This Overlooked Stock Has Massive Upside Potential With A P/E Less Than 8x And 3.4% Dividend Yield

As you know by my name, I love dividends. And in addition to sharing on here, I write regularly on the investment platform- Seeking Alpha.

My goal there is to teach everyday investors about building wealth, so they won’t to need to work to traditional retirement age.

I want to help you take control of your life, have F.I.R.E.

Here at Dividend Collection Agency the goal is to give investors and/or readers a different perspective. We take a simple approach to building wealth. And although investing may seem easy, people often miss opportunities by over complicating it.

But we are here to help.

Current Price: $86.17

Portfolio Purpose: Growth📈

When it comes to Omnicom Group (OMC), I’ve remained bullish for nearly a year. While higher interest rates pressured the broader market and cyclical businesses like advertising, OMC used this period to reposition its portfolio, streamline operations, and execute a transformational acquisition.

Even after the recent rally following its buyback announcement, shares trade at less than 8x forward earnings — a steep discount to historical norms — while offering a 3.5–4% dividend yield. At current levels, I view OMC as a compelling value play with potential to reach $100+ by the end of 2026.

Q4: Mixed Headline, Strong Underlying Growth 💸

OMC reported Q4 EPS of $2.59, missing estimates by $0.35, on revenue of $5.53B. Despite the miss:

EPS grew YoY from $2.41

Revenue increased YoY from $4.32B

Full-year EPS rose from $8.06 → $8.65

Revenue climbed from ~$15.7B → ~$17.3B

Organic growth accelerated to 9.3%, up from 5.2% the prior year.

Segment highlights:

Media & Advertising: +14.9%

Experiential: +19%

Precision Marketing: +8.6%

Healthcare: Returned to growth (+2.5%)

Despite volatility, the underlying business is improving — particularly in higher-growth digital and experiential areas.

IPG Acquisition: Bigger Than Initially Expected 👍🏾

OMC recently closed its acquisition of Interpublic Group, which management originally expected to generate $750M in cost synergies.

Post-earnings, they doubled synergy expectations to $1.5B over 30 months.

Additionally:

$5B total share repurchase program

$2.5B accelerated buyback

$900M in expected 2026 cost savings

Portfolio repositioning included exiting ~$2.5B in underperforming revenue streams. Management intends to complete additional divestitures within 12 months.

This is not just a cost-cutting story — it’s a structural reset aimed at margin expansion and EPS acceleration.

Dividend: Well Covered, Room to Grow 💵

In November, OMC announced a 14.3% dividend increase to $0.80 per quarter — the first raise since 2021.

2025 free cash flow:

FCF: $2.23B (up from $1.96B)

Net FCF: $1.677B

Dividends paid: ~$550M

Payout ratio: ~33%

That’s extremely conservative.

Between buybacks, dividend growth, and acquisition integration, capital allocation looks shareholder-friendly and disciplined.

Balance Sheet: Elevated Leverage, But Manageable ⚖️

Post-IPG acquisition:

Debt increased to $9.1B (from $6B)

Leverage rose to 3.1x (vs. peers lower)

Peer comparison:

WPP plc – ~2.0x

Publicis Groupe – ~1.0x

However:

Net debt: $2.23B

Cash: ~$6.9B

Revolver availability: $3.5B

Weighted avg. interest rate: 3.6%

Debt maturities manageable through 2030

Liquidity is strong. I expect deleveraging to become a focus through 2026–2027 as synergies flow through.

Valuation: This Is the Story 📖

Using expected 2026 EPS of $11.14:

Forward P/E: ~7.4x

5-year average P/E: ~11.9x

PEG ratio: 0.47x

If OMC re-rates to:

12x earnings → ~$133/share

14x earnings → ~$156/share

15x earnings → ~$167/share

Wall Street consensus sits near ~$100.50 (~21% upside).

