Kenvue's Acquiring By Kimberly-Clark Is A Win-Win For Shareholders

"A Solid Dividend Play Should The KMB Acquisition Fall Through"

As you know by my name, I love dividends. And in addition to sharing on here, I write regularly on the investment platform- Seeking Alpha.

My goal there is to teach everyday investors about building wealth, so they won’t to need to work to traditional retirement age.

I want to help you take control of your life, have F.I.R.E.

Here at Dividend Collection Agency the goal is to give investors and/or readers a different perspective. We take a simple approach to building wealth. And although investing may seem easy, people often miss opportunities by over complicating it.

But we are here to help.

Current Price: $18.07

Dividend/Yield: $0.21/4.735

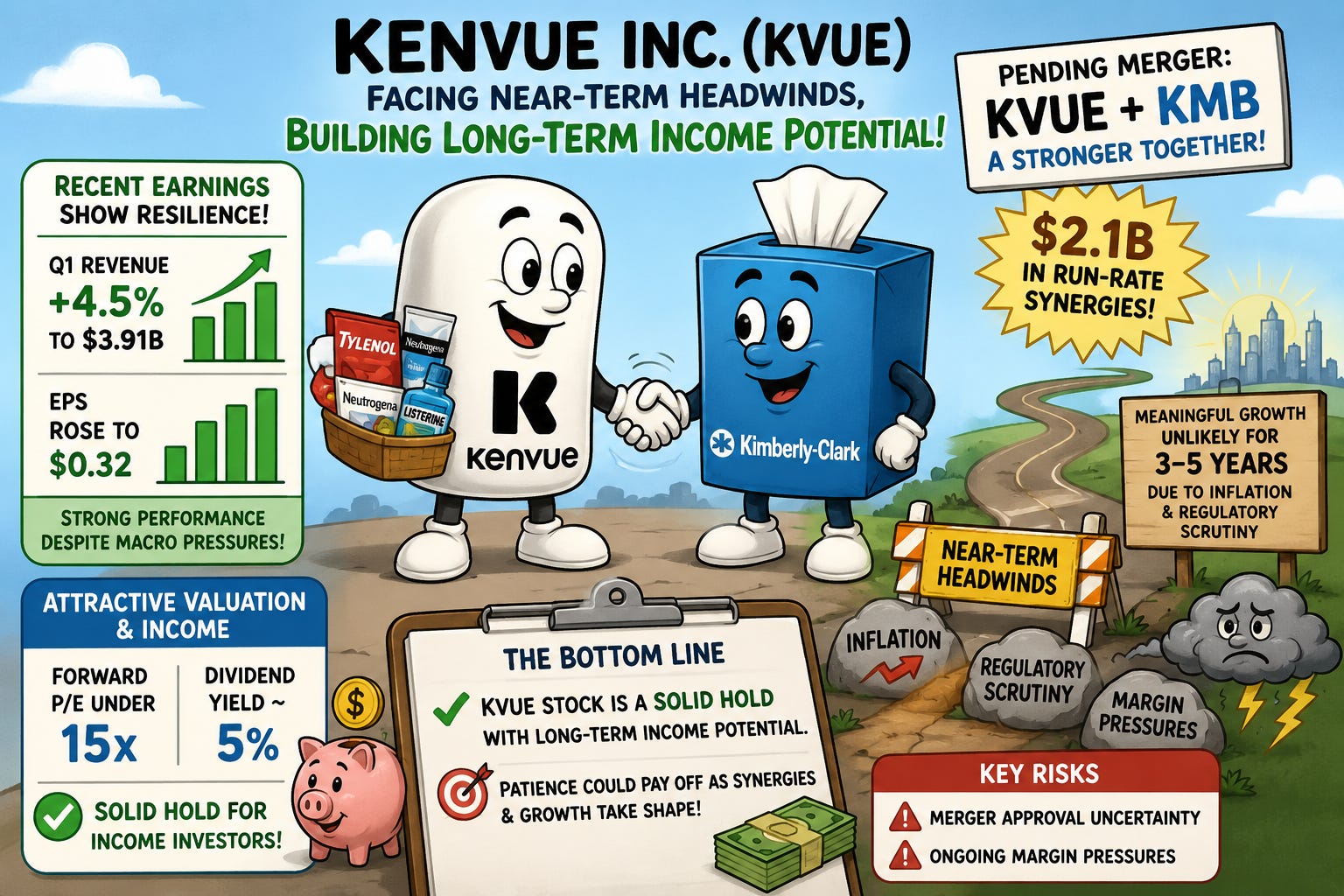

Although Kenvue’s (KVUE) spinoff from Johnson & Johnson (JNJ) is approaching its three-year anniversary, the stock’s performance has been underwhelming, marked by volatility and limited shareholder returns.

