Income Investing Mistakes To Avoid

Making These Crucial Mistakes Can Destroy Your Wealth

As you know by my name, I love dividends. And in addition to sharing on here, I write regularly on the investment platform- Seeking Alpha.

My goal there is to teach everyday investors about building wealth, so they won’t to need to work to traditional retirement age.

I want to help you take control of your life, have F.I.R.E.

Here at Dividend Collection Agency the goal is to give investors and/or readers a different perspective. We take a simple approach to building wealth. And although investing may seem easy, people often miss opportunities by over complicating it.

But we are here to help.

As a dividend-focused investor, I’ve often wondered why more investors don’t focus on collecting income. Instead, many gravitate toward growth at all costs.

For me, income investing has always been a simple, effective strategy—one that aligns well with achieving financial independence and early retirement (F.I.R.E.). The tradeoff, of course, is that it’s usually slower.

I once heard Jeff Bezos mention that he asked Warren Buffett why more people don’t copy his investing strategy, given how straightforward it is?

Buffett’s response was telling: because it’s a get-rich-slowly strategy—and most people prefer instant gratification.

While Buffett isn’t known as a dividend investor, he collects billions in dividends every year from high-quality businesses. In fact, it’s been reported that he receives over $800 million annually from a single investment!

Income investing works—but it requires patience, discipline, and a long time horizon.

After recently publishing an article on how I’d position a portfolio if I were starting fresh in 2026, a reader suggested I write about core principles, risk controls, and return drivers. That sparked this article.

Below are some of the biggest mistakes I’ve made as an income-focused investor, and what others can learn from them.

1. Don’t Chase High Yields 🏃🏾♂️

One of the biggest mistakes I made early on was chasing high, flashy yields.

A prime example was Medical Properties Trust (MPW).

At the time, the thesis sounded great:

Hospitals are essential

Demand isn’t going away

The yield looked attractive

The stock was widely praised by income investors

Despite selling well before the stock collapsed below $4, the investment still resulted in a loss.

The lesson?

A high yield is often a warning—not an opportunity.

Most dividend blowups don’t happen overnight. The warning signs are usually visible:

Tenant concentration

Balance sheet stress

Weak cash flow coverage

Over-reliance on debt

High-yield stocks can have a place in an income portfolio—but they should be limited, especially when the goal is long-term wealth accumulation.

2. Don’t Ignore Large-Cap Growth 🚀

Another major mistake I made was neglecting growth altogether.

Early on, I focused heavily on yield. While my income stream grew nicely, my portfolio lagged in overall wealth creation.

For investors under 50, I believe growth plays a critical role in one’s portfolio.

Dividend growers like Mastercard (MA) or UnitedHealth Group (UNH) turned modest investments into substantial wealth over decades—not because of yield, but because of:

Strong cash flows

High margins

Consistent earnings growth

More recently, companies like T-Mobile US (TMUS) and Meta Platforms (META) waited until their cash flows were durable before initiating dividends. That discipline allowed them to:

Grow dividends rapidly

Reinvest in the business

Maintain balance sheet flexibility

This is very different from Verizon (V), which commits a large portion of its cash flow to dividends, limiting growth, acquisitions, and debt reduction.

3. Don’t Overlook Total Returns 👀

Yield alone does not equal performance.

T-Mobile’s yield sits below 2%, while Verizon’s exceeds 7%. Yet over the same period:

