This Consumer Staple Has a 6% Yield And Paid A Consecutive Dividend Since 1989

"Down 28% In The Past Year, This Low P/E Stock May Be Attractive"

As you know by my name, I love dividends. And in addition to sharing on here, I write regularly on the investment platform- Seeking Alpha.

My goal there is to teach everyday investors about building wealth, so they won’t to need to work to traditional retirement age.

Thanks for reading! Subscribe for free to receive new posts and support my work.

I want to help you take control of your life, have F.I.R.E.

Here at Dividend Collection Agency the goal is to give investors and/or readers a different perspective. We take a simple approach to building wealth. And although investing may seem easy, people often miss opportunities by over complicating it.

But we are here to help.

Current Price: $21.25

Dividend/Yield: $0.29/5.55%

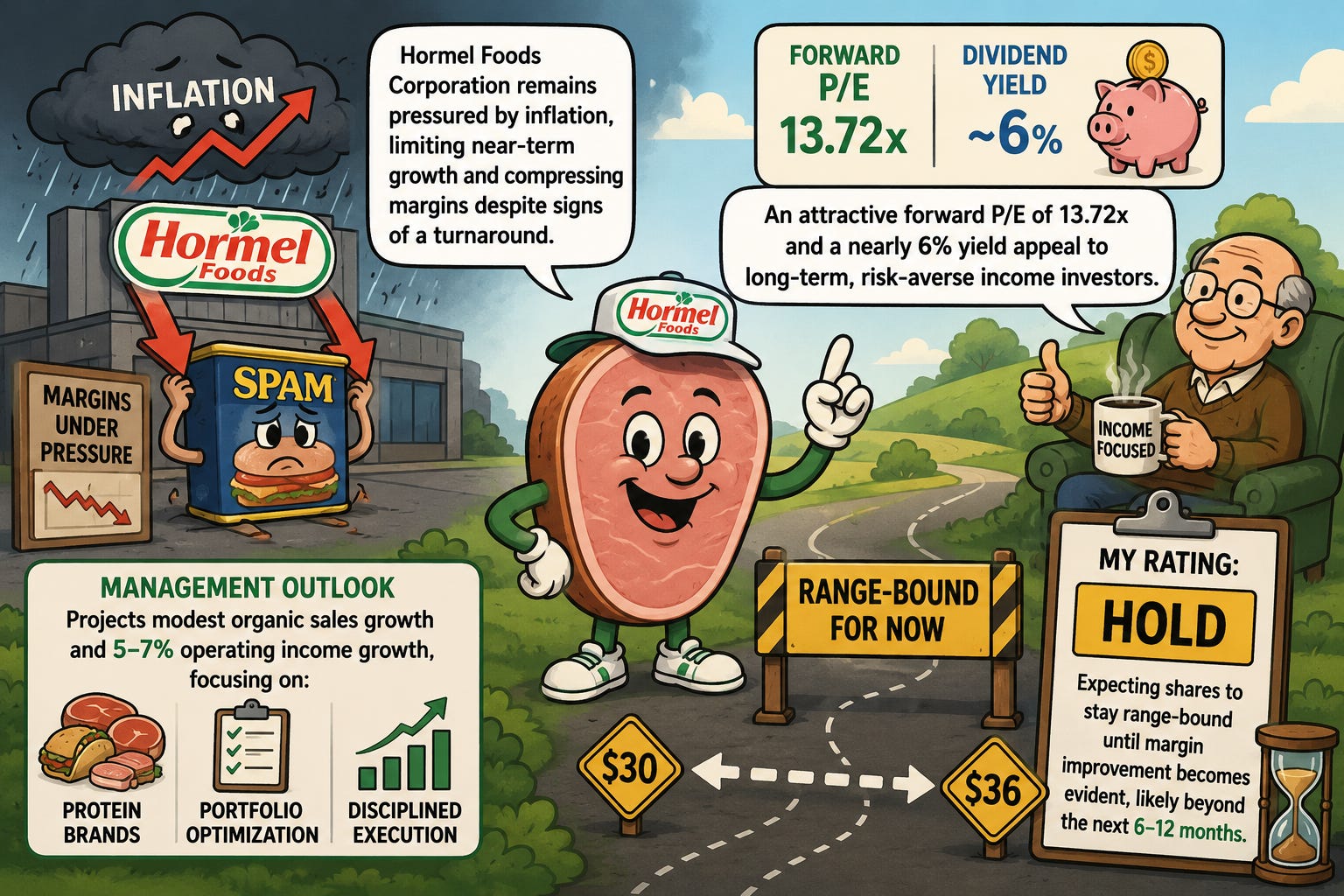

Inflation has not been kind to many businesses, especially those heavily reliant on consumer spending and discretionary grocery purchases.

