McDonald's Shares Aren't A Value Meal Deal Here, But Recent Pullback Improves Long-Term Setup

"MCD's 2.57% Yield Attractive For Long-Term Income/Growth Investors"

As you know by my name, I love dividends. And in addition to sharing on here, I write regularly on the investment platform- Seeking Alpha.

My goal there is to teach everyday investors about building wealth, so they won’t to need to work to traditional retirement age.

Thanks for reading! Subscribe for free to receive new posts and support my work.

I want to help you take control of your life, have F.I.R.E.

Here at Dividend Collection Agency the goal is to give investors and/or readers a different perspective. We take a simple approach to building wealth. And although investing may seem easy, people often miss opportunities by over complicating it.

But we are here to help.

Current Price: $280.80

Dividend/Yield: $1.86/2.57%

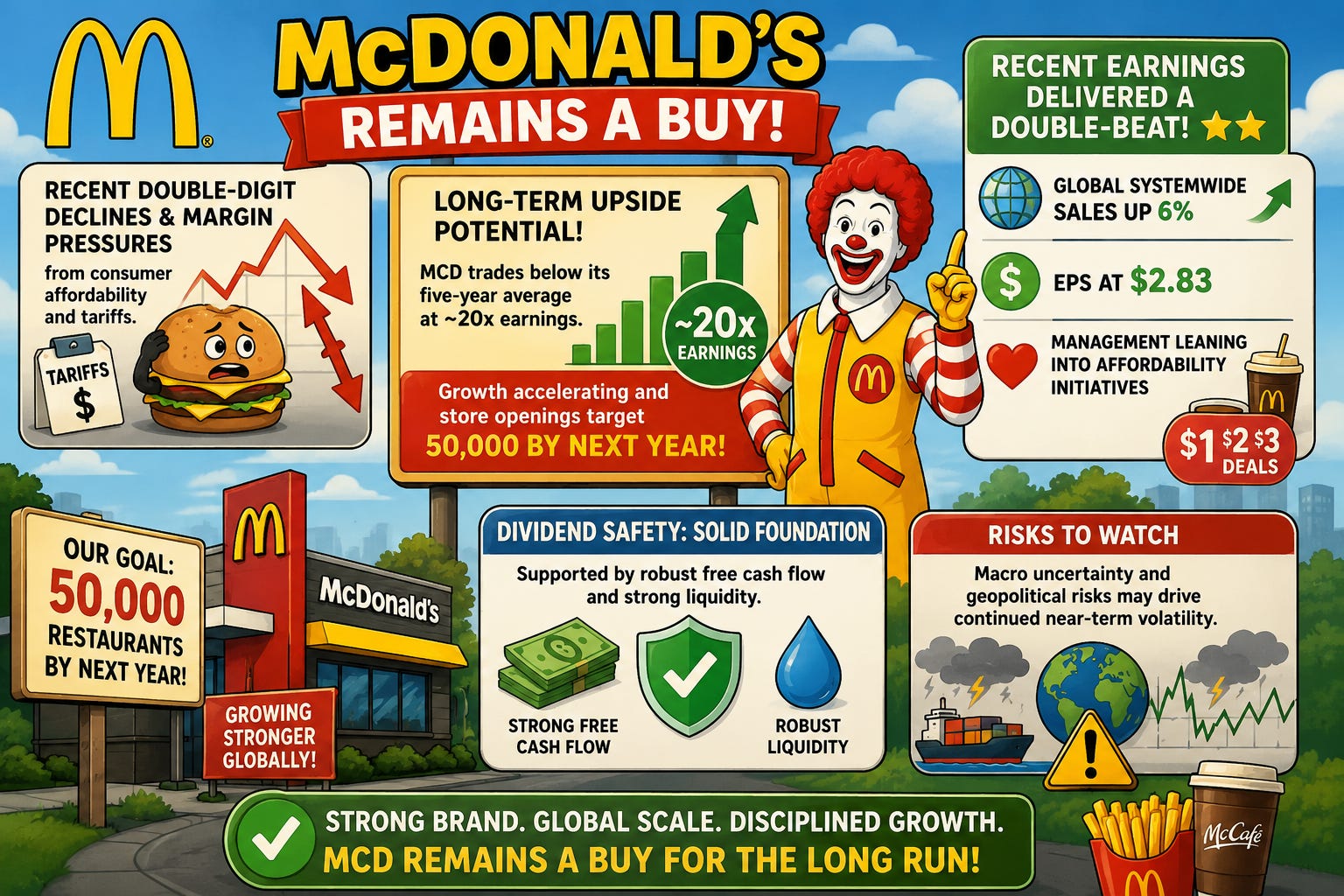

McDonald’s (MCD) has struggled in recent months, with shares down roughly 11% over the past year as affordability pressures, tariffs, and slower consumer spending weighed on sentiment.

Despite the near-term volatility, I believe the long-term investment thesis remains attractive.

The future Dividend King continues to generate resilient cash flow, maintain strong global brand dominance, and aggressively expand its footprint.

While growth has slowed from the double-digit pace seen in prior years, the recent pullback has improved valuation and created what I believe is a compelling long-term entry point for dividend growth investors.

Trading around 20x earnings — below its five-year average — MCD now offers a more attractive risk/reward profile with potential for shares to trend toward $400 over the next 12 to 24 months if macro conditions improve.

