Collect A 6%+ Yield From This Monthly Paying REIT

"Do You Own This REIT For Income?"

As you know by my name, I love dividends. And in addition to sharing on here, I write regularly on the investment platform- Seeking Alpha.

My goal there is to teach everyday investors about building wealth, so they won’t to need to work to traditional retirement age.

I want to help you take control of your life, have F.I.R.E.

Here at Dividend Collection Agency the goal is to give investors and/or readers a different perspective. We take a simple approach to building wealth. And although investing may seem easy, people often miss opportunities by over complicating it.

But we are here to help.

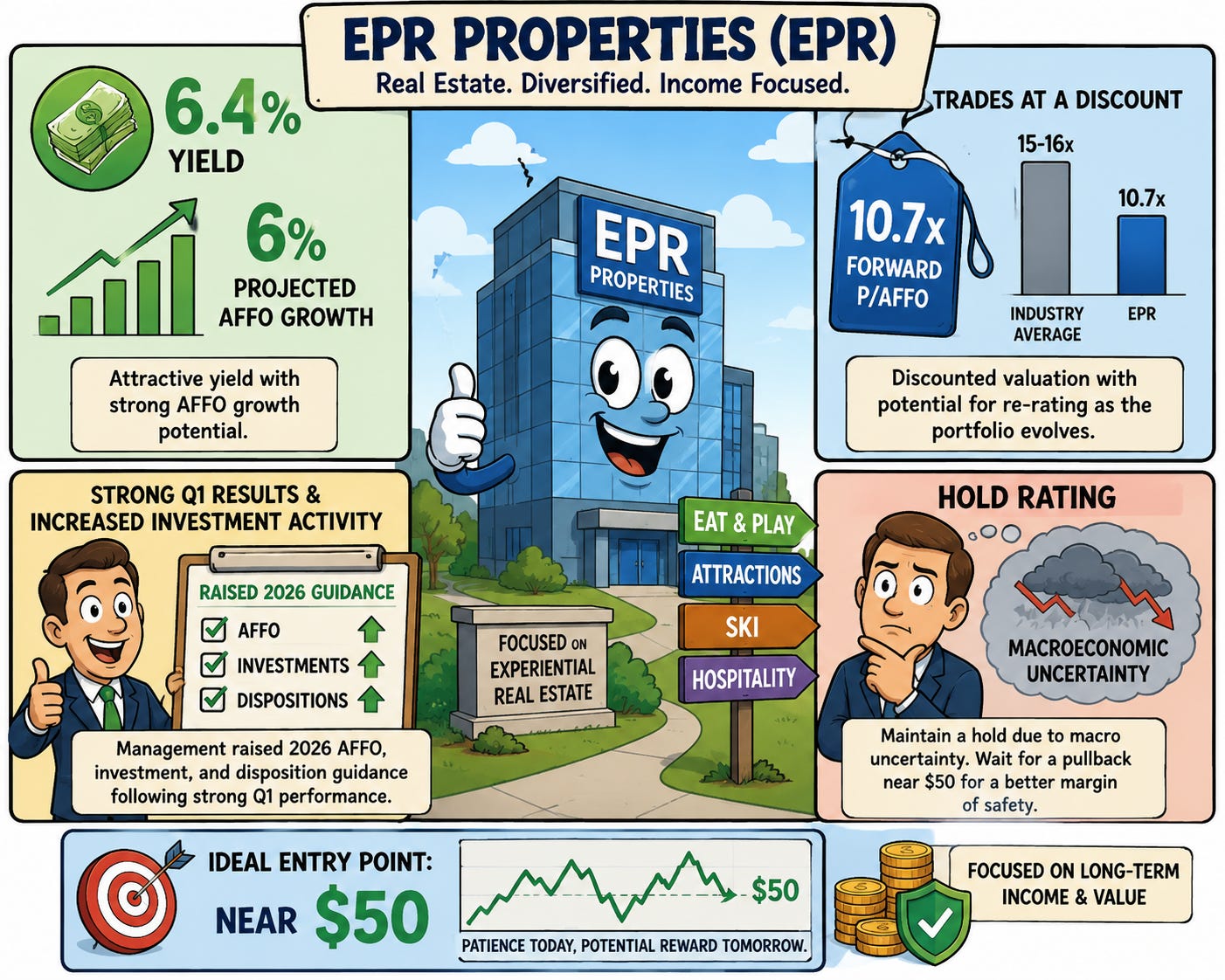

Current Price: $57.94

Dividend/Yield: $0.8975/6.4%

Year-to-date, the REIT (XLRE) sector has rallied roughly 10% as REITs continue recovering from one of the most difficult interest-rate environments in decades.

But despite the rally, I still believe there are select REIT opportunities offering attractive risk-adjusted upside potential for long-term income investors.

One name that continues standing out to me is Essential Properties Trust (EPR).

I downgraded EPR during my previous coverage, not because fundamentals were deteriorating, but because macroeconomic uncertainty combined with a strong share price rally reduced the margin of safety.

Today, I still believe EPR offers compelling long-term upside.

The company sports:

- A 6.4% dividend yield

- Roughly 6% projected AFFO growth

- A discounted valuation near 10.7x forward P/AFFO

- A well-covered monthly dividend

- Potential multiple expansion over the next 2–3 years

However, despite the attractive setup, I continue to reiterate shares at a hold rating due to persistent macro risks and the potential for better buying opportunities ahead.

