Kohl's: Collect A 3% Yield From An Improving Business, But Be Careful Of A Potential Value Trap

"Low P/E But Cheap For A Reason"

As you know by my name, I love dividends. And in addition to sharing on here, I write regularly on the investment platform- Seeking Alpha.

My goal there is to teach everyday investors about building wealth, so they won’t to need to work to traditional retirement age.

I want to help you take control of your life, have F.I.R.E.

Here at Dividend Collection Agency the goal is to give investors and/or readers a different perspective. We take a simple approach to building wealth. And although investing may seem easy, people often miss opportunities by over complicating it.

But we are here to help.

Current Price: $14.34

Dividend / Yield: $.050 / 3.31%

Portfolio Purpose: Growth 📉

Over the past year, Kohl’s Corporation (KSS) has faced significant pressure from economic uncertainty. During this period, the company was forced to cut its dividend by 75%, highlighting how “higher-for-longer” interest rates had placed substantial pressure on both the retailer and its consumer base.

Since then, the department store operator has begun showing incremental improvements. While this progress has helped push the stock up more than 30%, investors should still remain cautious. Despite a dividend yield above 3% and a seemingly attractive valuation, several macro and operational risks remain.

In this note, I’ll review Kohl’s recent performance, its outlook, and why patience may still be the best approach for investors.

Previous Thesis 📖

I last covered Kohl’s about six months ago.

At the time, the company had beaten both top- and bottom-line estimates, but revenue still declined 6.5% year-over-year. Shares rallied primarily because management raised full-year guidance.

Several developments offered reasons for cautious optimism:

The Sephora partnership driving store traffic

Stronger performance from proprietary brands

The dividend cut, which improved financial flexibility

Still, I suggested investors wait to see if those improvements would fully materialize amid continued economic uncertainty.

Since then, KSS shares are down roughly 9%, compared with the S&P 500 Index (SP 500), which is up roughly 5% over the same period.

Slight Improvements Beneath The Surface 👍🏾

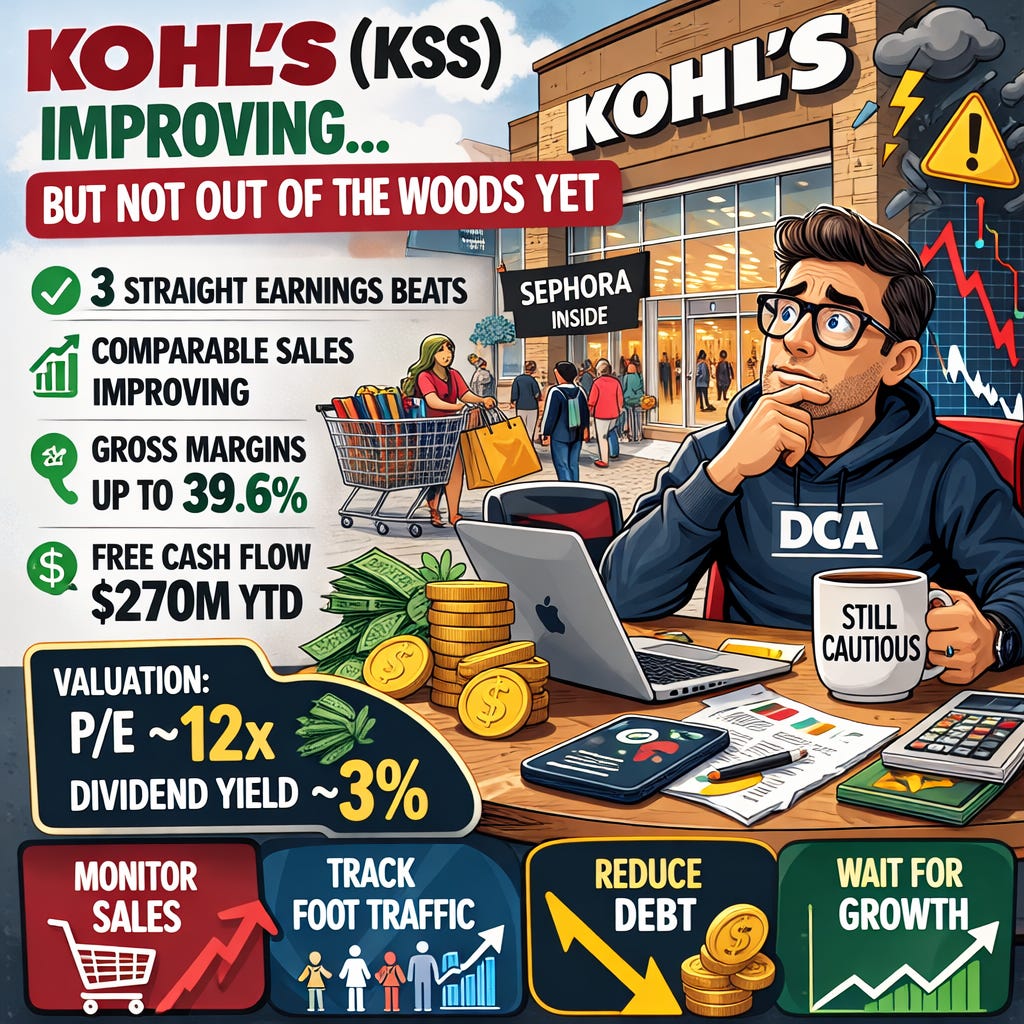

Kohl’s reported Q3 earnings in November, posting another double beat.