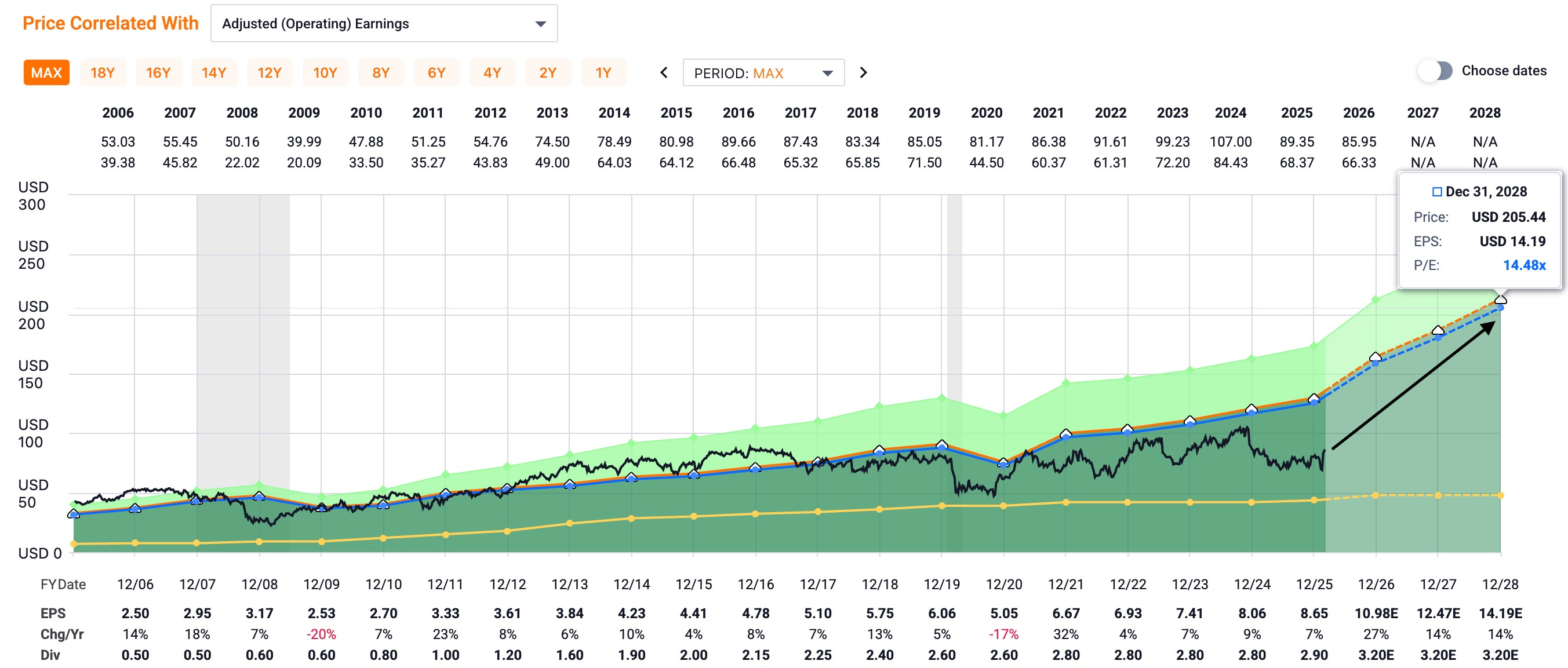

If rates decline and recession is avoided, a move above $100 by late 2026 is very achievable in my view. If the OMC can return to their historical average, upside potential is massive with a 2028 price target of $205.44.

If you’re looking for a stock analyzer tool that gives you future price targets based on historical data, use my code to get 25% off of FAST Graphs, my go-to the stock analyzer tool for research.

Risks ⚠️

Economic slowdown – Ad spending is cyclical.

AI disruption – Businesses may internalize more marketing functions.

Integration risk – IPG synergy execution must deliver.

That said, at <8x earnings, much of the macro risk appears priced in.

Bottom Line ✅

Omnicom is not a high-growth tech stock. It’s a mature, cash-generating advertising powerhouse trading at a distressed multiple.

You’re getting:

High single-digit to double-digit earnings growth potential

$1.5B in synergy upside

Massive buyback support

3.5–4% dividend yield

Balance sheet flexibility

Valuation far below historical norms

At today’s price, I believe downside is limited relative to upside potential. If execution continues and macro conditions stabilize, $100+ by 2026 looks very reasonable — with significantly higher levels possible over a multi-year horizon.

This is the type of asymmetric setup value investors look for.

Are you buying Omnicom? Why or why not? Let me know in the comments.

Happy Investing!

☎️ If you’re looking to create passive income and build your wealth from one of the top-rated analysts, book a call (Let’s Talk Investing or Detailed Portfolio Review) with me to get started.

If you’re looking to start investing check out our investment group over on Seeking Alpha.

Here’s How: Click the Seeking Alpha link here. Click investing group, subscribe now, or the blue hyperlink in my bio.

Not financial advice. For educational purposes only. I am not a licensed professional. Do your own due diligence.

Like & subscribe if you’re active duty, a veteran, or just love investing.