Why Is The Stock Market Giving Amazon The Microsoft Treatment?

"Why Amazon Is A Long-Term Buying Opportunity"

As you know by my name, I love dividends. And in addition to sharing on here, I write regularly on the investment platform- Seeking Alpha.

My goal there is to teach everyday investors about building wealth, so they won’t to need to work to traditional retirement age.

I want to help you take control of your life, have F.I.R.E.

Here at Dividend Collection Agency the goal is to give investors and/or readers a different perspective.

We take a simple approach to building wealth. And although investing may seem easy, people often miss opportunities by over complicating it.

But we are here to help.

Current Price: $231.90

Years ago, while I was still serving on active duty, I joked with one of my co-workers that Amazon (AMZN) would one day rule the world. Looking at the company today, I’m not so sure it was much of a joke.

From cloud computing and advertising to AI infrastructure, logistics, healthcare, and autonomous vehicles, Amazon continues expanding into industries that could fuel growth for years.

Yet despite all of that, the stock has largely gone nowhere over the past year.

I believe investors are making the same mistake they recently made with Microsoft—focusing on short-term free cash flow instead of long-term competitive positioning.

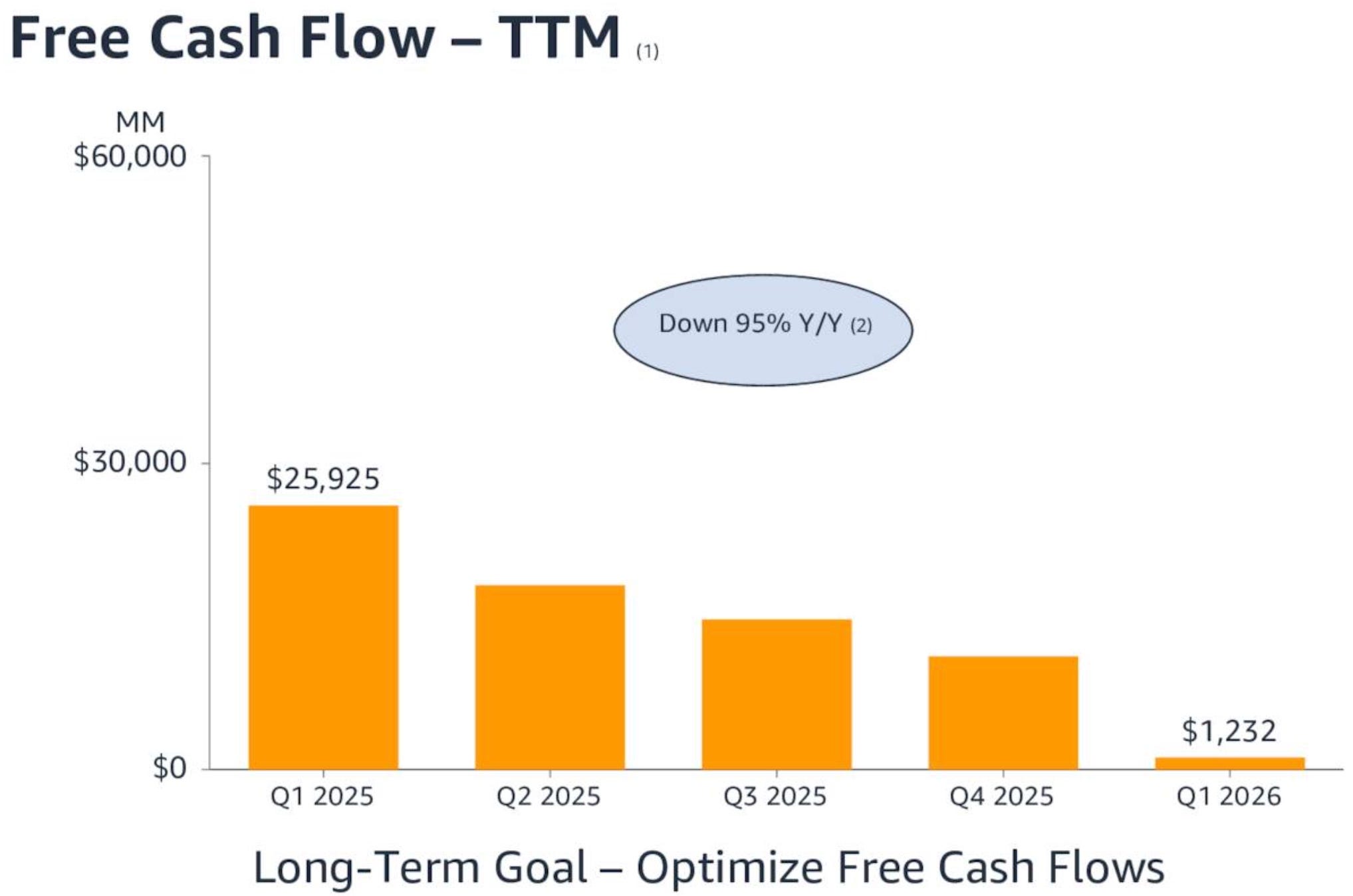

The Market Is Focused On The Wrong Metric 📊

Amazon’s aggressive AI spending has pressured free cash flow, causing many investors to question whether the company is overspending.

I see it differently.

Management isn’t sacrificing the future to improve quarterly numbers—they’re sacrificing today’s cash flow to strengthen Amazon’s competitive advantage over the next decade.

During the latest quarter:

Cash from operations increased 30% to $148.5 billion.

