This Dividend Stock Has A P/E Less Than 10x And 60%+ Upside Potential

"Build-A-Bear's Pullback Is A Gift For Long-Term Investors"

As you know by my name, I love dividends. And in addition to sharing on here, I write regularly on the investment platform- Seeking Alpha.

My goal there is to teach everyday investors about building wealth, so they won’t to need to work to traditional retirement age.

I want to help you take control of your life, have F.I.R.E.

Here at Dividend Collection Agency the goal is to give investors and/or readers a different perspective. We take a simple approach to building wealth. And although investing may seem easy, people often miss opportunities by over complicating it.

But we are here to help.

Current Price: $35.92

Dividend/Yield: $0.23/2.47%

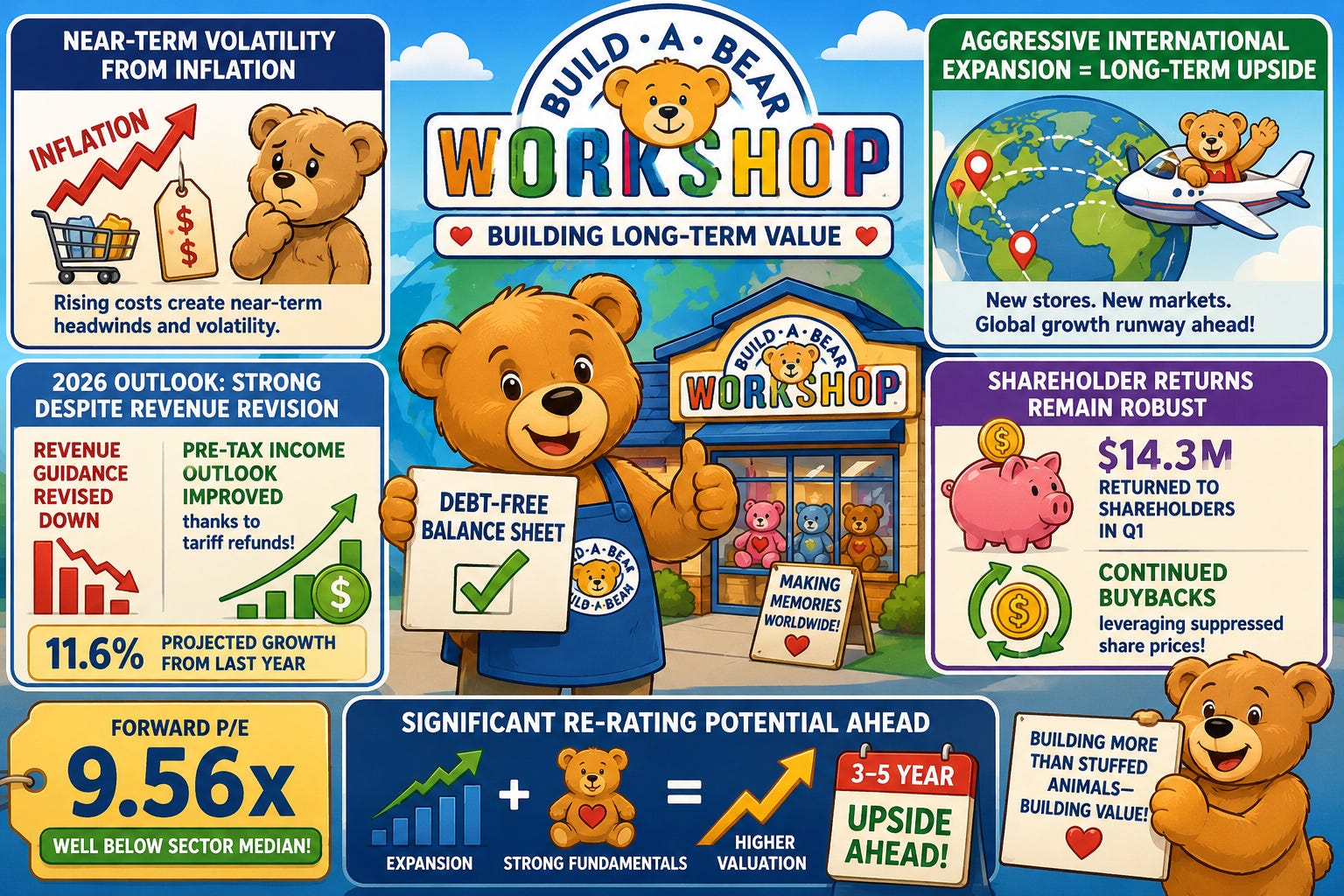

Consumer discretionary (XLY) companies have faced significant challenges over the past year. Persistent inflation, elevated energy prices, and growing economic uncertainty have pressured household budgets and forced consumers to become increasingly selective with their spending.

Build-A-Bear Workshop (BBW) has not been immune to these headwinds.

The company’s latest quarter showed clear signs that discretionary spending remains under pressure. Revenue declined year-over-year, e-commerce sales softened, and store traffic weakened. Yet despite these challenges, I believe much of the bad news is already reflected in the stock price.

With a debt-free balance sheet, aggressive international expansion strategy, growing shareholder returns, and a valuation well below peers, I continue to view Build-A-Bear as one of the more compelling long-term opportunities in retail.

While volatility may persist over the next year, I believe BBW has the potential to deliver substantial upside over the next several years as economic conditions normalize.

A Difficult Quarter, But Not A Broken Business 🧸

Build-A-Bear’s first-quarter results were mixed.

Revenue came in at $125.3 million, modestly below expectations, while earnings significantly exceeded analyst estimates. However, both revenue and earnings declined compared to last year’s record-setting quarter.

The softness was largely driven by the same issue affecting much of the consumer discretionary sector: inflation.

Net retail sales declined 5.1% year-over-year, while e-commerce sales fell more than 26%. Domestic store traffic also weakened as consumers continued to prioritize necessities over discretionary purchases.

On the surface, those numbers appear concerning.

However, investors should look beyond the headline figures.

