Collect Monthly Income From Real Estate With This Quality REIT

"Collect A 4% Monthly Yield"

As you know by my name, I love dividends. And in addition to sharing on here, I write regularly on the investment platform- Seeking Alpha.

My goal there is to teach everyday investors about building wealth, so they won’t to need to work to traditional retirement age.

I want to help you take control of your life, have F.I.R.E.

Here at Dividend Collection Agency the goal is to give investors and/or readers a different perspective. We take a simple approach to building wealth. And although investing may seem easy, people often miss opportunities by over complicating it.

But we are here to help.

Current Price: $

Portfolio Purpose: Income 💰

When it comes to retail net-lease REITs inside the Real Estate Select Sector SPDR Fund (XLRE), Agree Realty (ADC) continues to rank at the top in terms of balance sheet strength, tenant quality, and disciplined capital allocation.

Despite core FFO coming in merely in line with expectations this quarter, the bigger picture remains intact: steady growth, fortress-level credit metrics, and a clear runway for continued compounding.

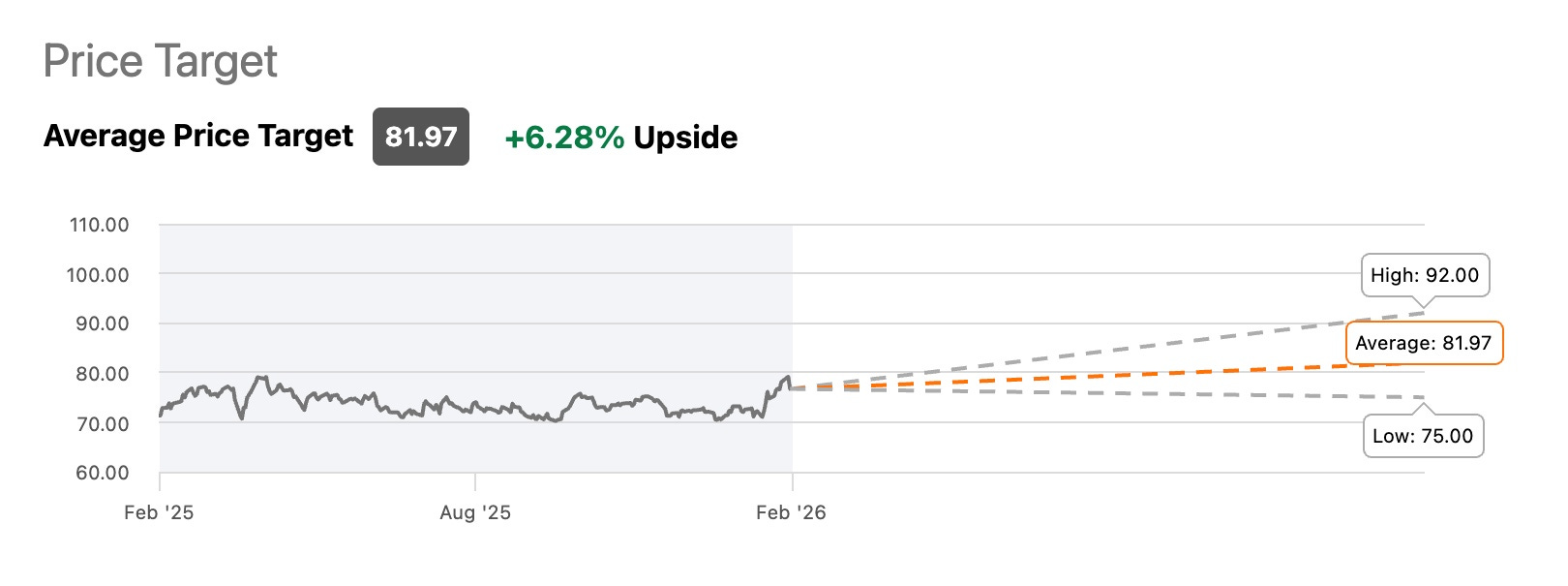

I continue to rate shares a Buy and believe a move toward $80+ by year-end 2026 is achievable.

Another Strong Quarter 💪🏾

Agree Realty reported Q4 core FFO of $1.10 per share, up 7.8% year-over-year. Revenue came in at $190.5 million, rising 18.6% from the prior year and slightly beating estimates.

For full-year 2025, core FFO grew from $4.08 to $4.28 per share, a 4.9% increase.

