This Dividend Growth Stock Has Outperformed - But Its Valuation Is Getting Dangerous

"Casey's Is Worth A Look On A Price Correction"

As you know by my name, I love dividends. And in addition to sharing on here, I write regularly on the investment platform- Seeking Alpha.

My goal there is to teach everyday investors about building wealth, so they won’t to need to work to traditional retirement age.

I want to help you take control of your life, have F.I.R.E.

Here at Dividend Collection Agency the goal is to give investors and/or readers a different perspective. We take a simple approach to building wealth. And although investing may seem easy, people often miss opportunities by over complicating it.

But we are here to help.

Current Price: $660.87

Dividend/Yield: $2.28 / 0.35%

Some investors may already be familiar with Casey’s General Stores (CASY), depending on what part of the country they live in. Personally, I’ve never stepped foot in a Casey’s location. But my girlfriend swears by their breakfast pizza, a favorite from childhood. And roughly two years ago, the stock appeared on my radar — and I immediately became bullish.

At the time, I assigned the company a buy rating, and since then the stock has significantly outperformed the S&P 500. Over the past two years, Casey’s has delivered strong returns backed by impressive operational growth.

However, despite being one of my favorite dividend growth companies, I can’t help but question whether the stock has now entered overvaluation territory.

In some ways, the situation reminds me of Costco (COST) — another fantastic company whose valuation has simply become too rich.

Both businesses deserve a premium multiple. But paying too much for even the highest-quality companies can lead to underperformance.

With CASY currently trading at a forward P/E above 38x, investors may already be pricing in a large portion of the company’s future growth.

Latest Results 📊

Casey’s most recent Q3 earnings report delivered mixed results.

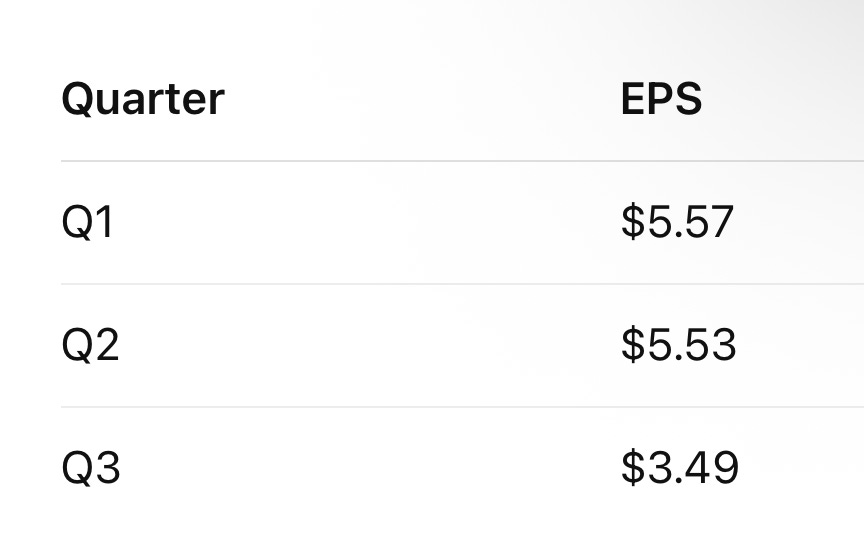

While EPS again beat expectations by $0.52, revenue missed estimates by roughly $120 million.

EPS: $3.49 (up nearly 50% from $2.33 a year ago)

Revenue: $3.92 billion (essentially flat year-over-year)

The modest revenue growth raises a key question:

Has the market already priced in most of Casey’s future growth?

The company has experienced rapid expansion over the last several years.

In 2025 alone:

✔️ 35 new stores were opened

✔️ 235 stores were acquired

✔️ Total store count reached 2,904 locations

The year prior also saw aggressive expansion through both new builds and acquisitions, including the Fike’s acquisition.

Looking ahead to FY2026, management expects to open 80 additional stores, continuing the company’s growth strategy.