One of the most encouraging developments from the quarter was the continued strength of Build-A-Bear’s international and commercial business. Combined revenue from these segments increased 34.1% year-over-year, reaching $11.8 million.

This growth demonstrates that management’s expansion strategy is beginning to gain traction and could become an increasingly important contributor to future results.

Margins Surprise To The Upside ↗️

While revenue disappointed, profitability was considerably stronger than expected.

Pre-tax income increased to $23.9 million compared to $19.6 million in the prior-year quarter. Gross margins expanded significantly to 64.4%, up from 56.9% last year.

Part of this improvement was driven by tariff refunds related to prior periods, but it nevertheless highlights management’s ability to protect profitability despite a difficult operating environment.

Even excluding the refund benefit, profitability remained relatively resilient considering the pressure on consumer spending.

The market appeared to recognize this strength, as shares reacted positively following the earnings release.

Guidance Wasn’t As Bad As Headlines Suggested 📰

One of the reasons investors initially reacted cautiously was management’s decision to lower revenue guidance for fiscal 2026.

The company now expects revenue between $530 million and $550 million, implying growth of approximately 1.9% at the midpoint compared to fiscal 2025.

While this represents a slowdown from previous expectations, management simultaneously raised its pre-tax income outlook.

Build-A-Bear now expects pre-tax income between $72 million and $78 million. Using the midpoint, that implies approximately 11.6% growth compared to last year’s $67.2 million.

In other words, management is expecting slower sales growth but stronger profitability.

In today’s environment, I view that as a positive development rather than a negative one.

International Expansion Remains The Biggest Catalyst 🚀

The long-term story for Build-A-Bear continues to revolve around expansion.

Over the past two years, the company has aggressively entered new international markets, adding ten countries in 2024 and another eight in 2025.

During the most recent quarter, Build-A-Bear opened seven new stores and remains on track to open approximately 50 locations during fiscal 2026.

Importantly, most of these openings are expected to occur internationally.

This matters because international markets represent one of the largest opportunities for future growth.

The company’s 34% increase in international and commercial revenue during the quarter suggests management is making the right strategic investments.

