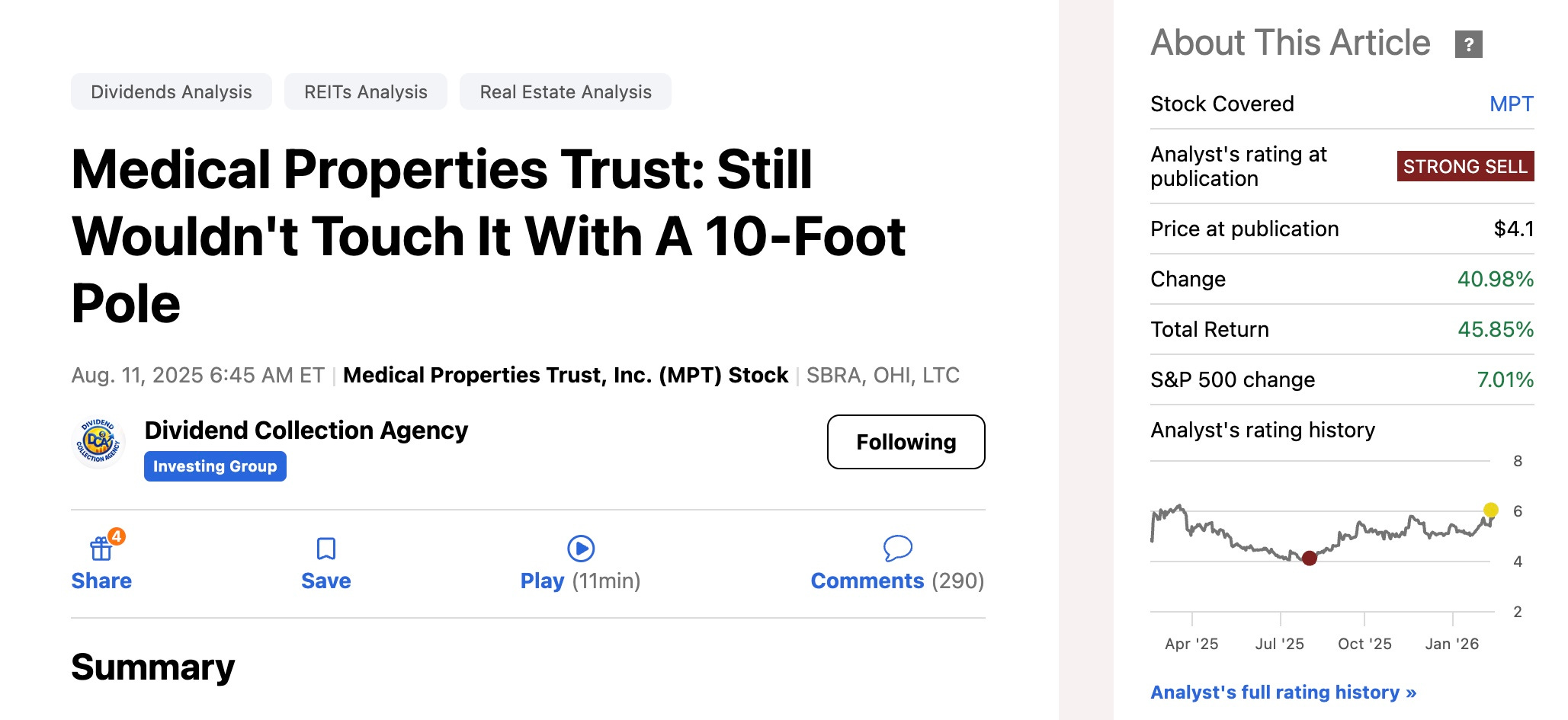

This Beaten Down Healthcare REIT Turnaround Seems To Be In Full Swing

"Is Medical Properties Trust Near 6% Yield Worth It Now?"

As you know by my name, I love dividends. And in addition to sharing on here, I write regularly on the investment platform- Seeking Alpha.

My goal there is to teach everyday investors about building wealth, so they won’t to need to work to traditional retirement age.

I want to help you take control of your life, have F.I.R.E.

Here at Dividend Collection Agency the goal is to give investors and/or readers a different perspective. We take a simple approach to building wealth. And although investing may seem easy, people often miss opportunities by over complicating it.

But we are here to help.

Current Price: $5.78

Portfolio Purpose: Income 💰

Although I don’t currently own shares of Medical Properties Trust (MPT), I’m very familiar with the name. I previously held shares, attracted by the high yield, essential hospital real estate, and the narrative that hospitals are “recession-resistant.”

Long story short — I exited at a small loss as tenant issues and balance sheet risk began stacking up.

Since then, the stock continued to slide… until recently.

Over the past year, shares are up more than 20%, and roughly 40%+ in just the last six months. That kind of move suggests the market believes the turnaround is gaining real traction.

