Why I Wouldn't Buy Nike Right Now Despite The 4% Yield

"Iconic Brand, But Not An Iconic Investment"

As you know by my name, I love dividends. And in addition to sharing on here, I write regularly on the investment platform- Seeking Alpha.

My goal there is to teach everyday investors about building wealth, so they won’t to need to work to traditional retirement age.

I want to help you take control of your life, have F.I.R.E.

Here at Dividend Collection Agency the goal is to give investors and/or readers a different perspective. We take a simple approach to building wealth. And although investing may seem easy, people often miss opportunities by over complicating it.

But we are here to help.

Current Price: $43.76

Dividend: $0.41

Nike (NKE) remains one of the world’s most recognizable brands, but a great company doesn’t always make a great investment.

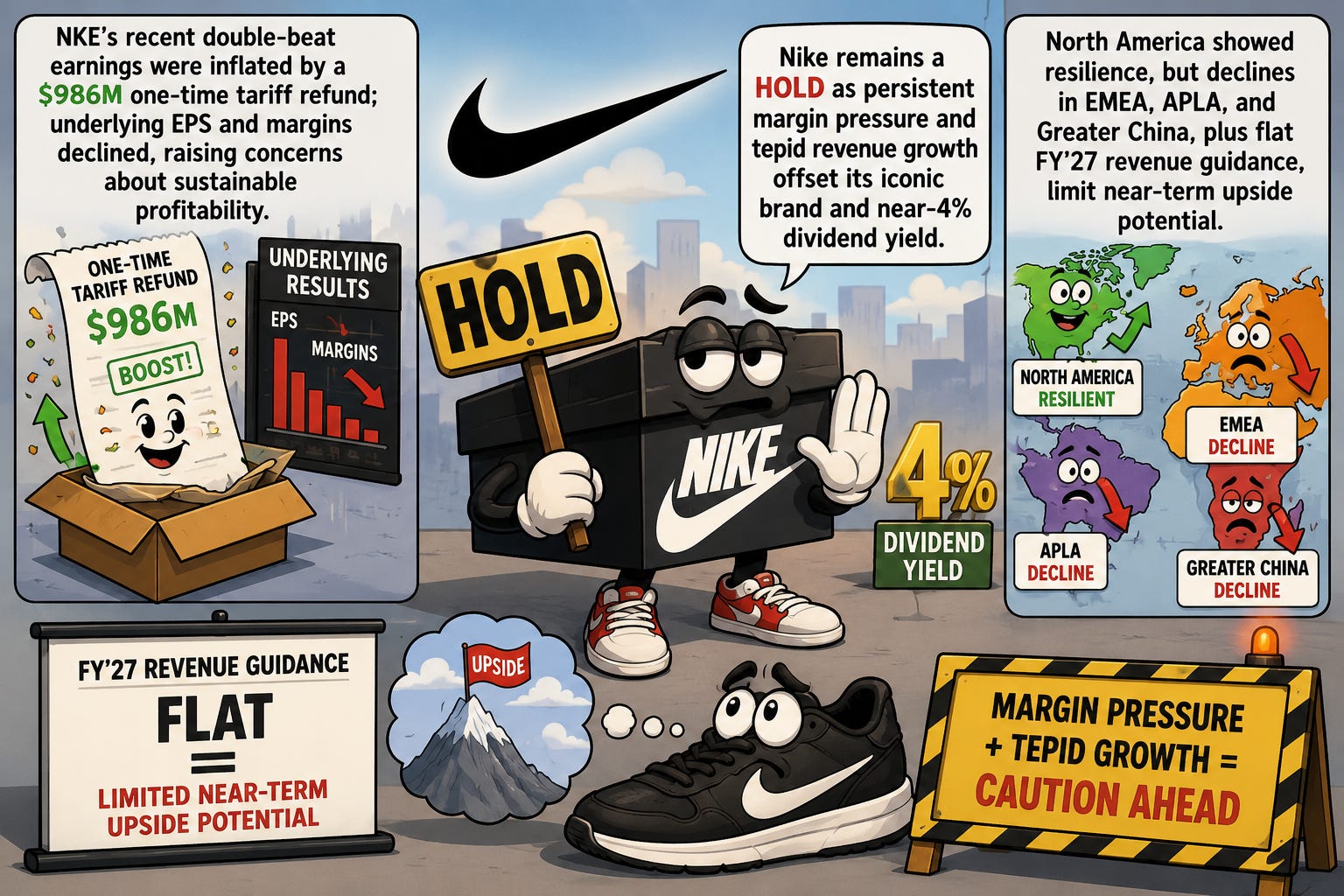

Despite shares trading well below their historical valuation and offering a dividend yield approaching 4%, I continue to believe the risk/reward remains unfavorable. While Nike posted another earnings beat, the headline numbers were significantly boosted by a one-time tariff refund, masking continued weakness in the underlying business.

Here’s why I remain cautious.

The Earnings Beat Wasn’t As Strong As It Looked 🫣

At first glance, Nike’s Q4 results appeared impressive.

EPS beat estimates by $0.59

Revenue topped expectations by roughly $150 million

However, the company received a $986 million one-time tariff refund, which dramatically inflated profitability.

Without that benefit:

Underlying EPS would have been approximately $0.20 instead of $0.72

Full-year EPS would have declined roughly 27%

Gross margins would have fallen, not expanded

This helps explain why Wall Street largely ignored the headline beat.

There Were Some Bright Spots ☀️

Not everything was negative.

North America continued improving as revenue rose 3%, supported by strength in:

Running

Global Football

Kids

Nike’s Running business also posted its fifth consecutive quarter of double-digit growth, adding roughly $1 billion in sales while gaining market share.

China also showed modest improvement.

Although sales still fell 12%, that was a meaningful improvement from the 20% decline experienced a year ago.

International Weakness Remains A Major Problem 🌎

Unfortunately, those positives weren’t enough to offset weakness elsewhere.

EMEA revenue fell 6%

APLA declined 1%

Greater China remains under pressure

Digital sales continue struggling across several regions, and management expects Q1 revenue to decline low-to-mid single digits.