However, one trend worth noting is that earnings have declined sequentially over the last three quarters:

Revenue has also declined sequentially:

Q1: $4.57B

Q2: $4.51B

Q3: $3.92B

Net income fell to $130.1 million, down from:

$206 million in Q2

$215.4 million in Q1

However, year-over-year results remain strong, with net income rising from $87 million in the prior year’s quarter.

Operational performance was still solid overall:

Same-store sales: +4%

Inside gross profit: +8.9% to $624M

Gross margins: improved to 42.2% (from 40.9% last year)

Strong Outlook 💪🏾

Despite the mixed quarter, management’s outlook remains optimistic.

For FY2026, Casey’s expects:

80 new store openings

EBITDA growth of 18–20%

Inside same-store sales growth of 3.5%–4.5%

Gross margins between 41.5%–42.5%

During the quarter, EBITDA increased 27.5% to $308.9 million.

Casey’s unique positioning continues to support long-term growth.

Two-thirds of its stores are located in small towns with populations under 20,000, helping create strong customer loyalty and less direct competition.

The company also surpassed 10 million rewards members, which should further strengthen customer retention and sales growth.

Robust Cash Flow & Balance Sheet ⚖️

Although Casey’s dividend yield is relatively modest, the company has been a growth powerhouse.

The quarterly dividend currently sits at $0.57 per share, and the payout remains extremely well covered.

In 2025:

Free Cash Flow: $584.6 million

FCF payout ratio: roughly 12%

Management also expects $1.25 billion in free cash flow by the end of the fiscal year.

The company continues to return capital through share buybacks as well.

During the most recent quarter:

$76 million in shares were repurchased

This was more than double the previous two quarters

Casey’s still has $138 million remaining under its authorization, which should continue supporting EPS growth.

The balance sheet also remains strong:

Net debt: $2.92 billion

Leverage: 1.7x (below management’s 2.0x target)

Liquidity: $1.4 billion

For comparison, this leverage level is slightly lower than Kroger (KR).

Where Do Shares Go From Here? ↕️

Like Costco, Casey’s appears to be trading at a very rich valuation.

Costco currently trades near 50x forward earnings, and Casey’s sits just behind at roughly 38x forward earnings.

Both companies are fantastic businesses with strong balance sheets and shareholder returns.

But investors today appear to be paying a large premium for safety amid economic uncertainty.