T-Mobile delivered superior price appreciation

Total returns favored growth over income

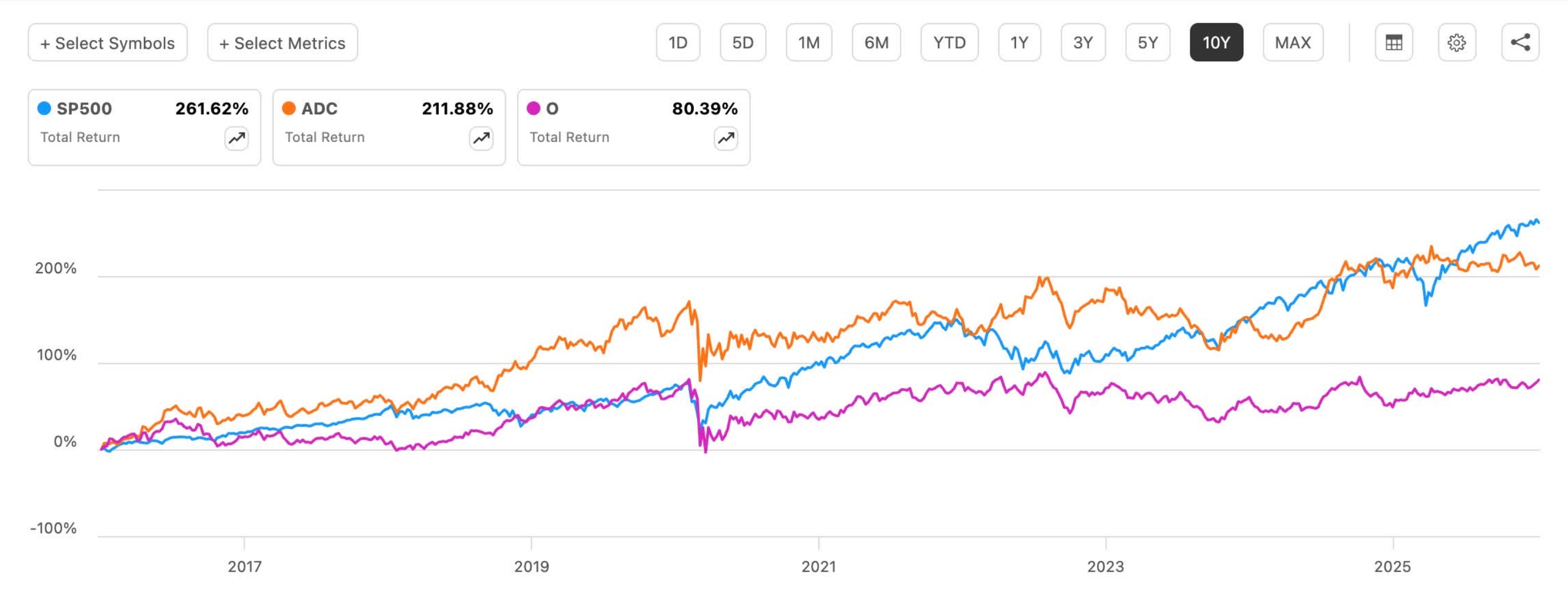

The same concept applies to REITs (XRE).

While Realty Income (O) is larger and more popular, Agree Realty (ADC) has delivered stronger long-term total returns due to:

Higher-quality tenants

Better capital discipline

Stronger balance sheet metrics

Income is important—but total return is what builds wealth.

4. Understand Taxes (This One Is Huge) 💵

Taxes are one of the most overlooked aspects of income investing.

Some investments—like REITs and BDCs (BIZD)—pay ordinary income, which can be taxed as high as 37% depending on your bracket.

Others—like dividends from companies such as Apple (AAPL) —are qualified dividends, taxed at long-term capital gains rates (0%–20%).

That difference compounds massively over time.

Certain assets are better suited for tax-advantaged accounts:

REITs

BDCs

Some covered call ETFs

Others work better in taxable accounts.