AWS revenue accelerated 28%.

Advertising revenue grew 22%.

Operating income climbed 30%.

Margins improved across both North America and International operations.

Those aren’t the numbers of a slowing business.

They’re the numbers of a company investing heavily while its core businesses continue accelerating.

Free Cash Flow Doesn’t Tell The Entire Story 📖

Free cash flow declined dramatically as capital expenditures surged to support AI infrastructure.

While that headline has worried investors, I believe it’s largely a timing issue rather than a deterioration in the underlying business.

Amazon is building the infrastructure required to compete in what could become a multi-trillion-dollar AI market.

These investments reduce near-term cash flow, but they also create barriers to entry that competitors will struggle to match.

If AI monetization unfolds as expected, today’s spending could generate significantly higher cash flows later this decade.

A Fortress Balance Sheet ⚖️

Amazon is uniquely positioned to fund this investment cycle.

The company ended the quarter with roughly $102 billion in cash and has no significant debt maturities until 2028.

Unlike many companies, Amazon doesn’t need to slow investment or raise capital to fund growth.

Its balance sheet allows management to invest aggressively while maintaining financial flexibility.

Risks ⚠️

The biggest risk is straightforward.

If AI adoption or monetization develops more slowly than expected, Amazon could experience a longer period of depressed free cash flow.

Persistent inflation and higher interest rates could also continue pressuring valuation multiples, causing additional near-term volatility.

Those are legitimate risks.

However, I believe they’re outweighed by Amazon’s long-term competitive advantages.

Long-Term Opportunity 📉

Analysts continue projecting strong earnings growth over the coming years.