Slowing Growth Has Weighed On Shares 🏋🏾

McDonald’s saw growth decelerate notably in 2025 compared to the strong post-pandemic recovery years.

While results remained solid overall, the business experienced:

Margin pressures from rising beef costs

Tariff-related headwinds

Softer discretionary consumer spending

Slower restaurant traffic globally

The Middle East conflict and rising oil prices also pressured sentiment throughout 2026, creating additional uncertainty for global consumer businesses.

Still, McDonald’s delivered respectable full-year results:

Global comparable sales rose 3.8%

U.S. comparable sales increased 3.9%

International markets also grew 3.9%

Systemwide sales rose 6% to $139.4 billion

Operating margins expanded to 46.1%

That performance was a meaningful improvement from the prior year, when several international markets experienced declining sales growth.

The reality is simple: higher inflation has pressured lower-income consumers, particularly in quick-service restaurants. But management appears focused on adapting quickly.

Affordability Initiatives And Growth Expansion ↗️

McDonald’s is aggressively leaning into affordability initiatives while simultaneously accelerating long-term growth investments.

The company launched its revamped McValue platform to drive traffic and improve value perception among consumers facing tighter budgets.

Early results appear encouraging.

During the latest quarter:

Revenue beat expectations at $6.52 billion

EPS came in at $2.83

Net income rose 6%

Global systemwide sales increased 6%

The quarter represented a notable rebound after the previous year’s softer performance.

Management also continues to invest heavily in expansion:

2,275 new stores opened in 2025

2,600 openings projected for 2026

Long-term target of 50,000 stores globally by next year

Capex is projected to rise toward $3.9 billion as the company accelerates development initiatives.

I believe this is one of the most important parts of the investment thesis.

McDonald’s remains one of the few restaurant companies with the scale, brand power, and balance sheet to continue expanding aggressively despite macro uncertainty.

The company also recently launched new refreshers and beverage initiatives designed to compete more directly with Starbucks and attract younger consumers.

Dividend Safety Remains Strong 💵

McDonald’s is on the verge of becoming a Dividend King, with 49 consecutive years of dividend increases.

While dividend growth has slowed from roughly 10% annually to closer to 5%, the payout still appears extremely safe.

Key dividend metrics remain solid:

Free cash flow payout ratio around 71%

2025 free cash flow totaled $7.2 billion

Shareholder returns reached $7.1 billion

Quarterly free cash flow covered dividends comfortably

The balance sheet remains manageable as well:

Long-term debt sits near $40 billion

Liquidity remains strong at roughly $1.2 billion

Debt has risen in recent years, but relative to McDonald’s scale and cash generation, I don’t view the current leverage as alarming.

Management also continues to buy back shares aggressively, repurchasing roughly $2 billion worth in 2025 alone.

Valuation And Long-Term Upside 📉

At roughly 20x earnings, McDonald’s now trades below its historical valuation average despite maintaining:

Strong profitability

Global scale

Reliable cash flow

Dividend growth

Expansion opportunities

Compared to peers like Domino’s Pizza (DPZ) and Chipotle Mexican Grill (CMG), the valuation appears increasingly attractive for conservative dividend growth investors.

I do not expect explosive market-beating returns from McDonald’s given the maturity of the business.

If you’re looking for a stock analyzer tool that gives you future price targets based on historical data, use my code to get 25% off of FAST Graphs, my go-to the stock analyzer tool for research.

However, I believe the current pullback creates a compelling setup for:

Steady long-term appreciation

Reliable dividend growth

Potential multiple expansion

Improved investor sentiment if inflation moderates

Should consumer spending stabilize and geopolitical tensions ease, shares could reasonably re-rate higher over the next one to two years.

Risks To Watch ⚠️

Near-term risks remain elevated.

The biggest concerns include:

Continued inflationary pressure

Higher beef costs

Tariff uncertainty

Weak consumer sentiment

Ongoing geopolitical tensions

If margins continue compressing, shares could potentially retest lows near the $260 range before stabilizing.

That said, further downside would likely improve the long-term investment opportunity for patient investors focused on dividend growth and income compounding.

Bottom Line ✅

McDonald’s remains one of the highest-quality restaurant businesses in the world.

While growth has slowed and macro pressures continue weighing on performance, the company’s:

Global scale

Franchise model

Dividend safety

Strong cash generation

Aggressive store expansion

…all support the long-term investment thesis.

I still rate shares a buy for long-term dividend growth investors, although I believe some near-term volatility is likely to persist until consumer conditions improve further.

Do you think McDonald’s aggressive store openings will accelerate growth? Let me know in the comments.

Just a note to let readers know I will be going paid soon. Be on the lookout for the article laying out the details. Feel free to provide any feedback!

Happy Investing!

☎️ If you’re looking to create passive income and build your wealth from one of the top-rated analysts, book a call (Let’s Talk Investing or Detailed Portfolio Review) with me to get started.

If you’re looking to start investing check out our investment group over on Seeking Alpha.

Here’s How: Click the Seeking Alpha link here. Click investing group, subscribe now (GET AN INVESTING GROUP FREE TRIAL), or the blue hyperlink in my bio.

Not financial advice. For educational purposes only. I am not a licensed professional. Do your own due diligence.

Like & subscribe if you’re active duty, a veteran, or just love investing.