🗓️ Economic Data For The Week

"Week of May 25th to May 29th"

My goal here is to teach everyday investors about building wealth, so they won’t to need to work to traditional retirement age.

I want to help you take control of your life, have F.I.R.E.

Thanks for reading! Subscribe for free to receive new posts and support my work.

Here at Dividend Collection Agency the goal is to give investors and/or readers a different perspective.

We take a simple approach to building wealth. And although investing may seem easy, people often miss opportunities by over complicating it.

But we are here to help.

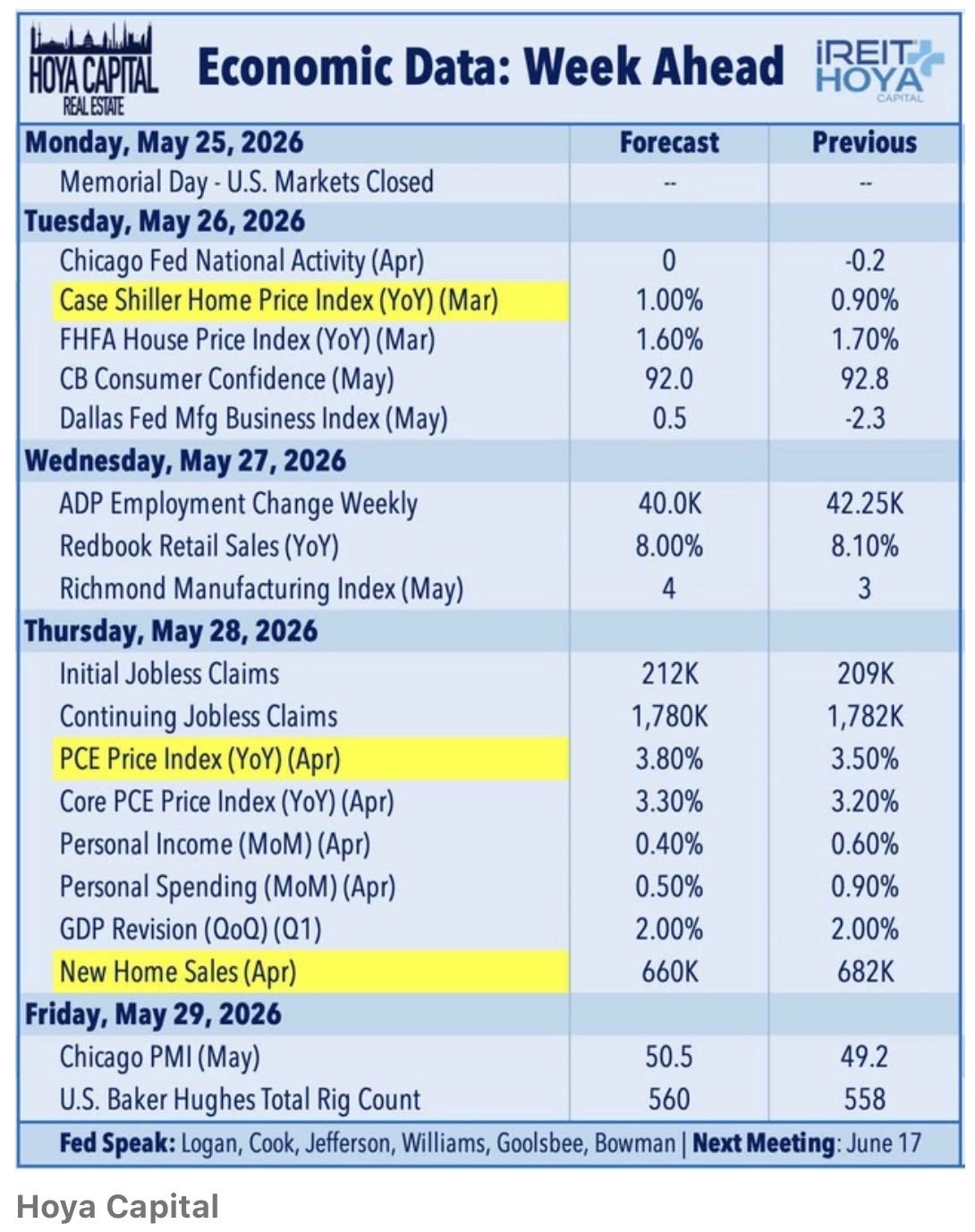

The week ahead may be shortened by the Memorial Day holiday, but investors will still face a packed slate of economic data that could shape expectations for inflation, interest rates, and the Federal Reserve’s next move.