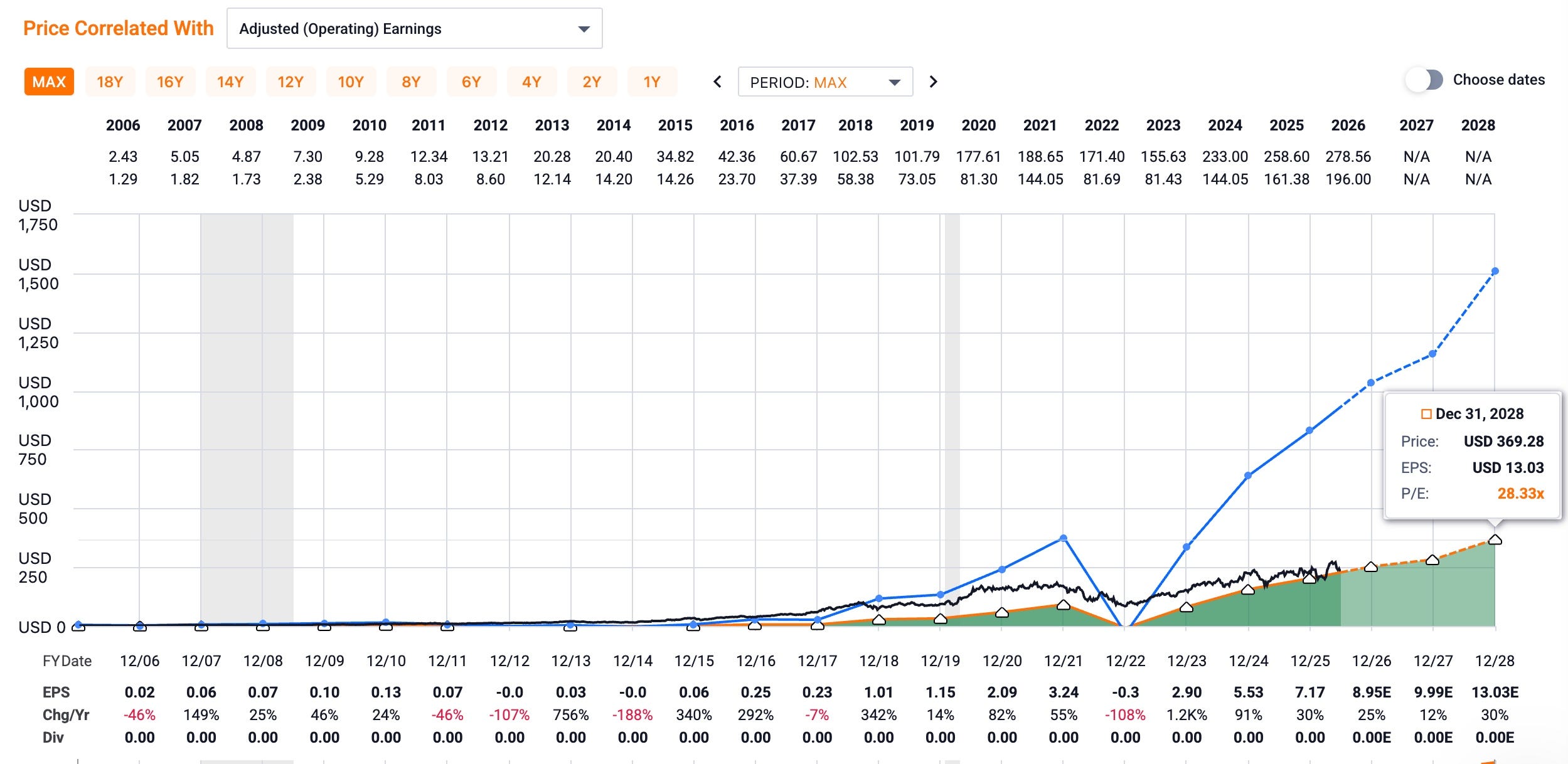

If earnings compound near current expectations and Amazon eventually returns to trading above 30x earnings, I believe the stock has meaningful upside from current levels. This also means the stock could surpass FastGraph’s 2028 price target of $369 a share.

If you’re looking for a stock analyzer tool that gives you future price targets based on historical data, use my code to get 25% off of FAST Graphs, my go-to the stock analyzer tool for research.

While the next several quarters may remain volatile, I view that volatility as an opportunity rather than a warning sign.

Investors often reward companies after the payoff becomes obvious—not while they’re making the investments that create it.

Final Thoughts ✅

The market appears fixated on Amazon’s declining free cash flow.

I believe it should be focused on everything else.

Revenue is accelerating.

AWS continues gaining momentum.

Advertising remains a high-margin growth engine.

Operating income continues expanding.

Most importantly, Amazon is investing aggressively in technologies that could define the next decade of computing.

For long-term investors willing to look beyond today’s cash flow pressures, I believe Amazon remains one of the highest-quality growth opportunities in the market.

RATING: BUY

Does Amazon fit into your investment strategy even though the company does not currently pay a dividend? Let me know in the comments.

Happy Investing 💰

☎️ If you’re looking to create passive income and build your wealth from one of the top-rated analysts, book a call (Let’s Talk Investing or Detailed Portfolio Review) with me to get started.

If you’re looking to start investing check out our investment group over on Seeking Alpha by clicking the link below the picture.

Here’s How: Click the Seeking Alpha link here. Click investing group, subscribe now (GET AN INVESTING GROUP FREE TRIAL), or the blue hyperlink in my bio.

‼️ Seeking Alpha is also currently offering a 20% membership sale ‼️

Not financial advice. For educational purposes only. I am not a licensed professional. Do your own due diligence.

Like & subscribe if you’re active duty, a veteran, or just love investing.