I initially purchased shares shortly after the spinoff and exited with a modest profit well before the company’s announced merger with Kimberly-Clark (KMB) in late 2025.

My first reaction to the deal was positive.

Combining two consumer staples giants with iconic brands seemed like a logical move that could unlock value through scale, cost synergies, and stronger global distribution. Shareholders overwhelmingly approved the transaction, but the real question remains:

Can This Merger Actually Reignite Growth? 📉

I believe it can.

The challenge is that investors may need to wait several years before seeing the full benefits materialize.

Kenvue Shows Signs Of Stability 🧱

Since separating from Johnson & Johnson, Kenvue has faced a difficult operating environment. Persistent inflation, higher interest rates, tariffs, and pressured consumer spending have all weighed on results.

Despite those headwinds, Kenvue delivered a solid first quarter.

Q1 Highlights 📋

Revenue increased 4.5% year-over-year to $3.91 billion

EPS rose to $0.32 from $0.24

Revenue exceeded estimates by $60 million

EPS beat expectations by $0.06

Growth was broad-based across all three business segments.

Skin Health & Beauty led the way with sales growth of 8.4%, supported by strong volume gains.

Essential Health delivered 4.9% sales growth and modest organic growth.

Self-Care remained challenged as a weaker cold and flu season resulted in lower volumes, though sales still increased 1.9%.

Considering the difficult macro backdrop, the quarter demonstrated that Kenvue’s portfolio of consumer brands remains resilient.