Due to ongoing geopolitical tensions and growing economic uncertainty, inflation concerns have resurfaced once again after April’s hotter-than-expected CPI report showed inflation rising to 3.8%.

As a result, consumers continue shifting toward value-oriented alternatives, benefiting retailers like Costco (COST) and Walmart (WMT) while pressuring branded food companies such as Hormel Foods (HRL).

That ongoing pressure is one of the biggest reasons Hormel continues struggling to regain momentum despite signs of stabilization beginning to emerge.

However, at a forward P/E of just 13.72x alongside a dividend yield nearing 6%, the risk/reward profile is becoming increasingly attractive for patient, long-term income investors willing to tolerate continued volatility.

In this article, I discuss Hormel’s latest earnings, expectations for their upcoming Q2 report, and why I continue to maintain a Hold rating despite the depressed valuation and elevated yield.

Portfolio Transition Showing Some Progress 📊

Although Hormel continues facing macro headwinds, there were some encouraging developments throughout 2025.

All three operating segments managed positive growth:

Segment Performance

Retail: +1%

Foodservice: +5%

International: +1%

Foodservice remains the strongest-performing business currently, benefiting from resilient demand and pricing actions.

For the year:

Organic sales growth totaled 2%

Revenue increased to $12.1 billion

EPS declined from $1.47 to $1.37

Unfortunately, profitability remains the core issue.

Margin Pressure Continues

Cash from operations declined from $1.3B to $845M

Operating income fell from $1.1B to $719M

Adjusted operating margin compressed from 9.6% to 8.4%

Persistent inflation and elevated input costs continue weighing heavily on profitability despite revenue stabilization.

Q1 Earnings: Stabilization Emerging 🤔

During Q1 earnings in February, Hormel delivered:

Q1 Highlights

2% organic sales growth

Fifth consecutive quarter of positive organic growth

EPS of $0.34

Strong Foodservice and International performance

Management credited much of the stabilization to their growing focus on protein-oriented products as consumer trends continue shifting toward high-protein diets and healthier food choices.

Segment Breakdown

Retail:

Sales declined 2%

Continued weakness from exiting non-core snack nut business

Foodservice:

Sales grew 7%

International:

Sales grew 8%

The Retail segment remains the primary concern moving forward, particularly as inflation pressures consumers toward lower-cost alternatives and private-label products.

Management’s Long-Term Strategy ♟

Hormel continues repositioning the portfolio toward:

Protein-powered brands

Higher-margin products

Operational optimization

Divestiture of lower-growth assets

One of the biggest strategic changes is the divestiture of the turkey business, which management expects will reduce annual revenue by roughly $50 million but have minimal earnings impact.

Long-term, management expects:

2%–3% annual sales growth

5%–7% operating income growth

While those growth rates are not overly exciting, they do suggest Hormel may finally be entering a more stable operating environment after several difficult years.