Key results included:

EPS: $0.10 (beat estimates by $0.27)

Revenue: $3.41B (beat estimates by $40M)

However, revenue was still down roughly 3% year-over-year, while net income fell 50%, declining from $22 million to $11 million.

Through the first three quarters:

Net income: $61M (flat YoY)

EPS: $0.54 (down slightly year-over-year)

At first glance, those numbers appear disappointing. But digging deeper reveals meaningful operational progress.

Sales Trends Improving ↗️

Net sales declined 2.8%, but that represents a significant improvement from the 8.8% decline in the prior year’s quarter.

For the first nine months:

Net sales declined 4%, improving from -6.1% previously.

Comparable Sales Showing Progress 💵

Comparable sales fell 1.7% in Q3, a major improvement from -9.3% the year before.

Year-to-date comparable sales are down 3.2%, a 320 basis-point improvement.

This progress was largely driven by higher transaction volumes, though average transaction size declined 3% during the quarter.

Digital and Margin Improvements 💻

Digital sales increased 2.4%, supported by higher traffic and improvements tied to the Kohl’s customer card.

Gross margins also expanded 51 basis points to 39.6%, helped by:

Stronger inventory management

Growth in proprietary brand sales

For comparison, Macy’s (M) reported slightly lower margins year-over-year, declining from 39.6% to 39.4%.

Additional growth drivers included:

New brand launches

Jewelry sales increasing 10%

Impulse purchases rising 4%

Overall, the data suggests Kohl’s is moving in the right direction, though more progress is still required.

Raised Guidance 💸

Kohl’s Q3 earnings beat marked their third consecutive earnings beat, allowing management to raise full-year guidance again.

Updated expectations include:

Net sales decline: improved from -6% to -5% range

Comparable sales: improved from -5% to -4% range

Operating margins: raised to 2.5%–2.7%

EPS guidance also improved from the prior range of $0.50–$0.80, signaling stronger profitability expectations.

Strong Free Cash Flow 💰

Another positive development is Kohl’s improving cash generation.

Through three quarters:

Cash from operations: $630M (vs. $52M last year)

Adjusted free cash flow: $270M

Shareholder returns: $42M

This leaves the company with ample retained cash flow, potentially allowing for share repurchases in the future.

For now, however, management appears focused on deleveraging, which I believe is the correct priority.

Management expects for 2025:

Cash from operations: $1.3B

Free cash flow: $900M

Balance Sheet ⚖️

At the end of the quarter:

Cash & equivalents: $144M

Long-term debt: $1.52B

Net debt: $1.42B

Leverage currently sits around 4.5x, or 2.6x when adjusted for leases.

Given the company’s improving free cash flow, I would like to see leverage reduced toward 2.0x by 2026.

What I Expect For Q4 🧐

Analysts expect meaningful improvements in Q4, driven largely by holiday sales.

Consensus estimates suggest stronger results than Q3:

Revenue above $3.41B

EPS above $0.10

My expectations:

EPS: $0.80 – $0.85

Improved top-line performance from holiday demand

Investors should pay particular attention to:

Comparable store sales

Transaction growth

Foot traffic trends

Valuation and Dividend Yield 💲

From a valuation standpoint, Kohl’s appears relatively attractive.

At the midpoint of guidance:

Forward P/E: 12.29x

Dividend yield: ~3%

Both metrics sit below the company’s five-year average and the broader sector.

While this could support a short-term rally—especially if earnings beat expectations—I believe near-term upside may remain limited.

Long-Term Growth Outlook 👀

Another reason for caution is the company’s expected near-term earnings headwinds.

However, analysts anticipate a turnaround later in the decade.

Consensus forecasts suggest:

Earnings growth could resume around 2027

Double-digit growth through 2031

If the economy avoids recession and interest rates decline, Kohl’s could return to sustainable growth sooner than expected.

Risks ⚠️

Recent geopolitical tensions—including attacks involving Iran—have added another layer of economic uncertainty.

Rising oil and gas prices could push inflation higher, potentially impacting consumer spending.

If inflation were to reaccelerate, the Federal Reserve could be forced to keep rates elevated longer, further pressuring retailers like Kohl’s.

While I still expect the Fed to hold rates steady rather than raise them, macro uncertainty remains elevated.

Bottom Line ✅

Kohl’s has made meaningful operational progress, and management appears to be moving the company in the right direction.

Positive developments include:

Improving sales trends

Expanding margins

Rising free cash flow

Attractive valuation metrics

The 3% dividend yield, now better supported by cash flows, also provides some incentive for shareholders to remain patient.

That said, investors should closely monitor:

Sales growth

Foot traffic trends

Deleveraging progress

If management can reduce leverage while returning to positive revenue and earnings growth, I would consider upgrading the stock to a Buy.

For now, however, elevated macro uncertainty and the risk of inflation reaccelerating lead me to maintain a cautious stance.

Do you think Kohl’s’ earnings growth will turn positive in the near term? Let me know in the comments.

Happy Investing!

☎️ If you’re looking to create passive income and build your wealth from one of the top-rated analysts, book a call (Let’s Talk Investing or Detailed Portfolio Review) with me to get started.

If you’re looking to start investing check out our investment group over on Seeking Alpha.

Here’s How: Click the Seeking Alpha link here. Click investing group, subscribe now, or the blue hyperlink in my bio.

Not financial advice. For educational purposes only. I am not a licensed professional. Do your own due diligence.

Like & subscribe if you’re active duty, a veteran, or just love investing.