Beyond geographic expansion, Build-A-Bear continues to broaden its product portfolio through new launches, partnerships, and innovative concepts. The company recently introduced its first wearable plush product and continues expanding its retail presence through partnerships with major retailers such as Walmart (WMT).

I would not be surprised to see additional partnerships announced over the next several years as management seeks to increase brand visibility and reach new customers.

Shareholder Returns Continue To Impress 🤩

One of the most attractive aspects of Build-A-Bear’s investment case is management’s commitment to returning capital to shareholders.

During the first quarter alone, the company returned $14.3 million through dividends and share repurchases.

The majority of this came from buybacks.

Management repurchased $11.4 million worth of stock during the quarter and an additional $3.3 million after quarter-end.

I particularly like seeing aggressive repurchases when the stock trades at depressed valuations. Management is effectively investing in its own business at what I believe are highly attractive prices.

Meanwhile, the dividend remains well covered.

Build-A-Bear ended last year with a free cash flow payout ratio of just 29%, providing substantial flexibility for future dividend increases as earnings growth resumes.

Balance Sheet Is A Major Competitive Advantage ⚖️

Many retailers are navigating today’s environment while carrying significant debt loads.

Build-A-Bear isn’t one of them.

The company continues to operate with no debt on its balance sheet while maintaining solid liquidity.

This provides management with tremendous flexibility.

The company can continue opening stores, launching new products, repurchasing shares, and paying dividends without worrying about refinancing risk or rising interest expenses.

In uncertain economic environments, balance sheet strength often becomes one of the most important differentiators between winners and losers.

Why I Think Shares Can Re-Rate Higher 📉

At current prices, Build-A-Bear trades at roughly 9.6 times forward earnings.

That’s not only below the consumer discretionary sector average but also near the company’s own five-year average valuation despite the business being significantly larger and more diversified than it was several years ago.

The market is clearly discounting continued inflation pressure and weaker consumer spending.

While those concerns are valid, I believe investors are overlooking several key strengths:

Debt-free balance sheet

Strong free cash flow generation

Growing dividend

Aggressive buybacks

Rapid international expansion

Product innovation and new partnerships

If inflation eventually moderates and consumer spending improves, I believe the market could assign Build-A-Bear a multiple closer to 14x-15x earnings over time.

That level of multiple expansion alone would create meaningful upside from current prices before considering any future earnings growth.

Risks To Consider ⚠️

The biggest risk remains inflation.

If inflation remains elevated for longer than expected, discretionary spending could stay under pressure and continue weighing on revenue growth.

Consumer confidence, energy prices, and interest rate policy will all remain important variables to monitor.

Investors should also expect volatility. Build-A-Bear is a smaller company operating in a cyclical industry, which naturally creates larger swings in sentiment and share price performance.

However, I believe these risks are already largely reflected in the stock’s valuation.

Bottom Line ✅

Build-A-Bear’s latest quarter wasn’t perfect.

Revenue softened, traffic declined, and consumers remain cautious.

But beneath the surface, the business continues to execute well. Profitability remains healthy, international expansion is accelerating, shareholder returns are increasing, and the balance sheet remains exceptionally strong.

While I expect continued volatility in the near term, I believe patient investors willing to look beyond today’s macroeconomic challenges have an opportunity to purchase a quality business at a compelling valuation.

For that reason, I continue to rate Build-A-Bear a Buy and believe the stock has the potential to deliver significant upside over the next three to five years.

Do you think BBW’s international exposure will help propel the company forward and grow earnings? Let me know in the comments.

Just a note to let readers know I will be going paid soon. Be on the lookout for the article laying out the details. Feel free to provide any feedback!

Happy Investing!

☎️ If you’re looking to create passive income and build your wealth from one of the top-rated analysts, book a call (Let’s Talk Investing or Detailed Portfolio Review) with me to get started.

If you’re looking to start investing check out our investment group over on Seeking Alpha.

Here’s How: Click the Seeking Alpha link here. Click investing group, subscribe now (GET AN INVESTING GROUP FREE TRIAL), or the blue hyperlink in my bio.

Not financial advice. For educational purposes only. I am not a licensed professional. Do your own due diligence.

Like & subscribe if you’re active duty, a veteran, or just love investing.