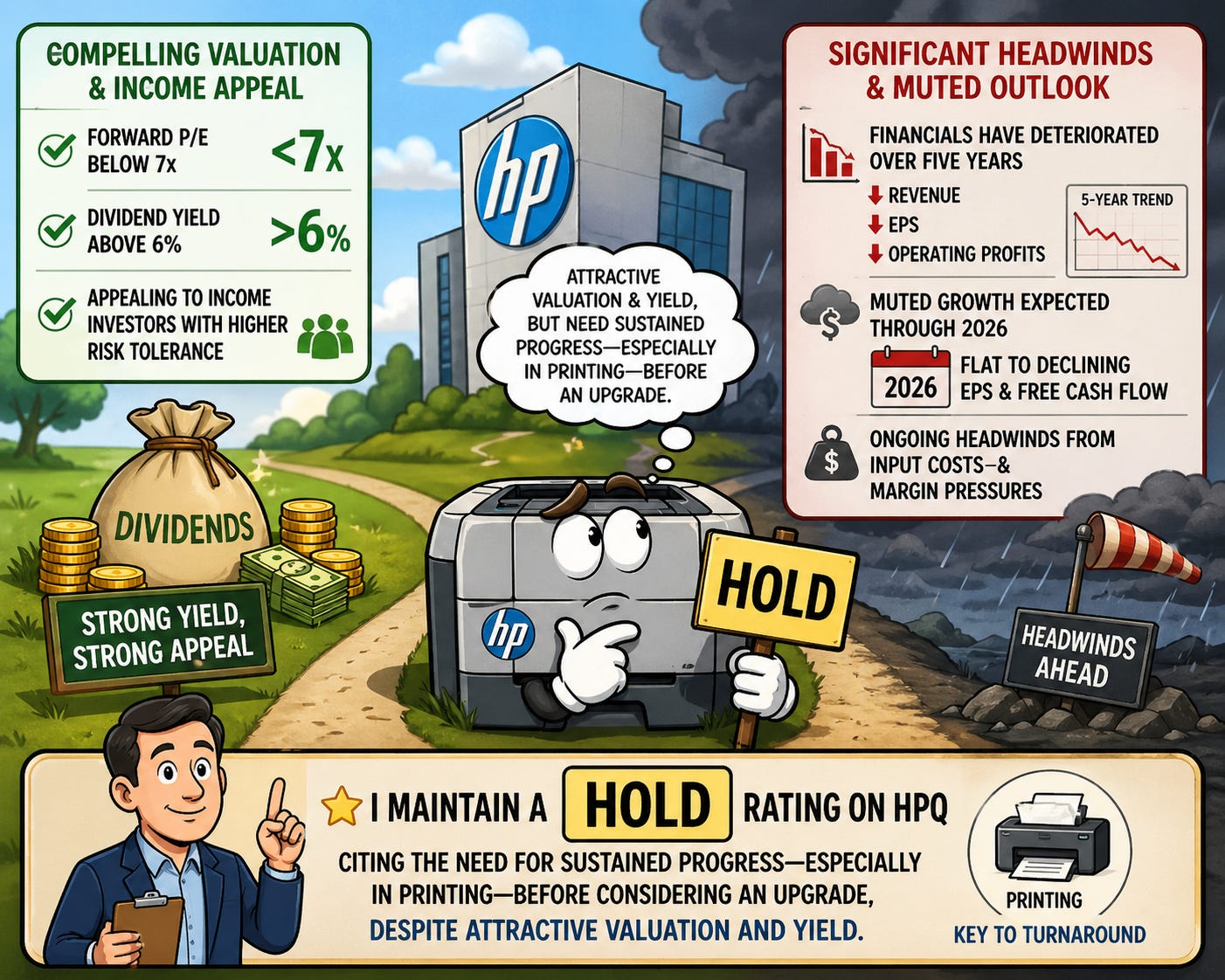

This Beaten-Down Technology Stock Offers A 6% Yield And Forward P/E Below 7x

"Appealing To Income Investors With A Higher Risk Tolerance"

As you know by my name, I love dividends. And in addition to sharing on here, I write regularly on the investment platform- Seeking Alpha.

My goal there is to teach everyday investors about building wealth, so they won’t to need to work to traditional retirement age.

I want to help you take control of your life, have F.I.R.E.

Here at Dividend Collection Agency the goal is to give investors and/or readers a different perspective. We take a simple approach to building wealth. And although investing may seem easy, people often miss opportunities by over complicating it.

But we are here to help.

Current Price: $19.73

Dividend/Yield: $0.30/6.08%

At a time when the market continues pushing toward new highs, finding attractively priced stocks is becoming increasingly difficult.

But there’s always an opportunity somewhere.

In the case of HP Inc. (HPQ), the past five years have been disappointing. However, with a forward P/E below 7x and a dividend yield north of 6%, the investment case is hard to ignore. Especially, for income-focused investors willing to take on some risk.

While I remain cautious in the near term, I do believe HPQ could offer compelling long-term upside if management can execute.

Brief Overview 📖

HP Inc. is a well-known name in the Technology (XLK) sector, primarily focused on:

Printing (core profit driver)

Personal Systems (PCs & devices)

Corporate Investments / Other

Founded in 1939 and public since 1957, HPQ separated from Hewlett Packard Enterprise (HPE) in 2015.

Latest Earnings: A “Beat”… But Underwhelming 📊

HPQ delivered a double beat in Q1:

EPS: $0.81 (+ $0.04 beat)

Revenue: $14.4B (+ $510M beat)

But here’s the issue:

Revenue declined sequentially from $14.6B.

EPS dropped from $0.93

So yes, they beat—but momentum is still lacking.

