This 4% Yielding Stock Has A Forward P/E Of Just 7x!

"I Expect Shares Could Re-Rate Higher In The Coming Years Giving Investors Massive Growth & Income Potential"

As you know by my name, I love dividends. And in addition to sharing on here, I write regularly on the investment platform- Seeking Alpha.

My goal there is to teach everyday investors about building wealth, so they won’t to need to work to traditional retirement age.

I want to help you take control of your life, have F.I.R.E.

Here at Dividend Collection Agency the goal is to give investors and/or readers a different perspective. We take a simple approach to building wealth. And although investing may seem easy, people often miss opportunities by over complicating it.

But we are here to help.

Current Price: $

Dividend/Yield: $

Since Omnicom Group (OMC) first popped up on my radar a few years ago, shares have been somewhat volatile, bouncing between $80 and $100 a share.

And the stock has always been very interesting to me.

But their lack of growth is one of the main reasons I’ve remained skeptical until now. The company recently acquired another media & advertising giant, Interpublic Group of Companies.

With the acquisition completed, OMC looks attractive as they expect growth to ramp up in the coming years.

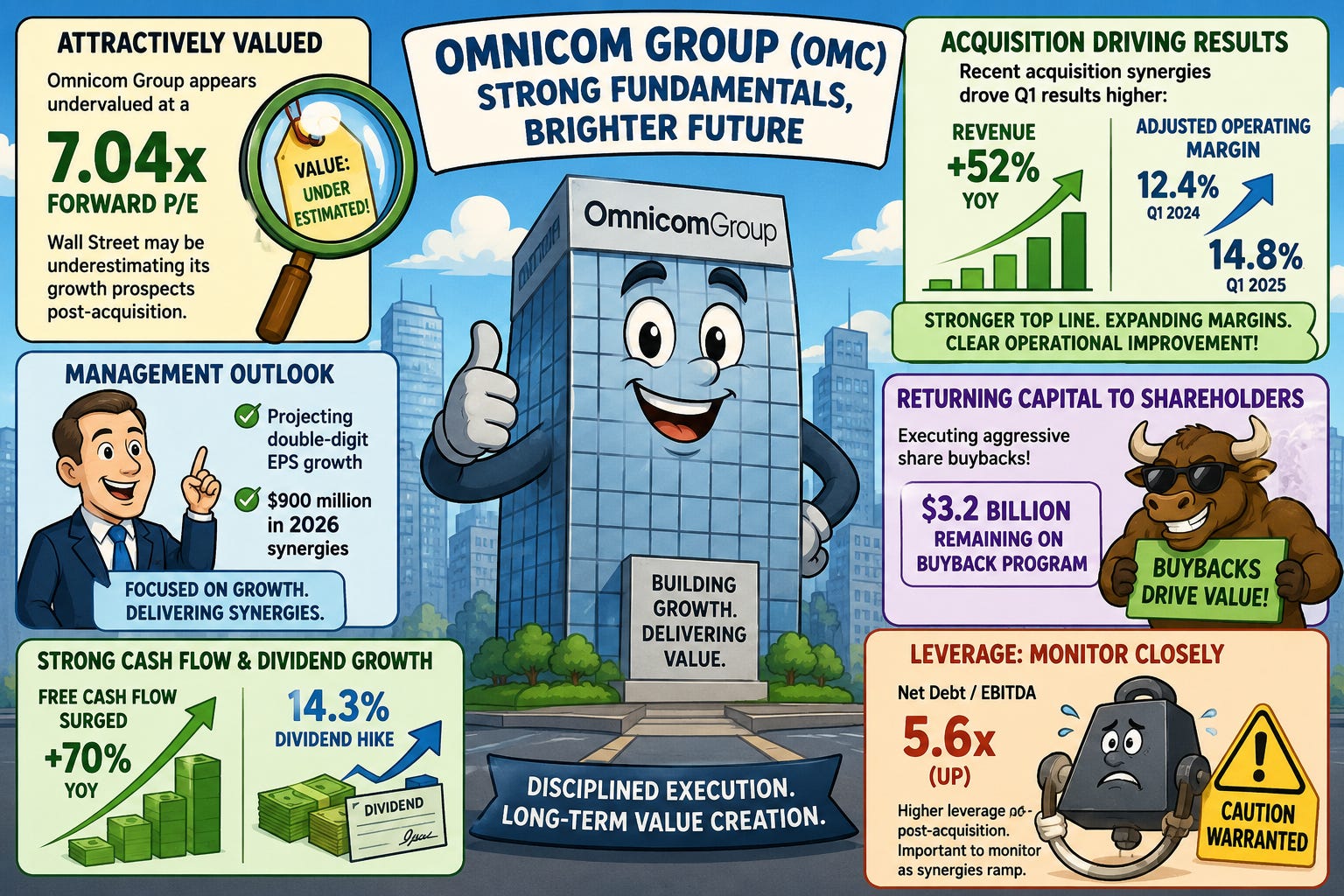

With a forward P/E of just 7.04x, I believe Wall Street may be underestimating OMC and think shares could re-rate in the next 24 to 36 months. Especially, if they can manage to meet growth expectations.

The dividend yield close to 4% is another incentive to invest if looking for an attractively priced stock with massive upside potential.

In this article, I discuss Omnicom Group’s latest earnings, fundamentals, why I believe shares could re-rate in the near future, and why Wall Street may be overlooking this quality compounder.

Acquisition Synergies Seem To Be Paying Off 🚀

As previously mentioned, OMC closed on their acquisition with IPG at the end of last November. And judging by Omnicom’s Q1 earnings report, the media & advertising giant delivered what I thought was strong growth across the board.

Their bottom line grew 11.8%, while revenue surged to $5.6 billion. Organic revenue growth came in at 3.9%, up from 3.4% the prior year.

Adjusted EBITDA increased from $653.1 million to $833.5 million, helping margins expand from 12.4% to 14.8%.

Management attributed the strong growth to portfolio realignment and acquisition synergies.

Although the quarter initially looked mixed on the surface with only a modest EPS beat of $0.06, growth compared to last year’s quarter improved significantly.

