One Of The Best Dividend Growth Stocks Ever, But Not At Nearly 50x Earnings

"Quality Comes At A Price, But Nearly 50x Earnings Is Too Expensive"

As you know by my name, I love dividends. And in addition to sharing on here, I write regularly on the investment platform- Seeking Alpha.

My goal there is to teach everyday investors about building wealth, so they won’t to need to work to traditional retirement age.

I want to help you take control of your life, have F.I.R.E.

Here at Dividend Collection Agency the goal is to give investors and/or readers a different perspective. We take a simple approach to building wealth. And although investing may seem easy, people often miss opportunities by over complicating it.

But we are here to help.

Current Price: $974.00

Dividend/Yield: $1.47/0.61%

Costco Wholesale (COST) remains one of my favorite dividend growth stocks of all time.

In fact, despite the company’s modest regular dividend yield, its combination of annual dividend increases and occasional special dividends is one of the main reasons I’ve always admired the business.

I’m also a Costco member myself and shop there almost weekly. I often joke with my girlfriend that one day you’ll probably be able to order a baby from Costco because the company seems to sell virtually everything else.

That customer loyalty is exactly why Costco commands such a premium valuation.

The company has built one of the strongest retail ecosystems in the world, supported by a fortress balance sheet, industry-leading membership retention, and a business model that continues to generate consistent growth regardless of economic conditions.

The problem isn’t the business.

The problem is the price investors are currently being asked to pay for it.

Even after the recent pullback, Costco still trades at more than 45x forward earnings. While I have no concerns about the long-term future of the company, I continue to believe that valuation alone could keep shares under pressure relative to the broader market.

As a result, I’m maintaining my Hold rating.

Costco Continues To Execute 📊

The latest quarter was another reminder of why Costco has earned its reputation as one of the highest-quality businesses in America.

Revenue came in at $70.5 billion, exceeding expectations by nearly $900 million, while earnings per share reached $4.93. Both revenue and earnings increased by double digits year-over-year, driven by healthy membership growth, strong traffic, and resilient consumer demand.

Membership income continued growing at an impressive pace, while executive memberships increased approximately 10% from the prior year.

Those are elite numbers for a retailer already operating at Costco’s scale.

However, beneath the headline results, there were a few signs that growth is beginning to normalize.

Comparable sales excluding fuel increased 6.6%, slightly below the prior quarter’s 6.7% growth and well below the 8% growth rate achieved a year ago.

While these figures remain strong, the trend suggests consumers may be becoming increasingly price-sensitive as inflationary pressures persist.

For a company that relies heavily on high-volume sales growth, slowing comparable sales growth is something investors should continue monitoring closely.

Higher Fuel Prices Are Helping Costco ⛽️

One interesting aspect of Costco’s quarter is that rising fuel prices actually provided a tailwind.

While higher energy costs have negatively impacted many businesses, Costco’s fuel operations benefit from offering members some of the lowest gasoline prices available.

Anyone who regularly visits a Costco gas station has likely witnessed the long lines firsthand.

As fuel prices rise, Costco’s value proposition becomes even more compelling, potentially driving additional membership growth.

Comparable sales including fuel rose 9.8%, highlighting just how significant the gasoline business has become.

Should energy prices remain elevated throughout the year, Costco may continue benefiting from increased traffic and membership additions.

However, there is also a downside.

Higher fuel costs contribute to inflationary pressures that ultimately reduce consumer purchasing power, which can weigh on spending across other merchandise categories.

Margin Pressure Remains A Watch Item 👀

Another area worth monitoring is profitability.

Gross margins declined to 11.04% compared to 11.25% in the prior year.

Management cited lower pricing on key staples such as eggs and beef, along with fuel-related impacts, as primary reasons for the decline.

This shouldn’t be viewed as a major concern today.

Costco has historically accepted lower margins in exchange for maintaining its value leadership and strengthening member loyalty.

Still, if inflation remains elevated for an extended period, margin pressure could become more persistent and place additional pressure on earnings growth.

The Growth Runway Remains Long ↗️

One reason investors continue paying premium multiples for Costco is because growth opportunities remain substantial.

Management continues targeting more than 30 net new warehouse openings annually and plans to open 26 warehouses this fiscal year alone.

During the most recent quarter, Costco added four new warehouses, bringing the global total to 928 locations.

The company also continues investing heavily in digital capabilities, fulfillment improvements, and customer experience enhancements designed to support future membership growth.

While many mature retailers struggle to find growth opportunities, Costco still has a significant runway both domestically and internationally.

That combination of scale and growth is rare.

Dividend Growth And Financial Strength 💰

Despite increased investment spending, Costco’s dividend remains exceptionally safe.

The company finished the fiscal year with a free cash flow payout ratio of just 28%, providing significant flexibility for future dividend increases and share repurchases.

Earlier this year, management increased the quarterly dividend by 13.1%, continuing a long history of double-digit dividend growth.

The balance sheet remains equally impressive.

Costco currently holds approximately $19 billion in cash and cash equivalents versus just $5.7 billion in long-term debt.

Very few companies possess this level of financial flexibility.

This balance sheet strength provides Costco with the ability to continue investing aggressively in growth while simultaneously rewarding shareholders through dividend increases, buybacks, and potentially future special dividends.

Valuation Remains Biggest Risk ⚠️

Operationally, Costco remains one of the strongest businesses in the market.

The issue is that investors already know that.

At roughly 45.6x forward earnings, Costco continues trading at a substantial premium not only to the broader market but also to many of its retail peers.

Even high-quality retailers such as Walmart (WMT) and Casey’s General Stores (CASY) trade at slightly lower valuations despite also carrying historically elevated multiples.

Meanwhile, BJ’s Wholesale Club (BJ) trades at less than half Costco’s valuation.

