Trump's Proposed 10% Credit Card Cap Won't Save You!

"Why The Credit Card Cap Does More Harm Than Good"

As you know by my name, I love dividends. And in addition to sharing on here, I write regularly on the investment platform- Seeking Alpha.

My goal there is to teach everyday investors about building wealth, so they won’t to need to work to traditional retirement age.

I want to help you take control of your life, have F.I.R.E.

Here at Dividend Collection Agency the goal is to give investors and/or readers a different perspective. We take a simple approach to building wealth. And although investing may seem easy, people often miss opportunities by over complicating it.

But we are here to help.

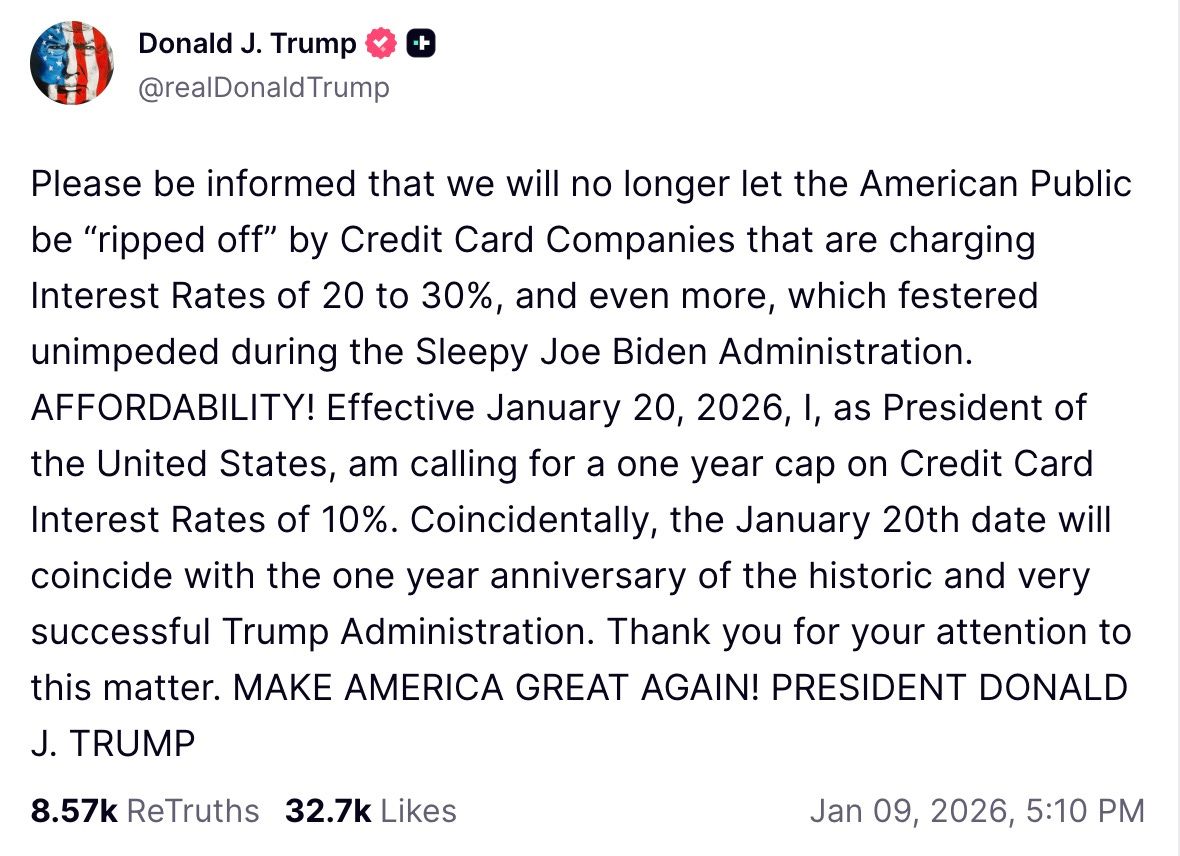

By now, most Americans have heard about the President’s suggestion to place a 10% cap on credit card interest rates for one year. The proposal is framed as a way to protect consumers from what are often described as “predatory” rates in the 20%–30% range.

In a Truth Social post, Donald Trump stated that he would no longer allow Americans to be “ripped off” by credit card companies and banks charging excessive interest.

On the surface, this sounds like a win for consumers.