During Q1’25, OMC’s earnings per share only grew 1.8% year-over-year, from $1.67 to $1.70. Revenue growth was also far slower at just 1.65%.

This historical lack of growth is likely one of the primary reasons the stock has underperformed over the past 3, 5, and 10 years.

More recently, I think concerns surrounding artificial intelligence adoption and macro uncertainty tied to the Middle East conflict have weighed on shares as well.

And while volatility may continue near term, if management can continue executing through:

Portfolio repositioning

AI integration

Accelerated share buybacks

Acquisition synergies

…I believe Omnicom has a strong chance of seeing a significant price re-rating.

Management reiterated expectations for roughly $900 million in 2026 synergies while also planning to continue aggressively repurchasing shares.

That combination alone could drive strong bottom-line growth over the next several years.

Performance Breakdown 📊

Breaking down Omnicom’s performance further, most segments experienced solid growth during the quarter with the exception of Advertising.

Management did not provide specific reasons for the weakness, but I believe increasing AI adoption among businesses could be impacting demand.

However, as OMC continues integrating IPG’s core assets, I expect growth trends to improve.

During Q1, management disposed of roughly $1 billion in non-core assets and expects additional sales in the coming quarters.

In total, Omnicom plans to divest portfolio assets representing approximately $3.2 billion in annual revenue.

This strategy allows management to focus on core operations expected to drive higher long-term growth.

Their Integrated Media segment led the way with high single-digit growth, while other segments delivered mid-single-digit growth.

Regionally:

U.S. revenue grew nearly 72%

Middle East revenue surged 146%

Latin America revenue climbed 80.9%

Overall, the quarter showed meaningful operational improvement following the acquisition.

Double-Digit EPS Growth Expected 📈

During the quarter, management stated they expect higher double-digit EPS growth in the coming quarters compared to Q1.

One major reason for their confidence appears to be aggressive share repurchases.

In Q1 alone, management repurchased $2.8 billion in stock and still had $3.2 billion remaining under the current authorization.

I fully expect buybacks to remain aggressive throughout the next 12 months and would not be surprised to see management expand the program further.

