currently yields approximately 4.4% and is expected to generate total growth of roughly 6.8% this fiscal year, driven primarily by strong leasing activity and accretive acquisitions.

With interest rates likely to provide tailwinds over the next 12–24 months, I believe FRT offers a compelling mix of income stability and long-term total return potential.

In this article, I’ll review the latest quarter, assess the REIT’s fundamentals, and explain why this Dividend King looks positioned to deliver 8%–10% annualized returns going forward.

Revisiting the Prior Thesis 📖

I last covered Federal Realty Investment Trust on Seeking Alpha in October 2024 in an article titled, “A Dividend King Fit for Retirees.”

At the time, I highlighted FRT’s income reliability, improving occupancy, and upside potential toward a $129 price target, making it an attractive option for retirees seeking dependable income.

Since then, FRT has underperformed the S&P 500 (SP500), declining more than 9%, while the index gained roughly 21%.

This divergence has largely been driven by higher interest rates and volatility in long-term Treasuries — persistent headwinds for the REIT sector as a whole, including diversified vehicles like Real Estate Select Sector SPDR Fund (XLRE).

Despite this underperformance, fundamentals at Federal Realty have continued to improve.

Another Beat, Another Guidance Raise ↗️

Federal Realty reported Q3 earnings at the end of October and delivered its strongest leasing quarter in company history. Leasing activity totaled 727,000 square feet, significantly above last year’s 581,000 square feet. Annual cash rent increased 28%, and the company broke ground on a new residential development.

Funds from operations (FFO) came in at $1.77, beating consensus estimates by one cent and increasing $0.06 year over year. Revenue also exceeded expectations by $7 million, reaching $322.25 million, aided by contractual rent escalators.

Net operating income (NOI) grew 4.4%, up from 2.9% a year earlier. On a cash basis, NOI growth improved from 3.4% to 3.7%. From an operating standpoint, Federal Realty continues to fire on all cylinders.

During the quarter, the REIT acquired a town center in Maryland for $187 million at a 7% cap rate, anchored by Target Corporation (TGT) and Whole Foods Market. The property attracts more than 5 million visitors annually, highlighting the quality and durability of FRT’s portfolio.

Through the first three quarters of the year, Federal Realty completed 23 acquisitions totaling $2.3 billion, exceeding cumulative acquisitions since 2019. These assets carried a weighted-average occupancy of 88%, which temporarily weighed on overall portfolio occupancy.

As a result, occupancy dipped slightly year over year from 94% to 93.8%. However, as these newly acquired properties lease up, management expects occupancy, NOI, and FFO to trend higher.

Reflecting this momentum, management raised full-year FFO guidance once again. FFO is now expected to range between $7.05 and $7.11, representing 4.6% growth at the midpoint versus 2024.

Looking Ahead to Q4 👀

Federal Realty is expected to report Q4 earnings in mid-February. Management does not expect recent acquisitions to materially impact the upcoming quarter due to timing.

Consensus FFO estimates call for a range of $1.82 to $1.88, implying 4.5% growth from the prior year. I believe results could land closer to $1.80–$1.85, still reflecting solid underlying momentum.

Balance Sheet Remains a Strength ⚖️

Despite elevated acquisition activity, Federal Realty’s balance sheet remains conservatively positioned. Net debt to EBITDA stands at 5.6x, only slightly above management’s long-term target of 5.5x. Fixed-charge coverage improved year over year from 3.7x to 3.9x.

For context, FRT’s leverage is comparable to Brixmor Property Group (BRX), slightly higher than Kite Realty Group Trust (KRG), and materially lower than highly levered peers such as Macerich (MAC). Personally, I prefer REITs with leverage below 6.0x, and FRT comfortably fits that profile.

Liquidity totals approximately $1.3 billion, with 88% of debt fixed-rate. Importantly, the REIT generates an estimated $75–$100 million in free cash flow after dividends, providing ample flexibility for future growth initiatives.

A Rock-Solid 4.4% Dividend 💵

Federal Realty Investment Trust is a true Dividend King, having raised its dividend for nearly 60 consecutive years. The current dividend yields approximately 4.4%, and management last increased the payout by 3% in August to $1.13 per share.

Using midpoint guidance, the dividend payout ratio sits at a conservative 63.8%, leaving meaningful retained capital and room for continued dividend growth. Over the past 23 years, FRT has delivered an average annual total return of 9.1%, underscoring the quality of its assets and management discipline.

Valuation and Long-Term Upside 📈

At current levels, Federal Realty trades at approximately 14.6x forward P/FFO, modestly above its five-year average of 13.6x.

On the surface, this may suggest the stock is fairly valued. However, this average includes the pandemic period and an unusually restrictive interest-rate environment.

Given the company’s asset quality, balance sheet strength, and consistent growth profile, I believe FRT deserves to trade closer to 15x–17x FFO as interest-rate pressures ease.

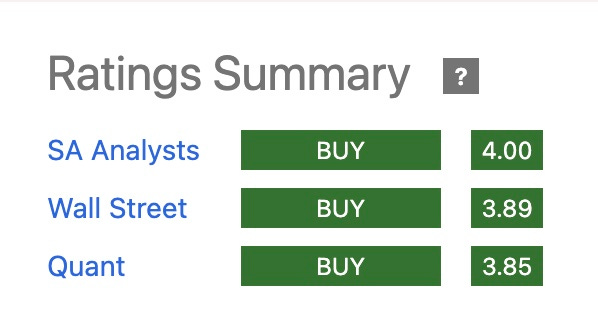

You can see below that us Seeking Alpha analysts, Wall Street, and Quant all agree that Federal Realty Trust is a buy.

If that rerating occurs alongside mid-single-digit FFO growth and a 4%+ dividend yield, investors could reasonably expect 8%–10% total returns over the next several years.

Risks ⚠️

Volatility in long-term Treasury yields remains the primary near-term risk and could continue to pressure REIT valuations. Additionally, any sustained deterioration in occupancy would likely weigh on sentiment and share price performance.

Bottom Line ✅

That said, Federal Realty’s strong leasing momentum, disciplined acquisition strategy, robust liquidity, and improving macro backdrop position the REIT well for the future. Investors are paid to wait with a reliable yield above 4%, while retaining exposure to meaningful upside.

What do you think of Federal Realty as an income play? Let me know in the comments.

Happy Investing!

☎️ If you’re looking to create passive income and build your wealth from one of the top-rated analysts, book a call (Let’s Talk Investing or Detailed Portfolio Review) with me to get started.

If you’re looking to start investing check out our investment group over on Seeking Alpha.

Here’s How: Click the Seeking Alpha link here. Click investing group, subscribe now, or the blue hyperlink in my bio.

Not financial advice. For educational purposes only. I am not a licensed professional. Do your own due diligence.

Like & subscribe if you’re active duty, a veteran, or just love investing.