Growth was driven primarily by disciplined acquisition activity and contractual rent escalators — exactly what you want to see from a net-lease REIT operating in a higher-rate environment.

Acquisition Activity 🛍️

During Q4:

$347.4 million invested across 78 properties

7.1% weighted-average cap rate

9 dispositions at 6.4% cap rate

70 basis point spread achieved

For the full year, acquisitions totaled $1.44 billion across 305 properties, up meaningfully from 2024’s $951 million.

Property count grew to 2,674 properties, with approximately 67% investment-grade tenant exposure.

Top tenants include:

Walmart (WMT)

Tractor Supply Company (TSCO)

Dollar General (DG)

This is essential retail exposure with durable business models — a key reason ADC commands a premium.

Ground Leases: The Quiet Advantage 🚧

One of Agree Realty’s underappreciated strengths is its expanding ground lease portfolio.

251 total ground leases (up from 229 last year)

100% occupancy

9-year weighted average lease term

89% investment-grade tenants

10.2% of annualized base rent

Ground leases sit in a stronger capital position and typically carry lower risk profiles. Over time, this mix shift enhances portfolio durability and reduces volatility during downturns.

2026 Guidance: Off to a Strong Start 🏎️

Management initiated 2026 guidance calling for:

$1.4–$1.6 billion in acquisitions

AFFO between $4.54 and $4.58 per share

Midpoint growth of approximately 5.3%

That’s slightly above recent growth rates — and if interest rates decline meaningfully, I would not be surprised to see upward revisions later in the year.

Combine:

~5–6% AFFO growth

~4% dividend yield

And you have a credible path toward double-digit total returns.

A-Rated Balance Sheet = Competitive Edge ⚖️

Agree Realty’s recently achieved A credit rating is a major differentiator in today’s environment.

Key metrics:

No material debt maturities until 2028

Pro forma leverage: 3.8x

$2 billion in liquidity

~$714 million in forward equity

~$3.3 billion total debt

Lower leverage and strong liquidity give ADC flexibility when others may be forced to retrench. In a consolidating sector, cost-of-capital advantages matter.

The Monthly Compounding Machine 📠

ADC ended the year with an AFFO payout ratio of 71%, leaving ample retained capital for growth.

The annualized dividend sits at $3.081, and the company raised its dividend 3.6% year-over-year in 2025.

Agree typically increases the dividend twice annually, reinforcing its reputation as a consistent monthly compounder.

For income-focused investors — particularly retirees seeking reliable distributions — this level of coverage and growth is compelling.

Valuation & Upside Potential 📈

Shares currently trade around 16.7x forward AFFO, slightly above the five-year average of 15.6x. However, that five-year window includes the pandemic and prolonged higher-for-longer rate pressure.

If:

AFFO grows 5–6%

Acquisition spreads remain healthy

Rates trend lower

A re-rating toward 18x–20x AFFO is reasonable.

That implies a price range of approximately $82–$86 per share.

While I prefer accumulating shares below $70 when possible, the long-term risk/reward profile remains attractive.

Risks To Monitor ⚠️

The primary risks include:

Long-term Treasury volatility

A potential recession driven by labor market weakness

Occupancy deterioration (currently 99.7%)

Recent layoff activity and macro uncertainty bear watching. However, ADC’s high investment-grade tenant exposure and essential retail focus provide meaningful downside insulation.

Bottom Line ✅

Agree Realty isn’t the cheapest REIT in the sector — but quality rarely is.

With:

An A-rated balance sheet

Nearly 100% occupancy

Strong investment-grade tenant concentration

Growing ground lease exposure

Mid-single-digit AFFO growth

A well-covered 4% yield

I continue to view ADC as one of the highest-quality net-lease REITs available today.

If rates cooperate, $80+ by the end of 2026 looks well within reach. For long-term income investors focused on steady compounding, Agree Realty remains a core holding worthy of its premium.

Do you think Agree Realty is a buy here? Let me know in the comments.

Happy Investing!

☎️ If you’re looking to create passive income and build your wealth from one of the top-rated analysts, book a call (Let’s Talk Investing or Detailed Portfolio Review) with me to get started.

If you’re looking to start investing check out our investment group over on Seeking Alpha.

Here’s How: Click the Seeking Alpha link here. Click investing group, subscribe now, or the blue hyperlink in my bio.

Not financial advice. For educational purposes only. I am not a licensed professional. Do your own due diligence.

Like & subscribe if you’re active duty, a veteran, or just love investing.