70% Free Cash Flow Growth 💵

Another factor likely contributing to OMC’s historical underperformance was stagnant dividend growth.

Before the recent 14.3% dividend increase, the payout had remained stuck at $0.70 since 2021.

But thanks to:

Acquisition synergies

Improved cash flow

Aggressive buybacks

…I believe dividend growth should accelerate going forward.

During the quarter, free cash flow surged 70% year-over-year to $656.9 million.

Management paid out just $251.7 million in dividends, resulting in a comfortable payout ratio of only 38.3%.

They also exited 2025 with a payout ratio near 33%, giving them substantial flexibility for future dividend hikes.

If management continues executing, I wouldn’t be surprised to see high single-digit or even double-digit dividend growth moving forward.

Balance Sheet Risks Remain ⚖️

One area investors should continue monitoring closely is leverage.

Net debt-to-EBITDA rose significantly to 5.6x post-acquisition compared to just 1.1x pre-deal.

Net debt increased from $2.7 billion to $5.7 billion, while long-term debt rose from $6.1 billion to $10 billion.

That said, liquidity remains solid with approximately $4.3 billion available.

Debt maturities also appear manageable, with the next major maturity not arriving until July 2027.

Still, reducing leverage should remain a top priority for management moving forward.

Why Shares Could Re-Rate Higher ↗️

Aside from the IPG acquisition and portfolio repositioning, Omnicom is also leaning heavily into AI through the launch of Omni.

Omni is an AI-driven marketing intelligence platform designed to:

Improve media engagement

Increase campaign performance

Boost ROI

Enhance brand scale and efficiency

Management also announced expanded client relationships during the quarter with companies including:

Exxon Mobil (XOM)

Delta Air Lines (DAL)

Clorox (CLX)

Merck & Co. (MRK)

Kroger (KR)

Although integration will take time, I believe Omnicom has a strong chance of seeing shares re-rate over the next 24 to 36 months.

At the current share price around $77 and using 2026 EPS estimates of $10.92, OMC trades at just 7.04x forward earnings.

That valuation appears far too cheap if management can deliver:

Double-digit EPS growth

Synergy realization

Higher margins

Accelerated dividend growth

At current levels, investors also collect a well-covered dividend yield near 4%.

Risks To Consider ⚠️

Despite my bullishness, risks remain.

The current macro environment could continue pressuring shares due to:

Higher-for-longer interest rates

Inflation concerns

Geopolitical instability

AI disruption risks

Additionally, the increased debt load post-acquisition may limit upside until investors gain more confidence in deleveraging progress.

Businesses increasingly adopting AI internally may also reduce demand for traditional advertising services over time.

Still, I believe Omnicom is positioning itself well through:

Portfolio optimization

AI integration

Buybacks

Synergy realization

Strong free cash flow generation

Bottom Line ✅

While I expect volatility to persist in the near to medium term, I believe Omnicom Group presents one of the more compelling long-term value opportunities in the market today.

The combination of:

A forward P/E of just 7.04x

A dividend yield near 4%

Accelerating free cash flow

Double-digit EPS growth expectations

Aggressive buybacks

AI integration

Post-merger synergies

…creates a compelling setup for long-term investors.

If management can continue executing successfully, I believe Wall Street will eventually assign OMC a significantly higher valuation multiple.

As a result, I am doubling down on my buy rating and believe shares offer attractive upside potential over the next 24 to 36 months.

Is Omnicom a stock for your portfolio? Let me know in the comments.

Just a note to let readers know I will be going paid soon. Be on the lookout for the article laying out the details. Feel free to provide any feedback!

Happy Investing!

☎️ If you’re looking to create passive income and build your wealth from one of the top-rated analysts, book a call (Let’s Talk Investing or Detailed Portfolio Review) with me to get started.

If you’re looking to start investing check out our investment group over on Seeking Alpha.

Here’s How: Click the Seeking Alpha link here. Click investing group, subscribe now (GET AN INVESTING GROUP FREE TRIAL), or the blue hyperlink in my bio.

Not financial advice. For educational purposes only. I am not a licensed professional. Do your own due diligence.

Like & subscribe if you’re active duty, a veteran, or just love investing.