I Would Avoid This 12% Yielding BDC

"All High Yields Aren't Created Equal"

As you know by my name, I love dividends. And in addition to sharing on here, I write regularly on the investment platform- Seeking Alpha.

My goal there is to teach everyday investors about building wealth, so they won’t to need to work to traditional retirement age.

I want to help you take control of your life, have F.I.R.E.

Here at Dividend Collection Agency the goal is to give investors and/or readers a different perspective. We take a simple approach to building wealth. And although investing may seem easy, people often miss opportunities by over complicating it.

But we are here to help.

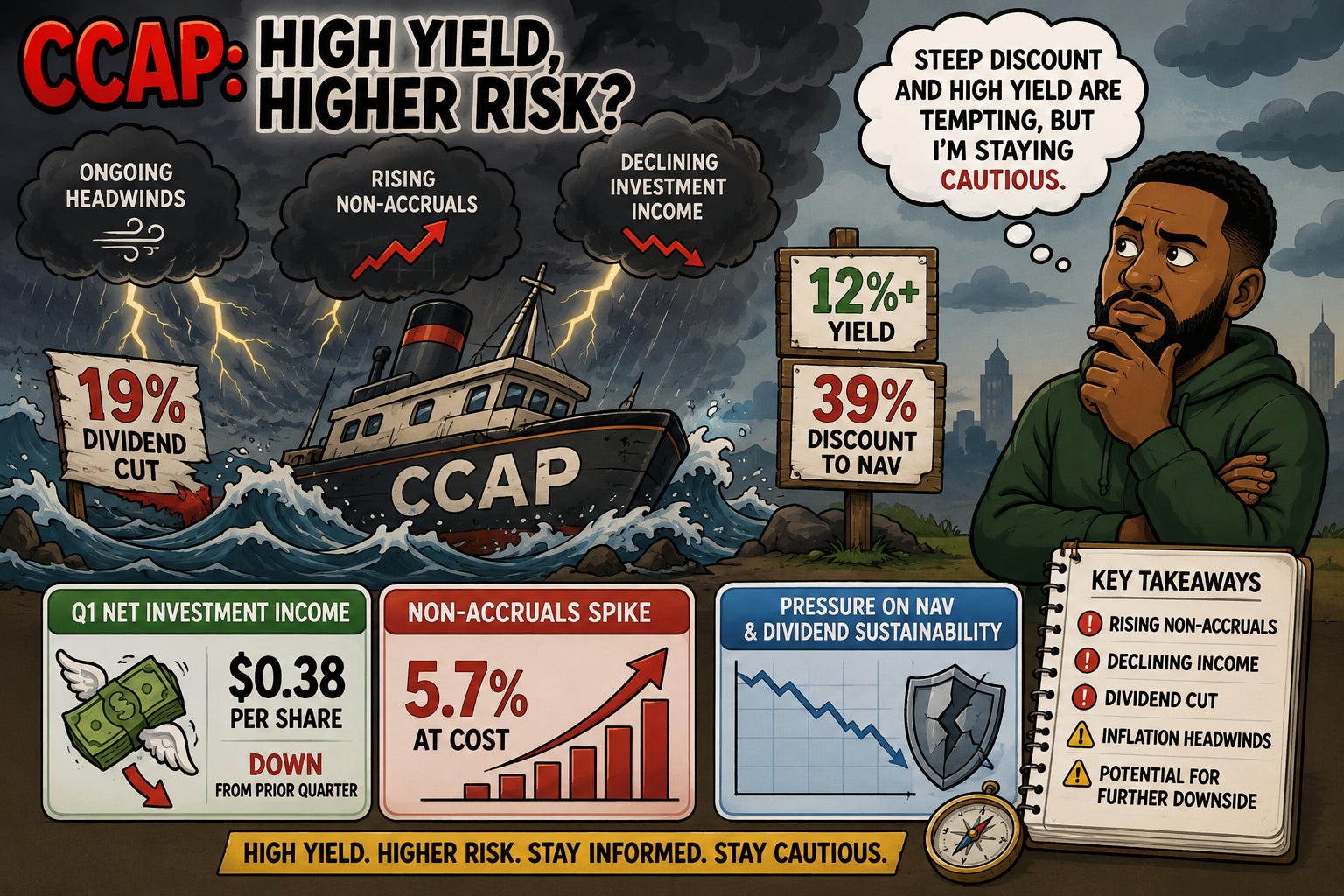

Current Price: $11.04

Dividend: $0.34

If you’ve been following my work, then you know I’ve maintained a cautious stance on the business development company (BDC) sector throughout 2025. While many investors viewed lower interest rates as a positive catalyst, I believed falling rates would pressure investment income and dividend coverage across the industry.

So far, that caution has been warranted.

The BDC sector (BIZD) has significantly underperformed the broader market, creating more attractive valuations. While I believe some high-quality BDCs now offer compelling opportunities, Crescent Capital BDC (CCAP) is not one of them.

Despite trading at an enormous 39% discount to net asset value and offering a dividend yield above 12%, I believe those metrics reflect elevated credit risk rather than a bargain.

After reviewing the company’s latest earnings, I remain concerned about deteriorating credit quality, shrinking investment income, and the possibility of additional downside over the coming quarters.

Looking Back 🔙

When I last covered CCAP in late 2025, I warned that although the nearly 30% discount to NAV and double-digit yield appeared attractive, declining interest rates and weakening dividend coverage could eventually pressure the stock.

That thesis has largely played out.

Shares have fallen more than 20% since then, while management was ultimately forced to reduce the dividend after another difficult quarter.

The recent selloff has made the valuation appear even cheaper—but cheaper doesn’t always mean better.