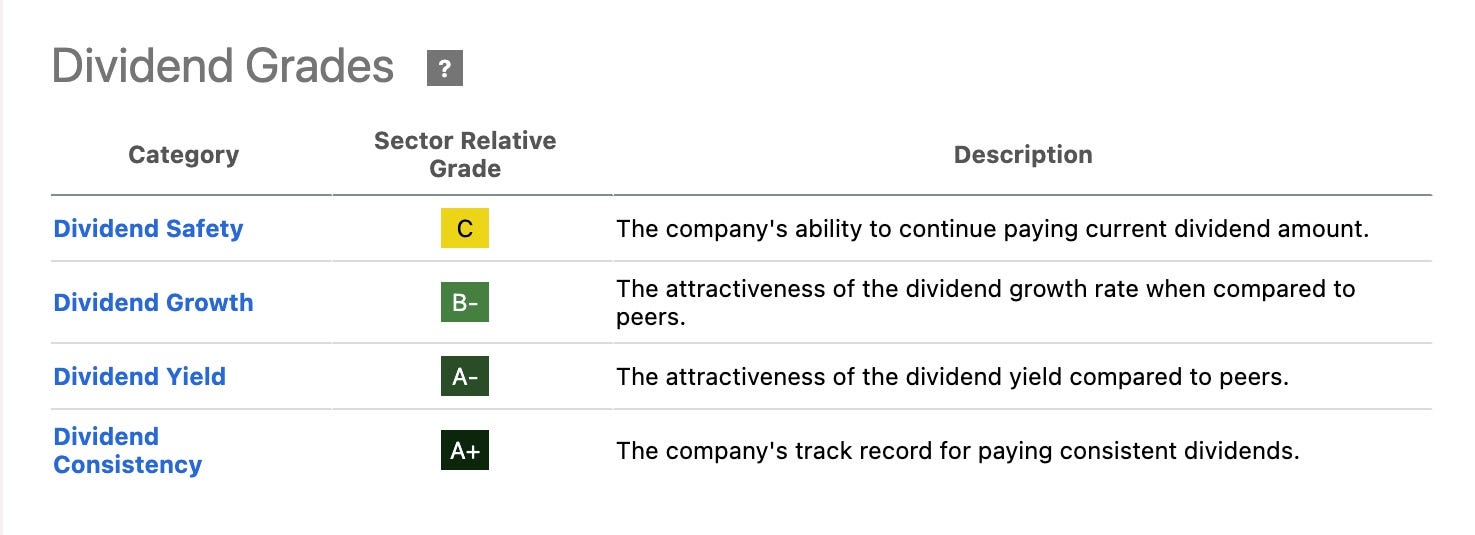

Dividend & Balance Sheet Remain Bright Spots 💵

Despite operational challenges, Hormel’s dividend remains relatively safe and well-covered.

Dividend Highlights

Payout ratio: 57%

Dividend Aristocrat status maintained

Yield approaching 6%

Cash generation also remains adequate:

Cash from operations: $349M

Capital expenditures: $69M

Dividends paid: $160M

The balance sheet remains healthy as well.

Balance Sheet Snapshot

Long-term debt: $2.85B

Cash & equivalents: $868M

Minimal near-term debt maturities

Management continues prioritizing investment-grade credit quality, giving Hormel flexibility to continue restructuring operations while supporting dividend growth.

Don’t Expect Much From Q2

Hormel reports Q2 earnings on May 28th, and personally, I do not expect major improvement.

Management already guided for:

Modest top-line growth

Mostly flat profitability

Current analyst expectations call for:

Slight EPS improvement

Revenue decline to roughly $2.96B

My Expectations

EPS: $0.34–$0.37

Revenue: $3.0B–$3.06B

The two biggest things investors should monitor:

Margins

Retail segment stabilization

If inflation remains elevated, margins could continue compressing, which would likely pressure shares further.

Valuation Looks Attractive 📉

Using guidance midpoint EPS of $1.47, Hormel trades at a forward P/E of just 13.72x.

That remains well below its:

5-year average multiple of 21.62x

Even compared to peers like:

Kraft Heinz (KHC)

The Campbell’s Company (CPB)

Hormel still offers a respectable combination of:

Defensive characteristics

Dividend reliability

Long-term brand strength

However, valuation alone is not enough to drive upside if margins continue deteriorating.

Why I’m Still Holding, Not Buying ⚠️

While the valuation and dividend are becoming increasingly attractive, I still believe near-term risks outweigh rewards.

Reasons For Caution

Inflation remains elevated

Consumer spending trends remain weak

Retail segment stabilization is still uncertain

Margins continue facing pressure

Management growth expectations remain modest

Near-term, I expect shares to remain mostly range-bound until:

Inflation moderates

Margins improve sequentially

Retail performance stabilizes

If margin recovery becomes more evident, I could eventually see shares moving toward the $22–$25 range over time.

But for now, patience is likely required.

Bottom Line ✅

From an income and valuation perspective, Hormel Foods is beginning to look increasingly attractive for long-term investors with higher risk tolerance.

The nearly 6% dividend yield, Dividend Aristocrat status, and depressed valuation all provide meaningful long-term upside potential if management successfully stabilizes margins and executes its portfolio transition.

However, inflationary pressures and changing consumer behavior will likely continue limiting profitability and growth over the near-to-medium term.

Is Hormel worth the 6% dividend? Let me know in the comments.

Just a note to let readers know I will be going paid soon. Be on the lookout for the article laying out the details. Feel free to provide any feedback!

Happy Investing!

☎️ If you’re looking to create passive income and build your wealth from one of the top-rated analysts, book a call (Let’s Talk Investing or Detailed Portfolio Review) with me to get started.

If you’re looking to start investing check out our investment group over on Seeking Alpha.

Here’s How: Click the Seeking Alpha link here. Click investing group, subscribe now (GET AN INVESTING GROUP FREE TRIAL), or the blue hyperlink in my bio.

Not financial advice. For educational purposes only. I am not a licensed professional. Do your own due diligence.

Like & subscribe if you’re active duty, a veteran, or just love investing.