But beneath the headlines, I believe a 10% cap would ultimately hurt Americans more than it helps—especially those who rely most on credit cards. At the time of writing, financial stocks have already sold off modestly on the news.

While I believe the chances of this proposal becoming law are slim, if it were approved, it could trigger a sharp sell-off across parts of the Financial sector (XLF). For long-term dividend investors, that volatility could present opportunity.

In this article, I’ll explain why a rate cap would backfire and what income-focused investors should consider if it happens.

Rate Caps Shift the Risk—They Don’t Remove It ⚠️

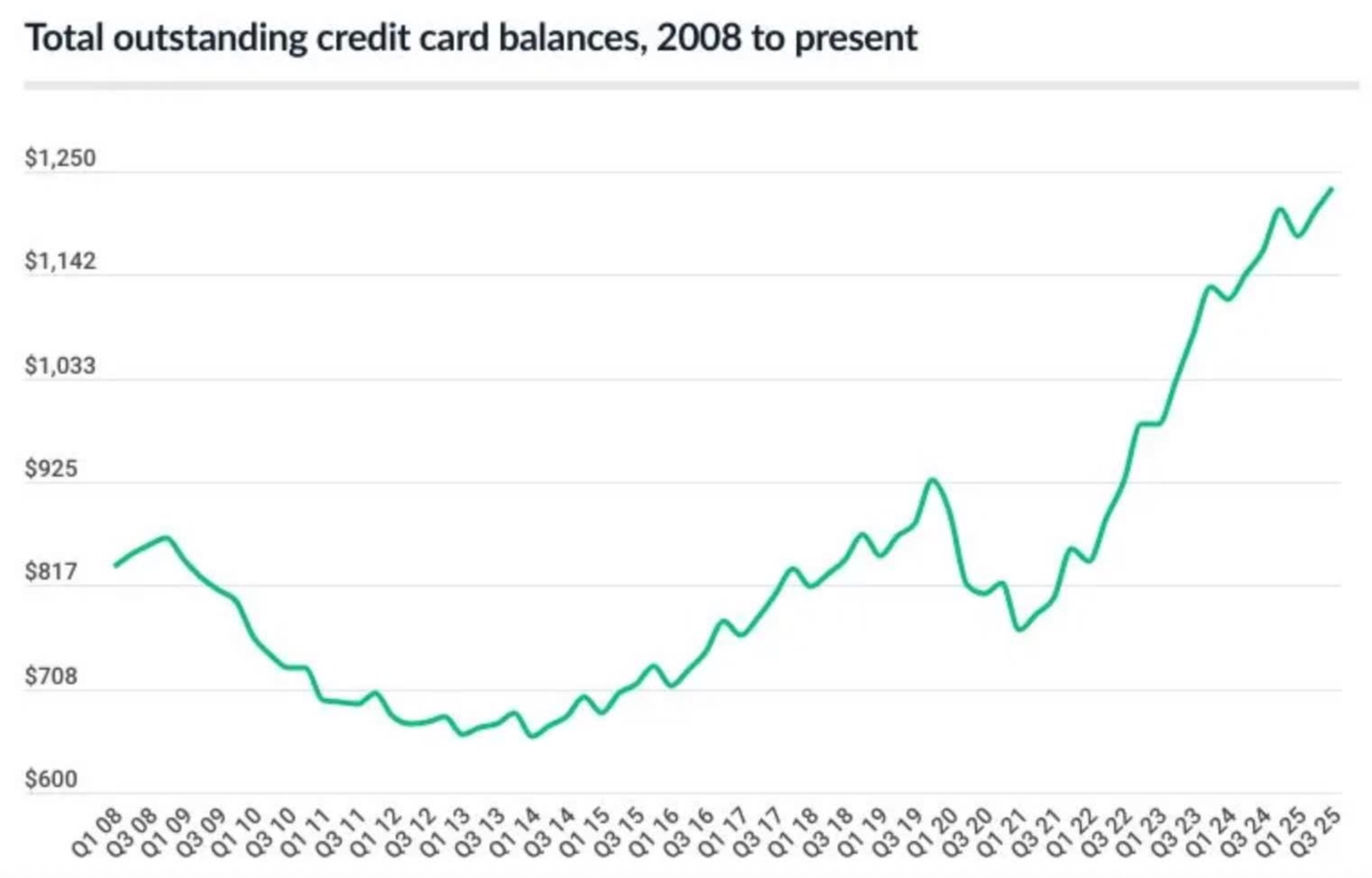

Outstanding U.S. credit card balances tell a clear story.