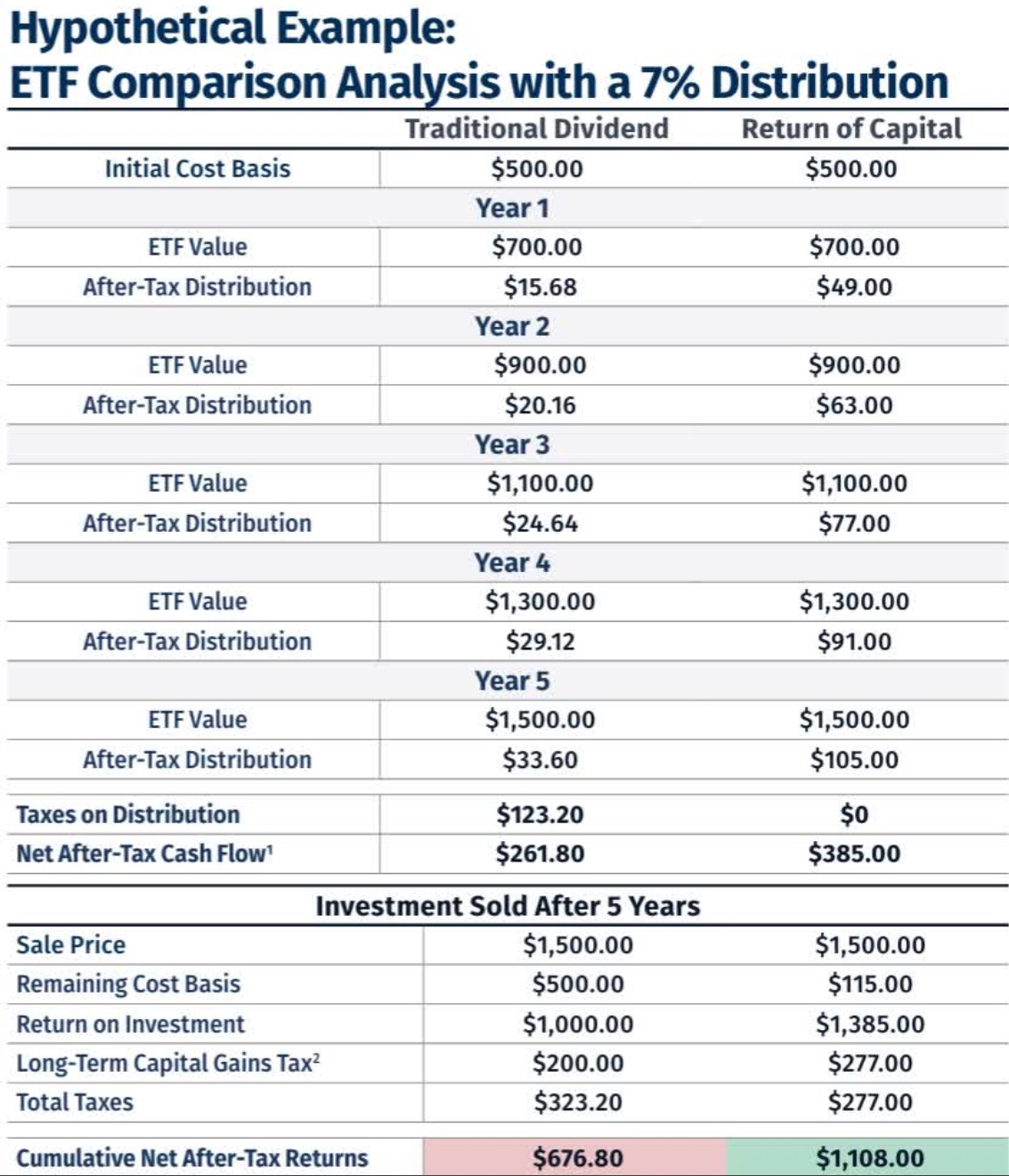

MLPs like Enterprise Products Partners (EPD) issue K-1 forms and often distribute return of capital, which can be tax-efficient—but adds complexity.

Many covered call funds, which have become extremely popular with younger investors also pay return of capital. While ROC offers tax-efficiency, it’s imperative to understand how these impact your taxes.

Return of capital defers your taxes until your cost basis reaches zero, or you decide to sell.

Below is an example:

Knowing where to hold each investment matters just as much as what you own.

5. Ignore Cash Flow at Your Own Risk ⚠️

Earnings payout ratios only tell part of the story.

Cash flow is king.

Companies like PepsiCo (PEP) and Starbucks (SBUX) have recently paid dividends that exceeded free cash flow—even when earnings appeared to cover payouts.

This creates risk.

Dividend cuts are rarely priced in fully and often lead to:

Sharp share price declines

Long recovery periods

Loss of investor trust

My personal guidelines:

FCF payout ratio under 70% for most companies

120%+ coverage for REITs and BDCs

Payout ratios below 80% for income vehicles

Portfolio Principles I Live By ⚖️

10–20 holdings is enough

Avoid ETF overlap above 30%

Balance income and growth—don’t lean too far either way

Expense ratios matter:

<0.50% for passive ETFs

<1% for active strategies

Bottom Line ✅

Too much income can stunt growth.

Too much growth can expose you to bubbles.

The key is balance, clarity of purpose, and understanding the role each investment plays in your portfolio.

Ask yourself:

Is this for income?

Growth?

Or both?

That clarity helps manage emotions during drawdowns—and keeps you invested for the long haul.

Slow. Steady. Paid.

What have you learned along your investing journey? Let me know in the comments.

Happy Investing!

☎️ If you’re looking to create passive income and build your wealth from one of the top-rated analysts, book a call (Let’s Talk Investing or Detailed Portfolio Review) with me to get started.

If you’re looking to start investing check out our investment group over on Seeking Alpha.

Here’s How: Click the Seeking Alpha link here. Click investing group, subscribe now, or the blue hyperlink in my bio.

Not financial advice. For educational purposes only. I am not a licensed professional. Do your own due diligence.

Like & subscribe if you’re active duty, a veteran, or just love investing.