What drove results?

Personal Systems: +11% revenue growth

Printing: -2% revenue decline (still the key segment)

Margins also slipped:

Printing: 19% → 18.3%

Personal Systems: 5.5% → 5.0%

Bottom line: modest improvements, but headwinds remain firmly in place.

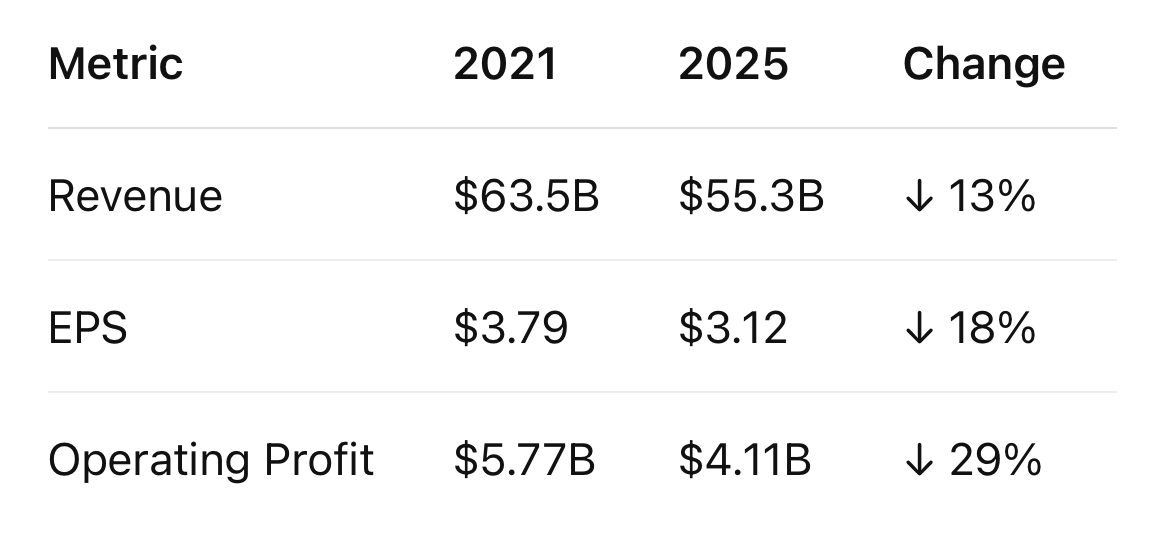

The Real Problem: 5-Year Deterioration 🚧

Zooming out tells the real story.

That’s why the stock has struggled—down significantly while the S&P 500 surged. This isn’t just a bad year—it’s a multi-year deterioration trend.

Muted Growth Ahead (Through 2026) ↔️

Management isn’t exactly signaling a turnaround—yet.

2026 EPS: expected to decline ~2%

Free Cash Flow: flat (~$2.9B midpoint)

Q2 EPS guidance: $0.70–$0.76 (~10% sequential decline)

Key headwinds:

Rising DRAM & NAND costs

Margin pressure

Tariffs & inflation impacts

Expect more of the same for at least another year.

Dividend Profile: The Real Appeal 💰

Here’s where HPQ gets interesting.

Dividend Yield: >6%

Payout Ratio: ~37%

2025 FCF: $2.93B vs $1.09B dividends

Even with declining financials, the dividend is:

✔ Well-covered

✔ Sustainable (for now)

✔ Likely to grow slowly

HPQ also raised its dividend 4% recently, signaling confidence. This is not a growth story—it’s an income play.

Can AI Save the Story? 🤖

Management is betting on AI to reignite growth:

New AI-powered PCs & printers

Partnerships with Intel and Autodesk

Collaboration with OpenAI on enterprise solutions

The strategy makes sense. But execution—and timing—are everything.

Analysts expect:

Growth to return in 2027

More meaningful expansion in 2028

Valuation: Cheap… For a Reason 🏷️

Forward P/E: ~6.9x. Historical “normal” multiple: ~9.8x.

If HPQ re-rates, there’s upside.

Even compared to Dell Technologies (DELL) trading at a much higher multiple, HPQ looks discounted.

But low multiples often signal low expectations—or structural issues.

Risks to Watch ⚠️

Continued Printing segment weakness

Persistent input cost inflation

Execution risk on AI initiatives

Macro volatility (rates, tariffs, demand)

If Printing doesn’t stabilize, the stock could continue drifting lower.

Bottom Line ✅

HPQ checks a lot of boxes:

✔ Valuation

✔ High dividend yield

✔ Potential long-term upside

But…

❌ Weak long-term financial trends

❌ Limited near-term growth

❌ Ongoing margin pressure

Despite the compelling yield and low valuation, I’m maintaining a Hold rating.

I want to see:

Sustained improvement in Printing

Stabilization in margins

Clear signs of growth returning

Until then, HPQ remains: A high-yield opportunity… but one that requires patience.

Do you think HPQ can weather the storm and see long term growth? Let me know in the comments.

Just a note to let readers know I will be going paid May 1st. Be on the lookout for the article laying out the details. Feel free to provide any feedback!

Happy Investing!

☎️ If you’re looking to create passive income and build your wealth from one of the top-rated analysts, book a call (Let’s Talk Investing or Detailed Portfolio Review) with me to get started.

If you’re looking to start investing check out our investment group over on Seeking Alpha.

Here’s How: Click the Seeking Alpha link here. Click investing group, subscribe now (GET AN INVESTING GROUP FREE TRIAL), or the blue hyperlink in my bio.

Not financial advice. For educational purposes only. I am not a licensed professional. Do your own due diligence.

Like & subscribe if you’re active duty, a veteran, or just love investing.