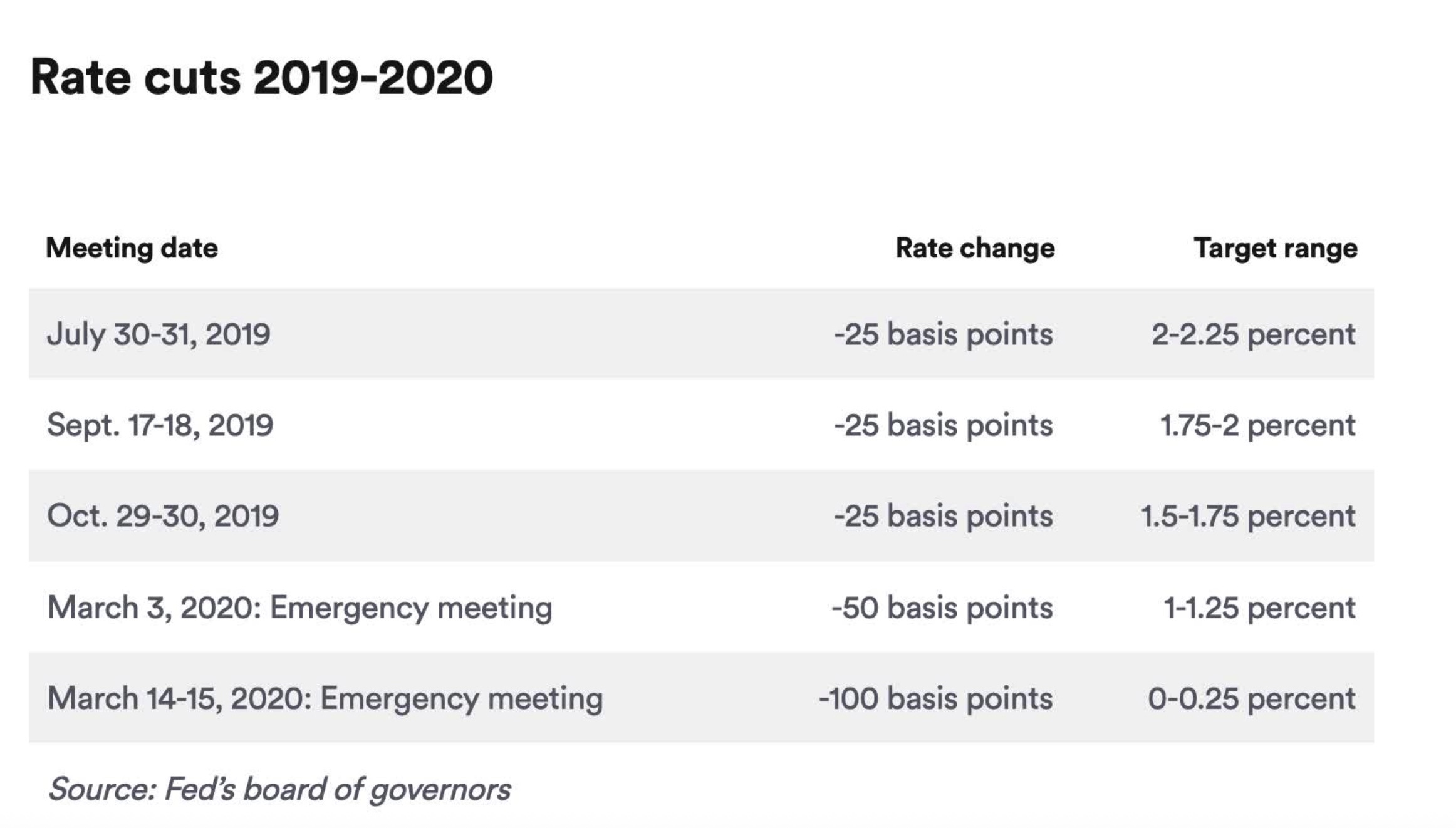

After peaking in 2008, balances declined through the early 2010s as the Federal Reserve slashed rates during the Great Financial Crisis. A similar pattern occurred in 2019–2020 when rates were again cut aggressively.

But since 2022, credit card debt has exploded.

Why? The Fed’s fastest rate-hiking cycle in history dramatically raised the cost of everyday living.