After reviewing the latest earnings, I believe the improvement is real — but the balance sheet still prevents me from getting overly bullish.

I’m upgrading MPT to a Hold.

A Quick Look Back 👀

Six months ago on Seeking Alpha, I was firmly negative on the stock.

Revenue and FFO were declining year-over-year. Tenant credit quality was deteriorating. Impairment charges were piling up. And leverage was far above my comfort zone.

At the time, I believed any turnaround would take longer than the market expected.

Since that call, shares have rallied sharply. The question now becomes:

Has enough fundamentally changed?

Q3: Early Signs of Stabilization ↔️

Q3 showed incremental progress:

FFO met expectations

Revenue came in at $237.5M (slightly light versus estimates)

Cash rent collections improved

Re-tenanting of six California properties boosted visibility

However, year-to-date revenue remained down, and normalized FFO declined year-over-year due to impairment charges — including fallout from the January 2025 bankruptcy of Prospect Medical Holdings.

The quarter suggested stabilization, but not a full recovery.

Q4: A Real Step Forward ➡️

Q4 was much stronger and frankly surprised me.

FFO: $0.18 (beat by $0.03)

Revenue: $270.3M (up sharply from Q3 and up meaningfully year-over-year)

Full-year FFO exceeded expectations

Key positives:

New leases signed on six former Prospect properties

Expected $45M increase in rent by year-end

$18M one-time payment from Vibra restructuring

$32M acquisition

Active share buybacks

Sequential improvement in both FFO and revenue is exactly what a turnaround needs to show.

But it’s important to zoom out:

Full-year revenue is still below prior levels, and straight-line rent declined year-over-year — which tells me some structural pressure remains.

The Dividend Hike & Buybacks 💵

Management increased the dividend by 12.5% to $0.09 per share.

That was surprising — and clearly a confidence signal.

Despite normalized FFO declining 28% year-over-year, the payout ratio sits near 57%, which is manageable on current guidance.

The $150M buyback program and active repurchases in Q4 further reinforce management’s confidence in liquidity and forward visibility.

For income-focused investors, that matters.

The Real Concern: Leverage 💸

This is where I remain cautious.

MPT’s leverage sits near 9.6x — well above my preferred 5.0x–5.5x range for REITs.

For comparison:

Sabra Health Care REIT (SBRA) operates around ~5.0x

National Health Investors (NHI) sits near ~3.6x

LTC Properties (LTC) is roughly ~5.6x

Upcoming maturities are meaningful:

2026: $1.1B+

2027: $1.6B

Liquidity is solid today — over $1B available on the revolver plus cash — and 92% of debt is fixed-rate. That helps.

But leverage at this level leaves little margin for error.

If tenant stress resurfaces, flexibility shrinks quickly.

Valuation: Discounted for a Reason 🏷️

Using 2026 FFO expectations of roughly $0.65, MPT trades around 8x forward earnings.

Peers trade significantly higher:

Sabra Health Care REIT ~13x+

Omega Healthcare Investors (OHI) ~15x

The discount reflects risk — primarily leverage and tenant credit exposure.

Near term, I expect shares to consolidate around the $6 range unless further sequential improvement is demonstrated.

If execution continues and leverage trends lower, I could see $8 by late 2026.

But that’s conditional on continued operational progress.

Risks to Watch ⚠️

Tenant credit deterioration

Additional bankruptcies

Medicaid reimbursement pressure

Refinancing risk in 2026–2027

High leverage limiting flexibility

Economic slowdown impacting hospital operators

Turnarounds fail when liquidity tightens. That’s the core risk here.

Bottom Line ✅

Medical Properties Trust is unquestionably in better shape than it was six months ago.

Sequential FFO growth. Revenue improvement. Dividend increase. Buybacks. Re-tenanting progress.

Those are meaningful steps forward.

However:

Revenue remains below historical levels

Leverage remains elevated

Tenant quality remains a concern

For now, that combination keeps me at Hold.

If management can show sustained FFO growth while meaningfully reducing leverage by the end of 2026, I would consider upgrading to a Buy.

Until then, investors are being paid a solid yield — but they are accepting above-average risk to earn it.

Turnarounds can be profitable — but patience and balance sheet discipline matter.

Do you think Medical Properties Trust will make a successful turnaround? Let me know in the comments.

Happy Investing!

☎️ If you’re looking to create passive income and build your wealth from one of the top-rated analysts, book a call (Let’s Talk Investing or Detailed Portfolio Review) with me to get started.

If you’re looking to start investing check out our investment group over on Seeking Alpha.

Here’s How: Click the Seeking Alpha link here. Click investing group, subscribe now, or the blue hyperlink in my bio.

Not financial advice. For educational purposes only. I am not a licensed professional. Do your own due diligence.

Like & subscribe if you’re active duty, a veteran, or just love investing.