Even more concerning, Nike expects FY2027 revenue to remain essentially flat, suggesting the turnaround will likely take longer than many investors anticipated.

The Dividend Looks Safe…For Now ⚠️

Nike’s balance sheet remains one of its biggest strengths.

The company finished the year with:

$7.6 billion in liquidity

Relatively modest debt levels

An A-rated balance sheet

That should support the dividend over the near term.

My concern isn’t an immediate dividend cut.

Instead, weakening earnings and declining cash generation could eventually limit future dividend growth if profitability doesn’t improve.

Valuation Isn’t Cheap Enough 💸

Many investors point to Nike trading below its five-year average valuation.

While that’s true, the stock still trades at more than 25x forward earnings—a premium for a company experiencing:

Slowing growth

Margin pressure

Weak international demand

Flat revenue guidance

Until Nike proves it can consistently expand margins and improve cash flow, I believe investors are still paying too much for future optimism.

Final Thoughts ✅

Nike remains an iconic company with one of the strongest brands in the world, but I believe the investment story still needs work.

The latest earnings beat looked impressive on the surface, yet much of the upside came from a one-time tariff refund rather than improving operations.

North America continues making progress, but persistent weakness across China and other international markets, combined with compressed margins and flat revenue expectations, keeps me on the sidelines.

I’d become more constructive if management can deliver sustained margin expansion, stronger free cash flow, and meaningful international growth—but until then, I believe better dividend opportunities exist elsewhere.

RATING: HOLD

Are You Buying Nike In The Low $40’s?

Let me know what you think in the comments.

💰 Happy Investing 💰

☎️ If you’re looking to create passive income and build your wealth from one of the top-rated analysts, book a call (Let’s Talk Investing or Detailed Portfolio Review) with me to get started.

If you’re looking to start investing check out our investment group over on Seeking Alpha.

Here’s How: Click the Seeking Alpha link here. Click investing group, subscribe now (GET AN INVESTING GROUP FREE TRIAL), or the blue hyperlink in my bio.

Not financial advice. For educational purposes only. I am not a licensed professional. Do your own due diligence.

Like & subscribe if you’re active duty, a veteran, or just love investing.