Food, housing, insurance, and transportation all became more expensive—forcing many households to rely on credit cards just to get by.

Today, U.S. credit card debt exceeds $1 trillion, a flashing red warning sign of household stress.

While higher rates benefit savers through HYSAs, money markets, and CDs, they’re devastating for consumers carrying revolving debt. And for many Americans, credit card use isn’t driven by reckless spending—it’s driven by necessity.

Lower-income and financially stressed consumers also tend to have lower credit scores, which means higher APRs. Even borrowers with excellent credit often pay well above 10%.

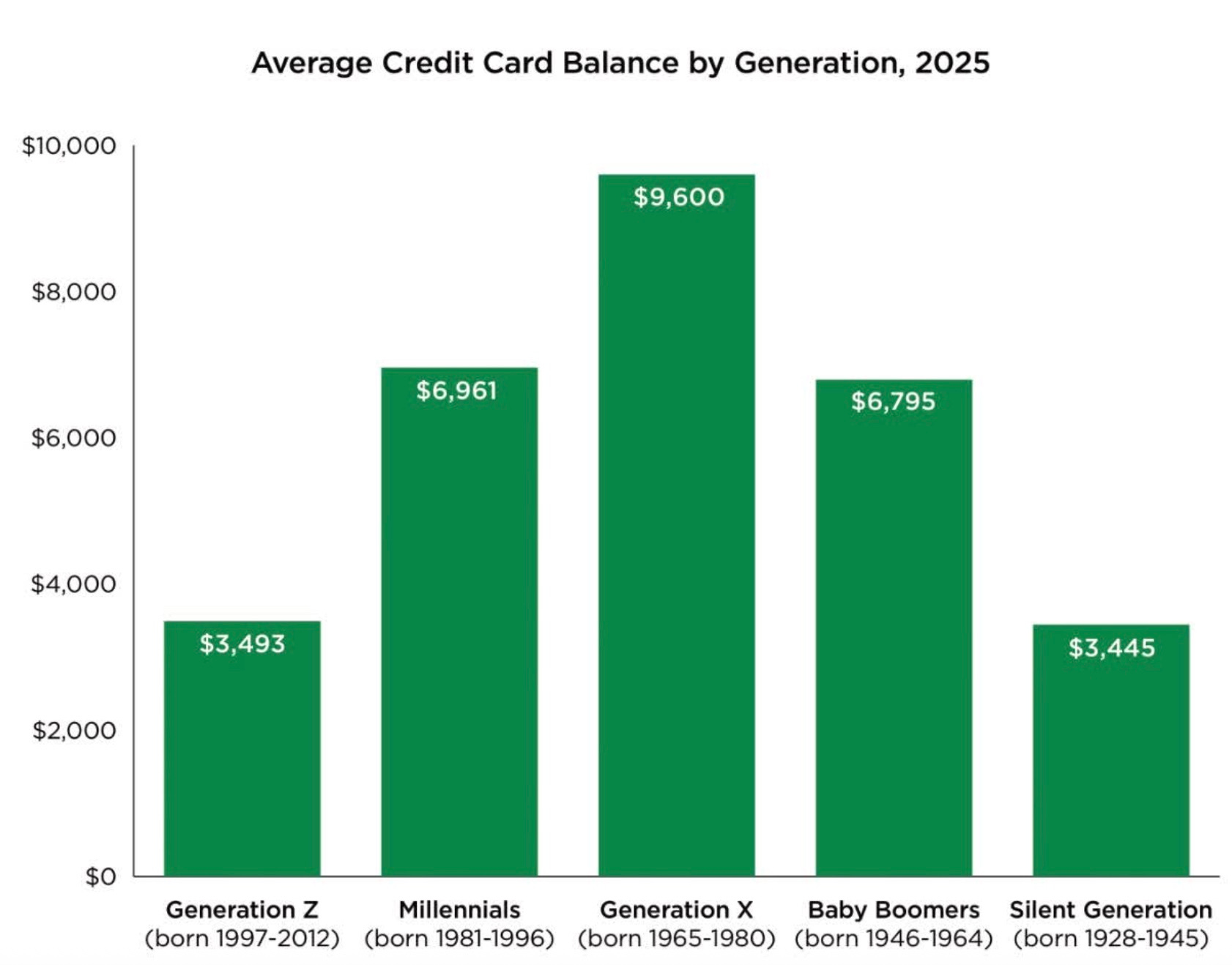

Below is the average credit card balance by generations.