Strong Quarter Continues Momentum 🏃🏾

EPR Properties delivered a strong Q1 report that helped reinforce the long-term investment thesis.

The company reported AFFO of $1.29 per share, beating expectations by $0.04. Revenue also came in ahead of estimates at approximately $181 million.

AFFO grew roughly 6% year-over-year while revenue increased 3.6%, supported by:

- Embedded rent escalators

- Higher investment spending

- Gains on real estate transactions

- Lower credit losses

Management also significantly accelerated investment activity during the quarter.

EPR invested $51.3 million and completed the previously announced acquisition with Six Flags Entertainment (FUN) involving seven experiential properties totaling approximately $315 million.

Importantly, this continues EPR’s transition away from theaters and toward broader experiential real estate categories.

That portfolio transition remains one of the most important aspects of the long-term bullish thesis.

Historically, the market has assigned EPR a discounted valuation due to concerns surrounding theater concentration and consumer discretionary exposure.

But as management continues diversifying into attractions, eat-and-play concepts, hospitality, and other experiential assets, I believe the market could gradually reward shares with a higher valuation multiple.

Raised Guidance Reinforces Confidence ↗️

One of the more encouraging developments from the quarter was management’s decision to raise guidance across several key areas.

EPR increased:

- AFFO guidance

- Investment guidance

- Disposition guidance

Management now expects approximately 6% AFFO growth, an increase from prior expectations closer to 4%–5%.

Investment guidance also increased substantially to a range of $500 million–$600 million, signaling management sees attractive opportunities despite the uncertain backdrop.

This is notable because it represents the highest level of activity the company has seen since the pandemic period.

In my opinion, this positions EPR well if interest rates continue trending lower over the next 6–12 months.

Lower financing costs combined with improving capital market conditions could allow experiential REITs like EPR to accelerate growth once again.

Dividend Remains Attractive 💵

One of the primary reasons income-focused investors continue gravitating toward EPR is the monthly dividend.

At current prices, shares yield approximately 6.4%, which remains attractive relative to many peers and fixed-income alternatives.

More importantly, the dividend remains well covered.

Using the midpoint of guidance, EPR’s AFFO payout ratio remains around 68%–70%, leaving a reasonable margin of safety.

The balance sheet also remains solid:

- Net leverage decreased to 4.8x

- Liquidity remains strong

- Over $1 billion remains available on the revolver

- Debt maturities remain manageable

While EPR doesn’t possess the same balance sheet strength as premium REITs like Agree Realty (ADC) or Realty Income (O), I still view the overall financial position as healthy.

Why I Believe Shares Could Re-Rate Higher 📉

From a valuation perspective, EPR still appears attractive.

Shares currently trade near 10.7x forward P/AFFO, well below many net lease and experiential REIT peers.

I don’t necessarily believe EPR deserves the same premium valuation as Realty Income or Agree Realty.

However, I do believe the current discount is excessive.

If management continues successfully diversifying the portfolio and maintaining steady growth, I think the market could eventually assign EPR an 11x–12x multiple over the medium term.

That alone could support a share price closer to their high price target of $66 from Wall Street over the next few years.

When combining:

- Potential valuation expansion

- A 6.4% yield

- Mid-single-digit AFFO growth

Investors could realistically see low-double-digit total return potential even without aggressive multiple expansion.

That’s a compelling setup for long-term income-oriented investors.

Why I Remain Cautious ⚠️

Despite the attractive long-term setup, I still believe caution is warranted.

My primary concern remains the macroeconomic environment.

The ongoing conflict in the Middle East continues creating inflationary risks, particularly through higher oil and energy prices.

If oil prices continue climbing, consumers could eventually begin pulling back discretionary spending.

That matters for EPR because experiential spending remains highly dependent on consumer confidence and disposable income.

Management highlighted healthy trends during the quarter, including:

- Strong box office performance

- Higher attendance trends

- Continued experiential spending growth

But these trends could weaken if inflation reaccelerates later this year.

And if consumer spending slows, EPR’s experiential-focused portfolio could experience temporary pressure.

This is why I continue preferring patience here despite the attractive yield and valuation.

Bottom Line ✅

Overall, I continue believing EPR Properties offers an attractive long-term investment case for income-oriented investors.

The combination of:

- A 6.4% dividend yield

- 6% projected AFFO growth

- Potential valuation expansion

- A transitioning portfolio

- A monthly dividend

makes the stock compelling over the long term.

However, macro uncertainty and inflation risks still create downside volatility potential in the near term.

For that reason, I continue preferring shares closer to the low-$50 range where investors can build a larger margin of safety and potentially enhance long-term total return potential.

For now, I reiterate shares at a hold.

Do you think EPR is a buy here or would you wait for a further pullback? Let me know in the comments.

Just a note to let readers know I will be going paid soon. Be on the lookout for the article laying out the details. Feel free to provide any feedback!

Happy Investing!

☎️ If you’re looking to create passive income and build your wealth from one of the top-rated analysts, book a call (Let’s Talk Investing or Detailed Portfolio Review) with me to get started.

If you’re looking to start investing check out our investment group over on Seeking Alpha.

Here’s How: Click the Seeking Alpha link here. Click investing group, subscribe now (GET AN INVESTING GROUP FREE TRIAL), or the blue hyperlink in my bio.

Not financial advice. For educational purposes only. I am not a licensed professional. Do your own due diligence.

Like & subscribe if you’re active duty, a veteran, or just love investing.