I understand why investors are willing to pay a premium.

In an environment filled with economic uncertainty, Costco has increasingly become viewed as a safe-haven stock.

The company offers predictable growth, recurring membership revenue, elite execution, and one of the strongest brands in retail.

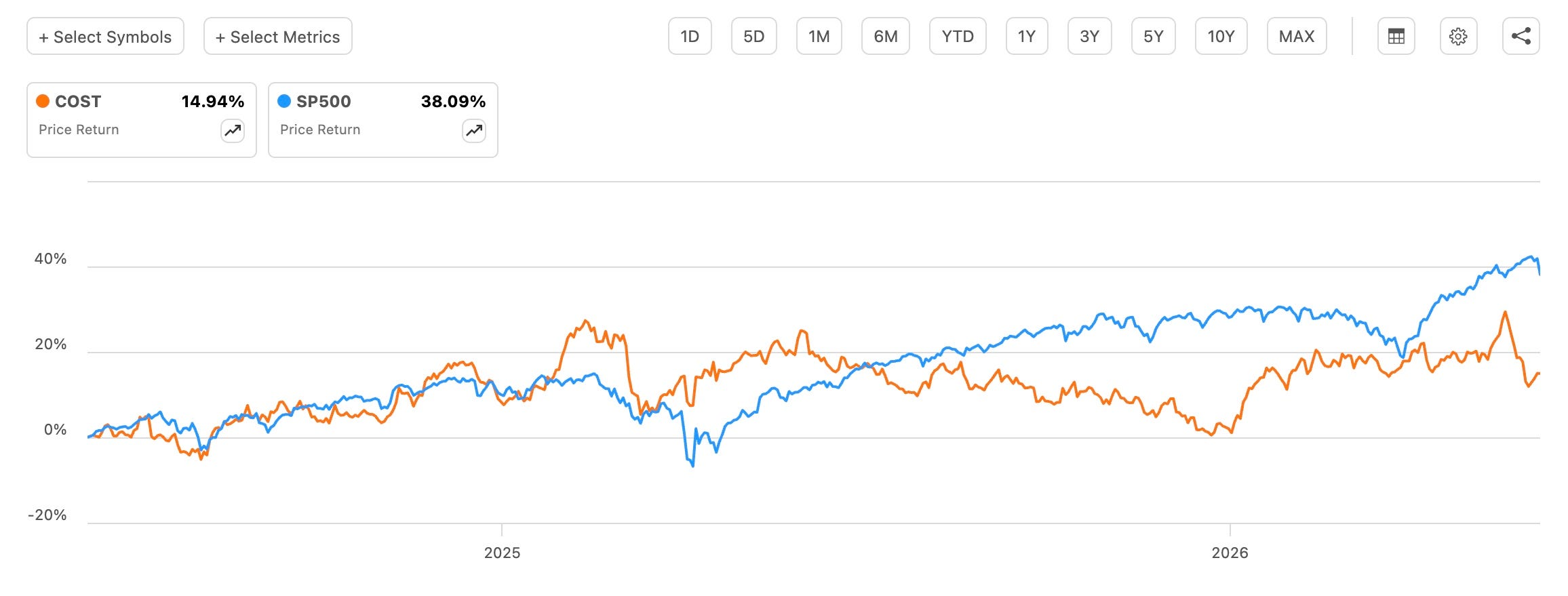

But even great businesses can become poor investments when purchased at excessive prices. Over the past year Costco is in the red, down close to 4%, while the index is up over 24%.

Over the past two years, Costco has continued generating strong business results while significantly underperforming the broader market.

That disconnect highlights the reality that valuation eventually matters. And although Costco deserves to trade at a premium, buying stocks when they’re overpriced puts you at higher risk of underperformance.

Could A Stock Split Help? ⛓️💥

One potential catalyst investors continue discussing is a stock split.

Costco shares briefly approached $1,100 earlier this year, fueling speculation that management could eventually consider one.

The company hasn’t split its stock in more than two decades.

A split would not change anything fundamentally, but it could improve accessibility for smaller retail investors and potentially boost sentiment.

While I don’t view a split as a major driver of long-term returns, it could provide a temporary catalyst for shares if management decides to pursue one.

Final Thoughts ✅

Costco remains one of the highest-quality businesses in the world.

Its membership model, customer loyalty, financial strength, and long-term growth prospects are all exceptional.

If I were building a portfolio designed to own companies for decades, Costco would absolutely deserve consideration.

But investing isn’t just about buying great businesses.

It’s also about paying reasonable prices.

At more than 45x forward earnings, I continue to believe Costco’s valuation leaves little room for meaningful upside while increasing the risk of further relative underperformance.

For existing shareholders, I believe Costco remains a stock worth holding.

For new investors, however, I would remain patient and wait for either a meaningful pullback or a valuation closer to the mid-30x earnings range before becoming more aggressive.

RATING: HOLD

Do you think Costco’s valuation is too rich at the moment? Or does the company’s financials and expansion warrant the valuation? Let me know in the comments.

Just a note to let readers know I will be going paid soon. Be on the lookout for the article laying out the details. Feel free to provide any feedback!

Happy Investing!

☎️ If you’re looking to create passive income and build your wealth from one of the top-rated analysts, book a call (Let’s Talk Investing or Detailed Portfolio Review) with me to get started.

If you’re looking to start investing check out our investment group over on Seeking Alpha.

Here’s How: Click the Seeking Alpha link here. Click investing group, subscribe now (GET AN INVESTING GROUP FREE TRIAL), or the blue hyperlink in my bio.

Not financial advice. For educational purposes only. I am not a licensed professional. Do your own due diligence.

Like & subscribe if you’re active duty, a veteran, or just love investing.