For context, despite having a strong credit profile, both of my personal bank cards currently charge 12%–13% APRs. And my other credit cards, even more.

How Banks Actually Make Money 💵

Banks don’t lend out of generosity. Their business model is simple:

Borrow money at lower rates

Lend it at higher rates

Collect interest, fees, and transaction revenue

Credit cards are incredibly profitable because they generate:

Interest income

Swipe fees

Late fees

Annual fees

A mandated 10% cap would compress margins dramatically. Especially when banks still face funding costs, fraud risk, and defaults.

That leads to an important question:

How would banks respond?

How Banks Would Likely Respond 😳

If a 10% cap became law, banks wouldn’t just accept lower profits. They would adapt—and not in ways that help consumers.

Likely responses include:

Tighter credit approvals

Reduced card issuance

Cuts to rewards and perks

Higher fees elsewhere

Who gets hurt the most?

Lower- and middle-income Americans who rely on credit cards for flexibility and emergencies.

Higher-risk borrowers would likely be screened out entirely, while existing cardholders could see benefits erode. Fewer perks, fewer rewards, and fewer options—precisely for the consumers the policy is supposed to protect.

Why Credit Card Companies Would Feel It Too 💳

Although companies like Visa (V) and Mastercard (MA) don’t set interest rates, they depend on transaction volume.

If banks tighten approvals and issue fewer cards, transaction growth slows.

Recent data highlights the scale:

Mastercard reported 3.6 billion cards worldwide, up 6% year over year

Visa has approximately 4 billion cards in circulation

Even modest slowdowns would impact revenue growth—and investor sentiment. Especially, since both stocks trade at premium valuations.

Banks Would Slash Perks First 🏦

Banks would almost certainly cut rewards before anything else.

I personally hold cards from American Express (AXP) and JPMorgan Chase (JPM). One AMEX perk I regularly use is monthly Uber (UBER) cash, which was already reduced during inflationary pressures.

If a rate cap passed, I would fully expect:

Reward reductions

Cash back cuts

Annual fee justification erosion

Cash back programs—often 2%–3%—are especially vulnerable. Ironically, many disciplined investors use those rewards to invest, not spend. Cutting them would quietly reduce household wealth-building.

We’ve Seen This Movie Before 🎥

This isn’t hypothetical.

After the Great Financial Crisis, debit card interchange fees were capped under new regulations meant to protect consumers. Banks responded by:

Eliminating free checking

Cutting perks

Introducing new account fees

More recently, banks pushed back hard when rate caps were floated again in 2023.

The difference today? Interest rates remain higher for longer, which means banks have less room to absorb margin pressure without passing costs back to consumers.

Volatility Creates Opportunity 💡

For transparency, I currently own Visa. Mastercard and American Express are two companies I’ve wanted to own for years.

If a 10% cap were approved, I would expect a knee-jerk sell-off across:

Visa

Mastercard

American Express

Valuations are elevated, and any threat to growth would hit sentiment fast.

I wouldn’t be surprised to see:

Visa dip below $300

Mastercard fall below $500

American Express sell off the hardest due to its banking exposure

Historically, these pullbacks are short-lived.

Over the past decade, all three have crushed the broader market, delivering strong total returns and double-digit dividend growth supported by healthy cash flows.

Bottom Line ✅

Visa, Mastercard, and American Express are high-quality businesses that rarely stay down for long.

I believe the odds of a 10% credit card rate cap becoming law are low. The unintended consequences—tighter credit, fewer perks, and reduced access—would hurt the very consumers it aims to help.

But if the market overreacts?

That’s when long-term dividend investors should pay attention.

If these stocks sell off sharply, consider setting limit orders and using volatility to your advantage. In my view, any panic would likely be temporary—while the actual businesses themselves remain enduring compounders.

What do you think of the 10% cap rate? Let me know in the comments.

Happy Investing!

☎️ If you’re looking to create passive income and build your wealth from one of the top-rated analysts, book a call (Let’s Talk Investing or Detailed Portfolio Review) with me to get started.

If you’re looking to start investing check out our investment group over on Seeking Alpha.

Here’s How: Click the Seeking Alpha link here. Click investing group, subscribe now, or the blue hyperlink in my bio.

Not financial advice. For educational purposes only. I am not a licensed professional. Do your own due diligence.

Like & subscribe if you’re active duty, a veteran, or just love investing.