U.S. markets will remain closed MONDAY for Memorial Day before attention quickly shifts toward a heavy lineup of housing data, inflation reports, labor market updates, GDP revisions, and regional manufacturing activity.

The biggest report of the week arrives THURSDAY with the release of the PCE Inflation report — the Federal Reserve’s preferred inflation gauge.

After recent hotter-than-expected inflation readings, markets will be closely watching to see whether price pressures continue reaccelerating heading into the summer months.

Key Economic Reports 📄

TUESDAY – Housing Data 🏡

Housing remains a major area of focus as elevated mortgage rates continue pressuring affordability and buyer demand.

Case-Shiller Home Price Index

Expected: +1.0% YoY

FHFA House Price Index

Expected: +1.6% YoY

Previous: +1.7%

While home prices remain resilient, higher financing costs continue limiting transaction activity and weighing on housing momentum.

THURSDAY – Main Event: PCE Inflation + GDP Revision 🎪

Thursday brings the most important reports of the week.

PCE Inflation Report

The Personal Consumption Expenditures (PCE) Index is expected to show inflation reaccelerating again in April.

Headline PCE

Expected: 3.8%

Previous: 3.5%

Core PCE

Expected: 3.3%

Previous: 3.2%

If inflation comes in hotter than expected once again, markets could further push out expectations for potential Fed rate cuts later this year.

Consumer Spending & Income 💵

Investors will also closely watch whether higher prices and elevated borrowing costs are beginning to pressure consumers.

Personal Income

Expected: +0.4%

Personal Spending

Expected: +0.5%

A slowdown in spending could reinforce concerns that consumers are gradually becoming more cautious amid persistent inflation and tighter financial conditions.

GDP Revision

We’ll also receive the first revision to Q1 GDP.

Q1 GDP (2nd Estimate)

Expected: 2.0%

While economic growth remains solid overall, investors continue monitoring whether higher rates are beginning to slow broader economic activity.

New Home Sales 🏷️

Housing data continues THURSDAY with New Home Sales.

New Home Sales

Expected: 660k

Previous: 682k

Mortgage rates remain one of the largest headwinds facing the housing market, particularly as affordability conditions remain historically stretched.

Labor Market Updates 📰

Labor data will remain important throughout the week.

Initial Jobless Claims

Expected: 212k

Continuing Claims

Expected: 1.78M

The labor market has remained surprisingly resilient despite elevated interest rates, though investors continue searching for signs of softening employment conditions.

FRIDAY – Manufacturing & Energy 🔌

FRIDAY closes out the week with regional manufacturing activity and energy market data.

Chicago PMI

Expected: 50.5

Previous: Below 50

A move back above 50 would signal expansionary activity and could suggest improving manufacturing conditions.

Baker Hughes Rig Count

Energy investors will also monitor the weekly rig count for additional insight into domestic energy production trends.

Fed Speakers This Week 🗣️

Several Federal Reserve officials are scheduled to speak throughout the week, including:

Logan

Cook

Jefferson

Williams

Goolsbee

Bowman

These comments could provide additional clues ahead of the Fed’s next policy meeting on June 17.

Bottom Line ✅

This may be a holiday-shortened week, but it could still carry significant implications for markets.

Inflation remains the market’s primary focus. Another hot PCE report could further pressure equities and reduce optimism surrounding near-term rate cuts.

At the same time, slowing spending, softer housing data, and rising jobless claims could reinforce concerns that elevated rates are beginning to weigh more heavily on the economy.

Markets continue balancing two competing narratives:

Sticky inflation keeping rates higher for longer

Slowing economic momentum increasing pressure for eventual policy easing

This week’s data could play a major role in determining which narrative gains momentum heading into June.

How do you think this week’s reports will affect the market? Let me know in the comments.

Just a note to let readers know I will be going paid soon. Be on the lookout for the article laying out the details. Feel free to provide any feedback!

🧐 Happy Investing!

If you’re someone who looking to start investing and need help creating passive income to achieve financial freedom, check out our investment group iREIT+HOYA Capital over on Seeking Alpha.

Here’s How: Click the Seeking Alpha link here. Click investing group, subscribe now (GET A FREE INVESTING GROUP TRIAL), or the blue hyperlink in my bio.

☎️ If you’re looking to create passive income and build your wealth from one of the top-rated analysts, book a call (Let’s Talk Investing or Detailed Portfolio Review) with me to get started.

Like & subscribe if you’re active duty, a veteran, or just love investing.