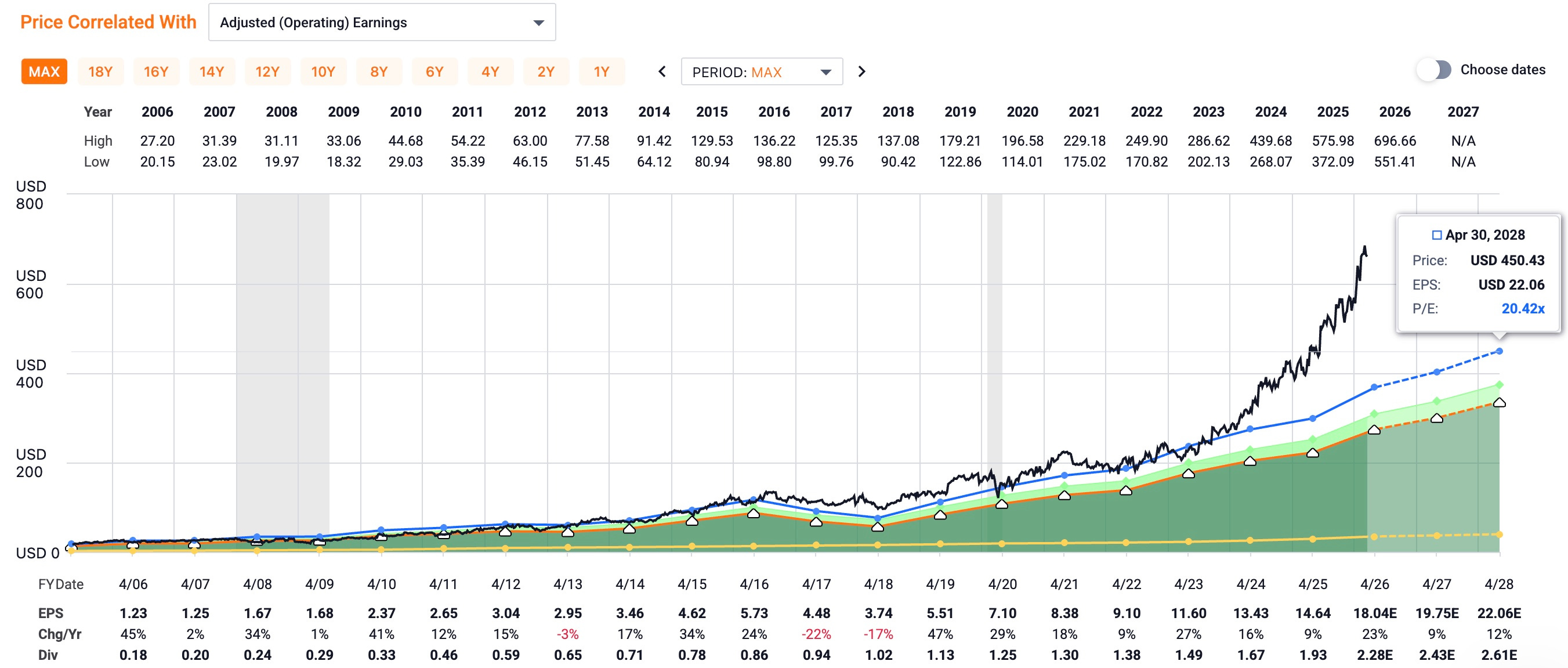

Based on 2026 earnings estimates, Casey’s forward P/E sits around 38.1x, well above its historical average.

In my opinion, a more reasonable valuation would be 25x–30x earnings.

When valuations expand too far above historical norms, future returns often slow.

Even Costco — despite strong fundamentals — has seen its stock move mostly sideways for long stretches.

I believe Casey’s could experience a similar outcome.

After rising 74% in the past year alone, the stock may struggle to continue climbing without stronger fundamental acceleration.

If we were to see a broader market correction, a 20–30% pullback in Casey’s would not be surprising.

If we were to see a broader market correction, a 20–30% pullback in Casey’s would not be surprising.

If you’re looking for a stock analyzer tool that gives you future price targets based on historical data, use my code to get 25% off of FAST Graphs, my go-to the stock analyzer tool for research.

Macro Risks ⚠️

Another risk investors should consider is the broader macro environment.

Markets have begun pricing in increasing recession risk, particularly with rising geopolitical tensions and the ongoing conflict involving Iran.

If these tensions persist, the probability of an economic slowdown could increase.

Recent labor data Recent also suggests the job market may be weakening.

February’s report showed a loss of 92,000 jobs, which could pressure consumer spending and eventually impact Casey’s sales growth.

Bottom Line ✅

Casey’s General Stores remains a high-quality company with strong long-term fundamentals.

The company continues to expand its store base, grow EBITDA at double-digit rates, and maintain strong margins.

Management’s plan to open 80 additional stores this fiscal year, combined with aggressive share repurchases, should continue supporting earnings growth.

However, sequential declines in earnings and flat revenue growth could signal that momentum is slowing.

With the stock trading at a forward P/E above 38x, I believe much of Casey’s future growth has already been priced in.

For that reason, while I still believe Casey’s is a business worth holding, the current valuation leaves little margin of safety.

I maintain my HOLD rating and would prefer to wait for a 20–30% pullback before considering new positions.

Do you think Casey’s is overvalued at the moment? Let me know in the comments.

Happy Investing!

☎️ If you’re looking to create passive income and build your wealth from one of the top-rated analysts, book a call (Let’s Talk Investing or Detailed Portfolio Review) with me to get started.

If you’re looking to start investing check out our investment group over on Seeking Alpha.

Here’s How: Click the Seeking Alpha link here. Click investing group, subscribe now, or the blue hyperlink in my bio.

Not financial advice. For educational purposes only. I am not a licensed professional. Do your own due diligence.

Like & subscribe if you’re active duty, a veteran, or just love investing.