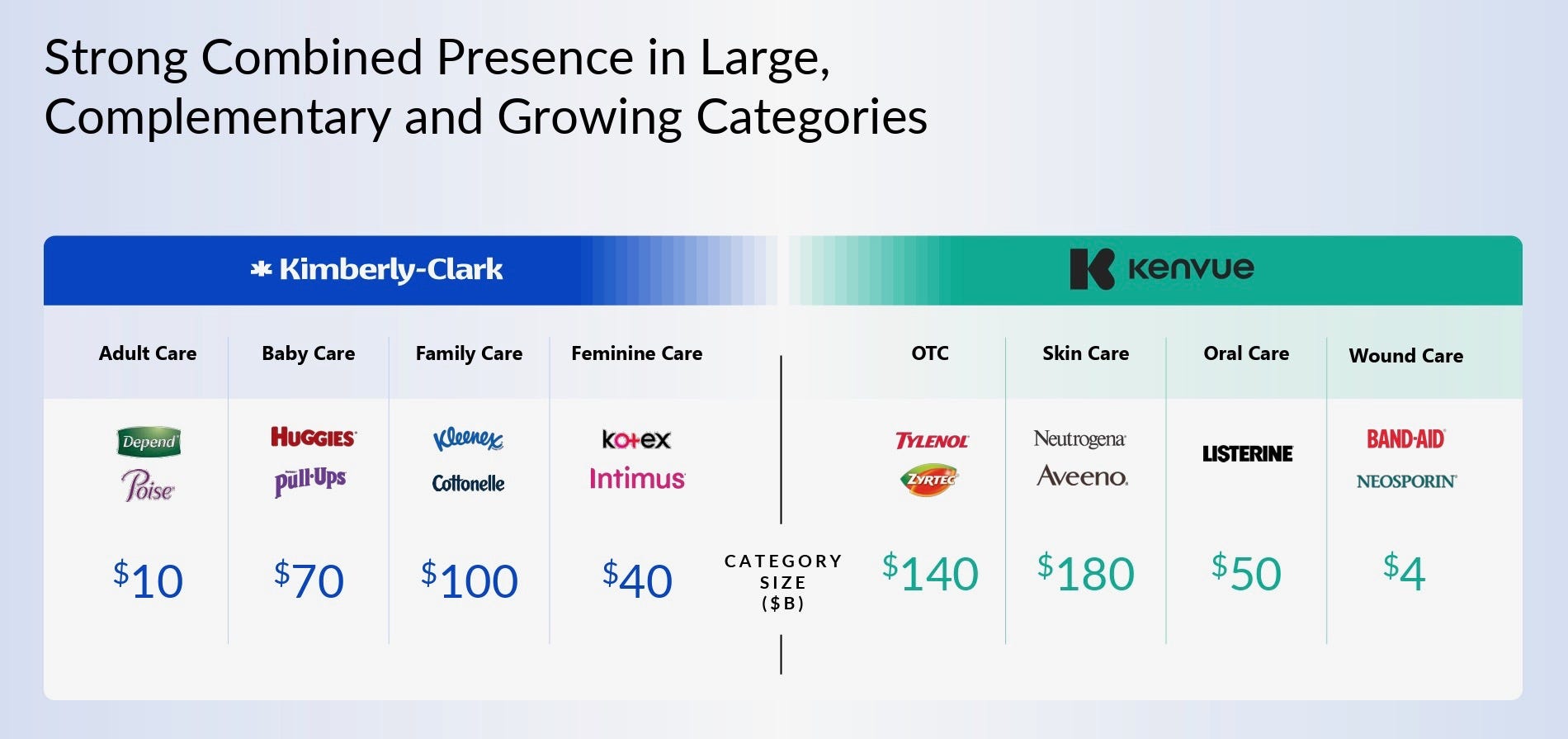

Why The Kimberly-Clark Merger Matters 🧻

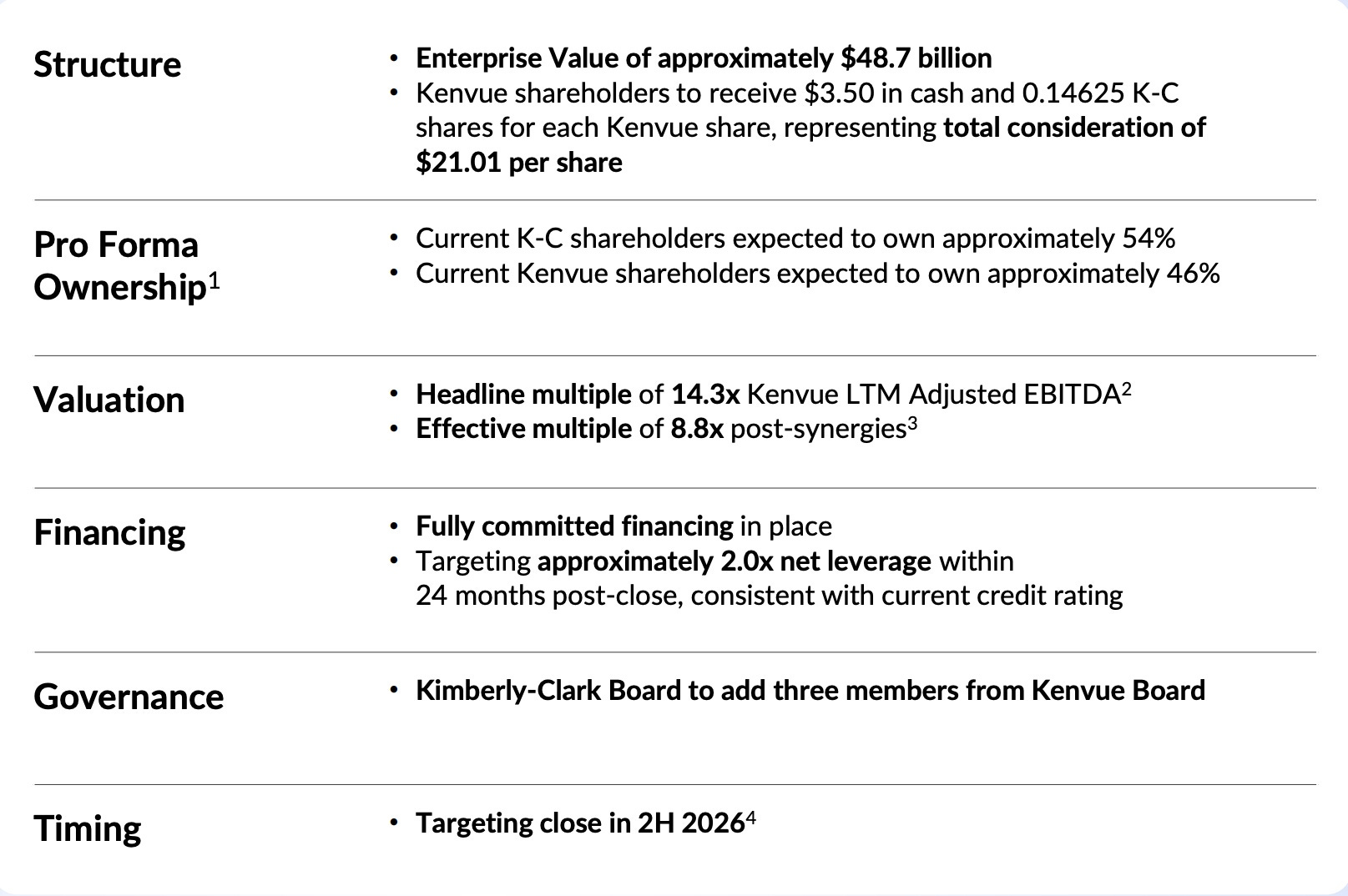

The proposed Kimberly-Clark merger is expected to close later this year, pending regulatory approval.

Management projects approximately $2.1 billion in annual run-rate synergies, making the deal one of the largest consumer staples combinations in recent years.

However, investors should temper expectations.

Even if approved, I don’t expect meaningful growth to emerge for at least three to five years.

Inflation remains elevated, consumers continue to face affordability pressures, and both companies are dealing with margin challenges.

Recent requests from Chinese regulators for additional information highlight that approval risk still exists.

That said, the long-term opportunity is compelling.

The combined company would own an impressive collection of household brands while expanding its global reach and supply-chain efficiency.

If management successfully integrates operations, optimizes manufacturing, and leverages international distribution networks, earnings growth could accelerate meaningfully over time.

International Growth: A Major Opportunity 🌎

One of the most attractive aspects of the merger is international expansion.

Approximately half of Kenvue’s revenue already comes from outside the United States, while Kimberly-Clark has established positions across several high-growth international markets.

Recent strength in countries such as Brazil, China, Indonesia, and Australia demonstrates that international demand remains healthy despite broader economic uncertainty.

Over time, I expect management to prioritize these markets as a key growth driver.

Cash Flow Supports The Dividend 💰

Kenvue’s balance sheet remains healthy.

During the first quarter:

Operating cash flow increased to $500 million

Free cash flow doubled year-over-year to approximately $400 million

Long-term debt totaled $8.7 billion

Cash and equivalents stood at $1.1 billion

These figures support the company’s dividend and provide flexibility as management prepares for integration efforts.

Valuation Remains Attractive 👏🏾

At less than 15x forward earnings and a dividend yield near 5%, Kenvue continues to offer an appealing risk-reward profile for income-focused investors.

Under the merger terms, Kenvue shareholders are expected to receive:

$3.50 per share in cash

0.14625 shares of Kimberly-Clark stock for each Kenvue share owned

Based on current prices, the implied value remains above where KVUE currently trades, suggesting investors are still assigning some probability that the deal faces regulatory hurdles.

Even if the merger ultimately fails, I believe Kenvue remains a solid income investment due to its strong brands, stable cash flows, and attractive dividend yield.

Final Thoughts ✅

For now, Kenvue remains more of an income story than a growth story.

Near-term uncertainty surrounding merger approval, inflation, and margin pressure could keep shares rangebound. However, I believe patient investors may eventually benefit if management successfully executes the Kimberly-Clark integration and captures the projected synergies.

The biggest risk remains regulatory approval. Should the deal fail, shares would likely face short-term downside.

Still, Kenvue’s fundamentals remain solid, and its nearly 5% dividend yield provides investors with a meaningful income stream while waiting for growth to emerge.

For existing shareholders, I continue to view KVUE as a Hold. Whether the merger succeeds or not, the company’s defensive business model, strong brands, and income potential make it worth keeping in a diversified portfolio.

RATING: HOLD

Do you think Kenvue will help Kimberly-Clark achieve the growth it’s looking for? Let me know in the comments.

Just a note to let readers know I will be going paid soon. Be on the lookout for the article laying out the details. Feel free to provide any feedback!

Happy Investing!

☎️ If you’re looking to create passive income and build your wealth from one of the top-rated analysts, book a call (Let’s Talk Investing or Detailed Portfolio Review) with me to get started.

If you’re looking to start investing check out our investment group over on Seeking Alpha.

Here’s How: Click the Seeking Alpha link here. Click investing group, subscribe now (GET AN INVESTING GROUP FREE TRIAL), or the blue hyperlink in my bio.

Not financial advice. For educational purposes only. I am not a licensed professional. Do your own due diligence.

Like & subscribe if you’re active duty, a veteran, or just love investing.